The American economy is set to recover, if only that huge 800-lb European gorilla won't squash everything.

With interest rates at record lows and set to stay that way for at least another year, the Federal Funds Target Rate is no longer a significant instrument in the Fed’s tool shed to move the economy. Francois Trahan, Head of Portfolio Strategy & Quantitative Research at Wolfe Trahan, has noted that the inflation cycle is the new Federal Funds Rate. When inflation is elevated it cuts into consumer wallets and corporate profits, and when the inflation rate falls the converse is true. Thus, the plunge in commodity prices since April-May is providing a disinflationary stimulus that is currently leading to an economic rebound. Given inflation trends have a lagging impact on the economy by roughly six months and commodities recently bottomed in October of this year, we could expect a manufacturing rebound to continue into Q1 to Q2 of 2012. However, that may all be thrown out the window if the 800 lb gorilla, which is the European credit crisis, is not resolved in short order as fear will likely permeate into consumer and business sentiment, leading both to tighten their purse strings and dash any hope of an American recovery.

Leading Indicators Pointing to Manufacturing Recovery

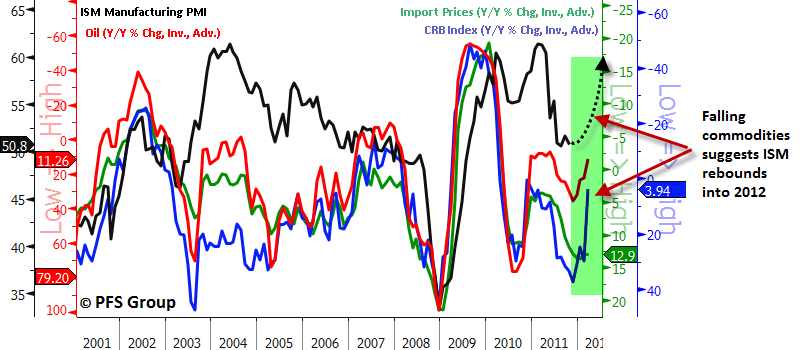

As mentioned in the opening paragraph, inflation trends have proven to be a great tool at predicting economic turning points as their peaks and troughs are associated with peaks and troughs in manufacturing roughly six months down the line. With commodities peaking in the spring, one could predict an economic turnaround late in the fall which appears to be happening as the ISM Manufacturing PMI has stopped falling. Shown below are the trends in commodities relative to the ISM Manufacturing PMI, with the commodities shown inverted for directional similarity and advanced. As seen below, the declining commodity inflation pressures over the prior six months forecast the ISM to rebound heading into early 2012.

Source: Bloomberg

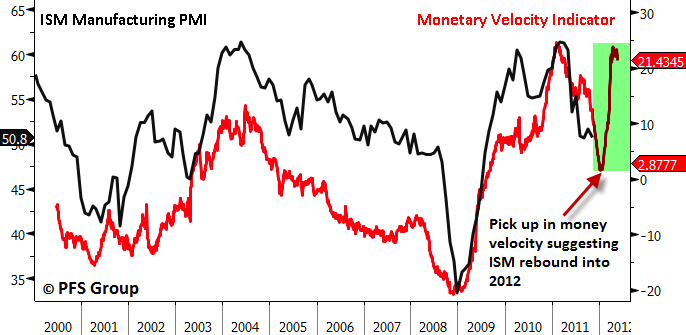

Other indicators such as money velocity are also predicting a pickup in the manufacturing sector heading into 2012 as previously created money trickles into the economy.

Source: Bloomberg

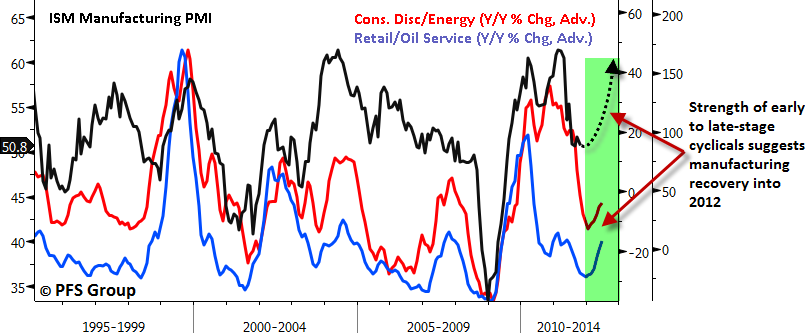

Even the interplay between sectors in the stock market is suggesting a pickup in manufacturing activity. The leading tendencies between the sectors that are hurt by inflation (consumer discretionary stocks) and those that benefit from inflation (energy stocks) are suggesting a rebound in manufacturing. The relative performance of the consumer discretionary sector to the energy sector suggests the ISM should improve over the next few months.

