Sokol's Dirty

My bet is that Mary Schapiro over at the SEC started looking at Sokol as of this morning. The optics on this one are terrible. So there has to be some noise from the regulator. I'm also willing to bet that nothing comes from it. Insider trading is a very tough case to make. Wiretaps and witnesses are needed.

My bet is that Mary Schapiro over at the SEC started looking at Sokol as of this morning. The optics on this one are terrible. So there has to be some noise from the regulator. I'm also willing to bet that nothing comes from it. Insider trading is a very tough case to make. Wiretaps and witnesses are needed.

I was on both the buy and sell side. I pitched a thousand deals and listened to the sale from the other side of the desk. The rules were always the same. If you were talking a deal you didn't trade the stock. Period.

It might be useful to have Citi chime in on this. What are their house rules on this? They were pitching this deal to Sokol. If anyone on that deal team were trading the stock they would be out in an hour. If Berkshire has no hard rules on this, well, shame on them and shame on Warren B.

One thing that rubs me is that Sokol has made it out that he was just trying to make a few extra bucks so that he could give some more away. Like he is a nice guy. Bull…. He's just another predator.

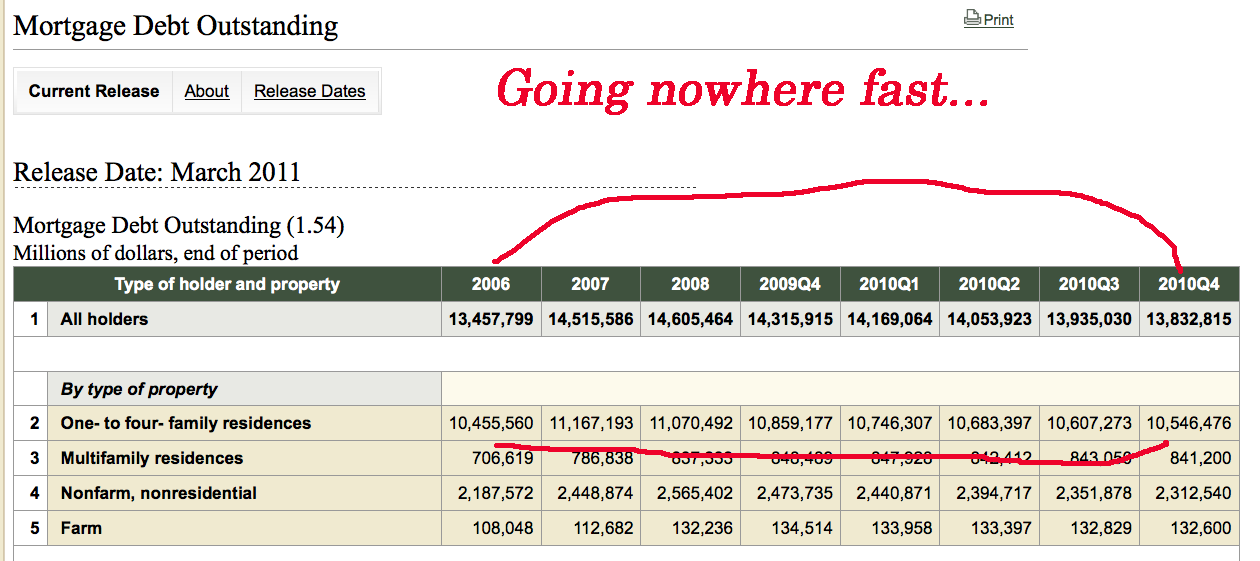

Mortgages Outstanding

The FRB 4th Q 2010 Mortgages Outstanding report is hardly worth looking at. Nothing is happening in mortgage land. The lines are basically flat.

The FRB info is stale, but Fannie just released its report for February. Same thing. There is no growth in mortgages. There continues to be a very small month to month declines.

