Back in April, the world’s largest bond manager, PIMCO, made widespread news when it was announced that they were betting against US government debt (see article) by having a minus 3% of its $236B Total Return Fund in government securities. Bill Gross gave a few reasons why his bet against US government may be wrong and at the time I penned an article (Why Bill Gross is Wrong…In The Short Term) highlighting why I thought the risks to his bet were higher than they were predicting. My argument against shorting US government debt was chiefly based on the message of leading economic indicators (LEIs), which were signaling a slowdown in US growth, which would likely put pressure on equities and support for Treasury securities. Now, coming full circle, the message from the LEIs is that US growth is likely to accelerate into early 2012 which should lead to demand for stocks over Treasuries and now may be the time for Bill Gross to bet against US Debt.

Link between LEIs, Stock Prices and Bond Yields

Both the bond market and the stock market are both leading economic indicators. When a recession is right around the corner stocks often fall in anticipation of reduced economic activity, which in turn depresses inflationary pressures and bond yields fall. When a recovery is developing, stocks rise as do bond yields in anticipation of higher corporate profits and greater inflationary pressures. For this reason, LEIs such as the ISM Manufacturing PMI, which also leads turns in the economy, often move coincidently with stock prices and bond yields. This tendency is shown below with the twelve month rate of change (12-Mo ROC) in the S&P 500 alongside the ISM Manufacturing PMI. This linkage is quite clear and if the ISM is set to rise heading into 2012 then the 12-Mo ROC in the S&P 500 should also increase ahead.

Source: Bloomberg

With a potential increase in the Manufacturing ISM PMI heading into next year, bonds are likely to come under pressure as bond yields rise in concert with rising inflationary expectations.

Source: Bloomberg

LEIs Signal Recovery into 2012 – Bond Yields & Stocks Likely to Rise

Shown above was the close relationship between the annual return in the S&P 500 and bond yields in relation to the ISM Manufacturing PMI. If one had LEIs that lead economic turns even earlier than the ISM, or what I would call long-leading economic indicators, then one could likely have an earlier warning for coming turns in stock prices and bond yields. Back in April I presented three such long-leading economic indicators that signaled a sharp deceleration in growth and why investors should gravitate out of stocks and more towards bonds. These same indicators are presented below and suggest the economic deceleration in the economy should end in Q4 2011 (right now) and show a pickup in growth heading into 2012.

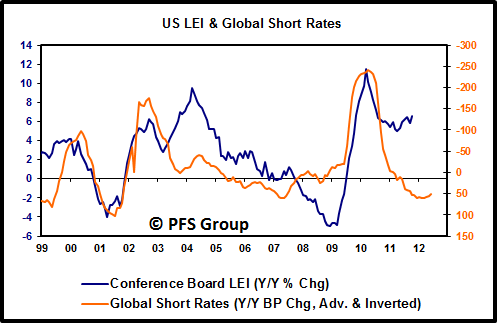

The first long-leading economic indicator presented in April was a look at global monetary policy, which is one of the greatest influences on the business cycle. When central banks lower rates commercial banks can garner a greater yield spread (borrow at low short-term rates and lend at higher long-term rates) and are more inclined to lend. More credit in the economy translates into more business investment and more consumer spending, both leading to greater economic growth. The impact from central bank policy often operates with at least a nine month lag and so looking at the change in central bank rates provides a preview of what one can expect for changes to economic growth nine months to a year out. Based on looking at the change in global central bank rates, US LEIs should be bottom now and slowly improving heading into 2012 as past interest rate cuts act as current economic stimulants.

Source: Bloomberg

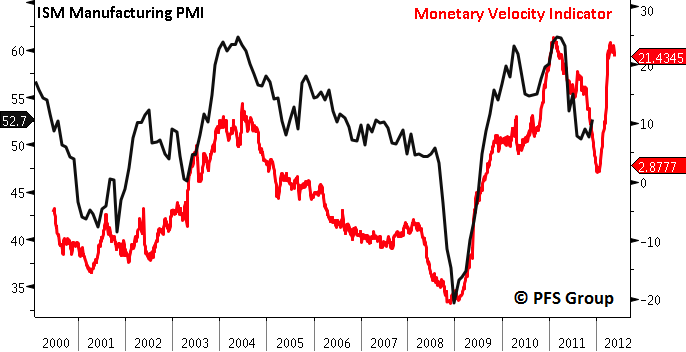

Another key long-leading economic indicator is the measure of money velocity moving through an economy. The greater flow of money from central banks to commercial banks and into the economy, the greater the economic activity. Based on our Monetary Velocity Indicator, which is shown advanced below, we should see the ISM Manufacturing PMI rise sharply heading into early 2012.

Source: Bloomberg

Another useful long-leading economic indicator is the relationship between certain sectors of the stock market. The relative performance of early to late-stage cyclicals typically provides a nine month advanced look at the trends in the ISM Manufacturing PMI. While in April the relative performance of early to late-stage cyclicals signaled a sharp deceleration in economic growth. However, the relationship between them now shows that the ISM should be bottoming now and sees a modest advance into 2012.

Source: Bloomberg

Did Bill Gross Make Two Mistakes?

Bill Gross came out in August and formally admitted he was wrong as a Reuter’s article points out.

PIMCO says betting against U.S. debt was a mistake

"When you're underperforming the index, you go home at night and cry in your beer," the Financial Times quoted Gross as saying. "It's not fun, but who said this business should be fun. We're too well paid to hang our heads and say boo hoo..."

He told the Financial Times that his view on the U.S. economy significantly changed earlier this month after the Federal Reserve promised to keep interest rates low for at least another two years earlier.

"Freezing rates for two years, that was a pretty significant statement in terms of the vulnerability of Treasuries to go down in price and up in yield," Gross said.

As of the end of 09/30/2011, Bill Gross’ flagship Total Return Fund had a 22.49% exposure to government debt as Gross went back into Treasuries after they had risen. With the LEIs pointing to an increase in interest rates over the next several months, it appears Bill Gross may have made a second mistake.

Summary

The chief reason Bill Gross was wrong on his bet against US government securities was his more bullish outlook for the economy than what transpired. Back in March long-leading economic indicators were suggesting a sharp deceleration in growth which indicated investors should become more defensive and shift out of stocks and into bonds. However, long-leading economic indicators are now signaling the opposite and suggest that investors come out of their investment bunkers (that is, overweight bonds/cash, underweight stocks) and transition their portfolio for a more optimistic economic climate.