Source: Bloomberg

In addition to an improved manufacturing outlook, we may also see improvement in the labor market. US job openings tend to lead overall employment levels by several months and the fact that job openings just hit a cycle high suggests payrolls may continue to expand for the next several months, a welcome news for everyone. We have yet to see the drop off in job openings as we did during the 2001 and 2007 recessions and as long as job openings continue to rise so too should overall employment levels.

Source: Bloomberg

With the negative economic momentum seeming to end over the last two months, it was encouraging to see our recession probability model fail to exceed the 20% threshold level typically associated with recessions, with the 1987 breach the only exception.

Source: Bloomberg

The 800 Pound Gorilla

While the outlook is markedly improved from a few months ago and despite the message of leading indicators suggesting further improvement ahead, today’s investing climate could see winds change at a moment's notice. There is no doubt that the current 800 pound gorilla in the room is the European debt crisis, which, if left unchecked, could lead to another global recession. Either Germany relents to EU pressure and blinks by standing aside while the ECB embarks on massive money printing to support sovereign debt markets and shore up the commercial banks, or the euro zone breaks up with either the strong or the weak links leaving. If Germany stands aside and lets the ECB print money then we could expect a massive reflationary boom not unlike what was seen with the U.S. QE 1 and 2. However, if the Euro zone fails to come to some type of solution then the debt markets across the pond will continue to erupt with bond yields and credit default swaps surging. Bankruptcies and sovereign defaults could ripple through the global credit system and elevate fear to the point that consumers and businesses close their purse strings and either fail to spend in the consumers case or fail to invest in terms of corporations.

Shown below are various credit spreads and we can see that the Euro 2-year currency swap has nearly reached the levels seen at the height of the 2008 credit crisis as stress and credit market tensions remain high. Additionally, we are starting to get signs of contagion here domestically as USD 2-year currency swaps have also risen significantly over the last two weeks and are at their highest levels in more than a year. Other traditional credit measures such as the TED Spread and the LIBOR-OIS spread haven risen slowly for six months straight, though still below 2010 levels and 2008 highs.

Source: Bloomberg

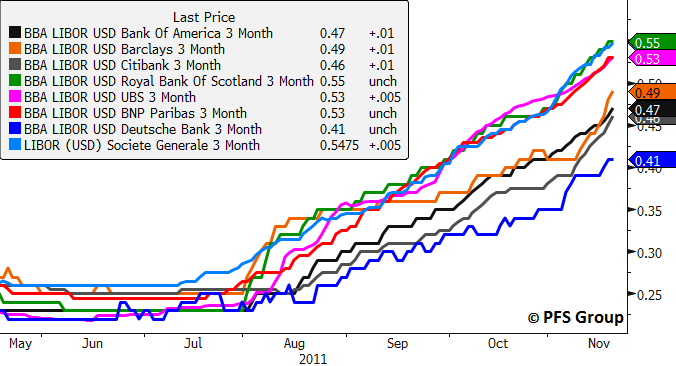

Credit tensions among banks also remains high as overnight lending rates between banks have risen unabated since July as banks are more reluctant to lend to one another.

Source: Bloomberg

While leading economic indicators are collectively sending a strong message that we are likely to see the economy recover heading into 2012, there are no guarantees in this credit-crisis prone global economy, where financial trouble in one region can spread to infect the entire global economy. With the Euro zone representing the 2nd largest economic region behind the U.S., a significant credit crisis that in turn weighs heavily on its economic growth will not be without consequences to global economic growth. Thus, despite leading indicators pointing to a rebound in the U.S., any potential rebound may be killed by a further eruption of the European credit crisis.