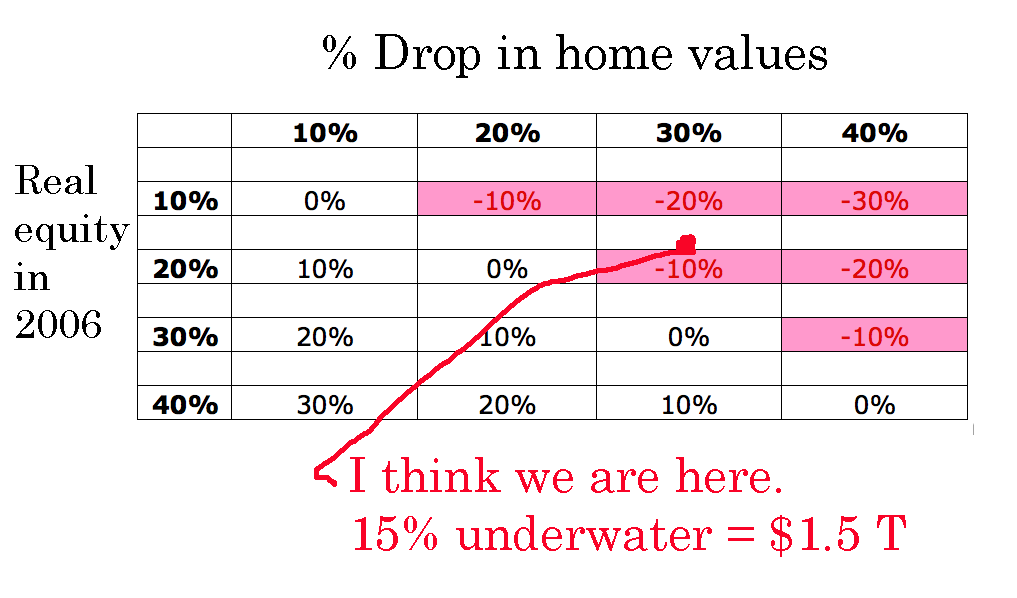

I was looking at this data and trying to draw some conclusions on how “healthy” these .5T of mortgages are. I have no reliable data on key variables, so I set up a matrix. The question I want to answer is how much real equity is behind all this paper today?

How much equity was there behind the housing stock in 2006? The answer is, A) At least 5%, but B) less than 50%. So the variables would be 10, 20, 30 and 40%.

How much has residential real estate fallen in value since 2007? It's the same as above. At least 5% but less than 50%. So I considered what it looks like using drops in values of 10, 20, 30 and 40%.

I think equity (fair value minus mortgage) was around 15% in 2006. There was a lot of 100% cash out ReFi-ing going on back then. There was also a lot of high LTV mortgages being handed out. 15% equity is a generous assumption. I think the average loss of value is about 30% nationwide. This too masks reality as the biggest concentrations of homes are in areas that saw greater than 30% declines.

The conclusion is that there is still very substantial negative equity in the broad mortgage pool. The number starts with T. You can make your own dot on the chart. We ain't out of these woods yet.

Price of 'Talent'

Ed DeMarco, the fellow running the FHFA, appeared before the Subcommittee on Capital Markets, Insurance, and Government-Sponsored Enterprises today.

He had 16 pages of prepared remarks. All boring except for the last paragraph:

I am concerned that legislation to overhaul the compensation levels and programs in place today with the application of a federal pay system to non-federal employees carries great risk for the conservatorships and hence the taxpayer. I understand and have sympathy for what might motivate such a proposal, but I must report to this Subcommittee my firm view that such an action would, on balance, increase costs to taxpayers and risk further disruptions in housing market.

If DeMarco was talking with some friends he might have said it differently:

I need finance people. Lots of them. I need people who understand credit. MBS Traders. Back office types. People who understand and can price derivatives. Market economists. I need managers.

But I can't get them. Government pay doesn't draw the talent we need. I'm sitting on a time bomb. A 6 trillion book and the good people are all leaving. The private sector is sucking them up.

I know it sounds crazy but we have to pay the head of a government agency 4Xs what the president makes.The geeks who evaluate our derivative book earn (on Wall Street) 3Xs what a congressman makes.

I see no way around this. I fear it will end badly.

De Marco is a smart fellow. Consider his words a warning. We really don't want the guys who finished last in the class running these beasts. (Fan and Fred are not going away anytime soon). The flip side is equally unacceptable. Big salaries for mid level management and geeks at Fan and Fred? That would go over big…… We ain't out of these woods yet.

Supply

Dian L. Chu did a good summary of the supply side of crude. Bottom line; Cushing is full (damn near). If supply and demand have anything to do with the outcome the price is headed lower. Tough to argue with.

I wrote about the Cushing issue some time ago and got what I thought was an interesting comment from someone:

Today is March 2. A 100 tank car train left Stanley North Dakota loaded with Bakken oil headed to St. James Louisiana… delivered price was 4.60 a barrel… burlington northern rail road is charging a barrel for freight… by passing cushing oklahoma because it is full… and with limited oil out of the offshore rigs it pays to haul it all the way across the continent.........wow.

That was a month ago. Nothing has changed. High grade crude for Gulf delivery is still at a very big premium to WTI. bucks as of this afternoon.

A Few Questions

- Are trains running with crude? If not, why not?

- Is the /brl a good number for transportation? If so why the apparent arbitrage?

- Are “we” paying gas prices based on Cushing or LLS?

- It looks like there is a boatload to be made here. Is there? Who's making it?