It is almost like clock-work during earnings season that bearish-leaning commentators will find something to hang their hat on. A little over a month ago when the market was selling off, calls for a crash and coming bear market arose yet again and before the bears could blink the stock market indexes hit new all-time highs. Now, we are in the middle of earnings season and the grumpy old bears are trying to find something to be negative about, discrediting a decent earnings season by arguing that financials are carrying all the weight. "If you remove the financial sector, earnings stink," they say. Others cite lack of earnings growth and how the market shouldn't be this high now or going forward. I have a problem with both of these arguments.

First off, when does it make sense to strip out the best performing sector during any given earnings season? Why not strip out the worst performing sector or better yet, the best and the worst performing sectors. Stripping out the best performing sector to water down the market’s earnings makes as much sense as stripping out food and energy from the inflation rate. Last time I checked, food and energy were an important part of general living costs just as the financial industry is a major component of the economy; you can’t strip it out just because you don’t like the results. Imagine measuring GDP and stripping out states as if they didn’t exist: “While GDP was up ‘X’ percent over the past year, if you removed Texas and California the economy essentially went nowhere.” Or better yet, imagine a sports commentator saying that “The L.A. Lakers are really horrible if you take away Kobe Byrant.”

While it is true that the financial sector has had a large contribution to the great earnings season, that is only part of the story. For example, taking a look at total sales for the companies within the S&P 500 that have reported so far, while the financial sector is responsible for 63% of the aggregate sales surprise, the energy sector is responsible for 60%. Also, total sales for all sectors surprised this quarter even though the S&P 500’s biggest sector, technology at 18%, saw sales decline. Looking at the aggregate earnings surprise, the financial sector was responsible for 70% of the earnings surprise while the industrial, consumer discretionary, and health care sector made sizable contributions as well.

Source: Bloomberg

Even if you strip out the financial sector, you still have a pretty good reporting season. The biggest positive for sales was energy, which made up 161% of the aggregate sales surprise while industrials (20%) and consumer discretionary (41%) also made significant contributions. Turning to aggregate earnings surprises, the health care (64%), industrial (42%), and consumer discretionary (30%) sectors did the heavy lifting while the technology sector depressed earnings by 28%.

Source: Bloomberg

The financial, industrial, and consumer discretionary sectors are some of the most cyclical areas of the economy and that fact that they are leading is a good thing, something the bears fail to understand. What would concern me is if the bulk of the earnings and sales growth came from defensive sectors or commodity sectors, as was the case at the 2007 top, something which is clearly not occurring now.

The bears out there complaining about financials leading the market are likely the same bears who said that the market had it wrong in the first half of the year as the defensive sectors like health care, consumer staples, utilities, and telecom led. The argument is that defensive stocks lead at tops and their leadership meant we were heading towards one unless the cyclical sectors turned around. Well guess what? THEY DID! The industrial, consumer discretionary, and financial sectors are on fire and yet the bears are still finding something to be negative about, wanting to strip financial earnings from the earnings season.

First off, it is never wise to argue against what are perhaps two of the most respected market axioms: “Don’t fight the tape” and “Don’t fight the Fed.” Telling the market it has things wrong is typically a sign of bad planning or a failed prediction. That said, the market doesn't care what you or I think it should be doing. In the end, the market is simply a weighing mechanism that takes all the negative and positive inputs and tells everyone how they are balancing out. It really is that simple.

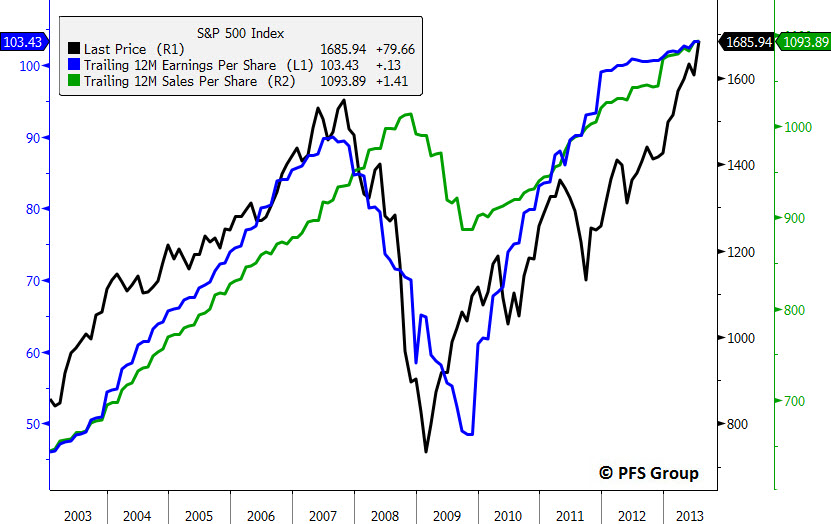

Some argue the market has it wrong and should not be rallying as strong as it is given weak earnings and sales growth. What these investors fail to realize is the market is a discounting mechanism and they are looking at things in the rear view mirror. The market moves based on expectations for future earnings, not on what earnings and sales were from a quarter ago. This is why the market LEADS earnings and sales. Don’t believe me? Just take a look at the S&P 500 below relative to its trailing 12-month earnings-per-share (EPS) and sales-per-share (SPS). You can see from the figure below that although the S&P 500 peaked coincident with earnings at the 2007 top, it did so well ahead of sales, and then also well before sales and earnings at the 2009 bottom. The fact that the S&P 500 is rallying is telling anyone willing to listen that earnings and sales for Q3 are likely set to accelerate.

Source: Bloomberg

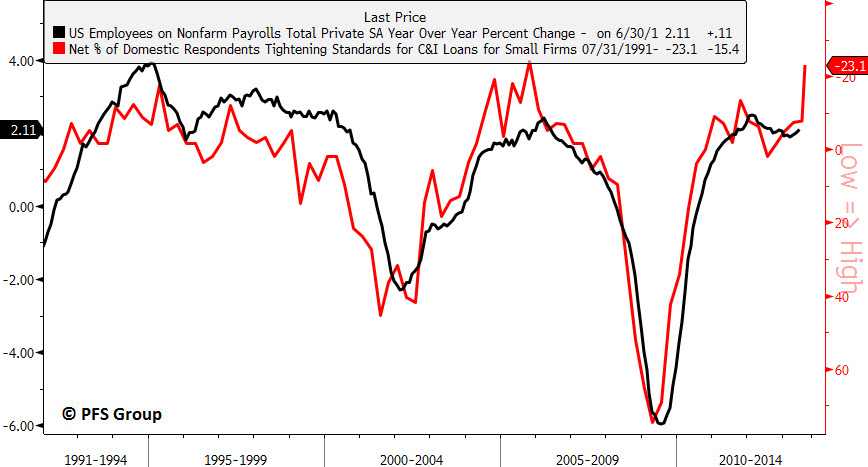

As I’ve stated several times in my writings, it is far more important to understand what the market IS doing than what you think the market SHOULD be doing. The market is rallying on a so-so earnings season mainly because it is discounting what is to come. As I’ve argued over the last two months, the economy should accelerate in the second half of the year and that is likely what is driving the market higher. As seen below, based on banks easing credit standards and making more loans, we are likely to see employment gains accelerate in the back half of the year. Given jobs are one of the key elements to any recovery, an acceleration in payrolls is very bullish for the market and economy.

Source: Bloomberg

Additionally, the health of our financial system is currently very strong as reflected in both the Bloomberg U.S. and Europe Financial Conditions Indexes, which just recently hit multi-year highs. Heading into a bear market and recession we typically see strains in the financial system begin to flare up as credit spreads widen. This was exactly the case leading up to the 2007 recession as the Bloomberg Financial Conditions Index for the U.S. and Europe peaked well before their respective stock markets did. Similarly, they both bottomed late in 2008, nearly half a year before the 2009 bottom. Thus, it is quite bullish that both stress indexes rest near their highs.

Source: Bloomberg

As long as the bears keep telling the market what it should be doing rather than focus on what it is doing, I believe they will continue to be consistently wrong and do a disservice to investors. Removing ego will help you be on the right side of the investment table far more than assuming you know more than what millions of market participants are doing, as the market is simply the aggregate sum of every investor's actions.