Since May 22nd the markets have been taking a much needed breather and have continued to cool off into this week. While the markets have had a mild pullback, there is nothing in the data below to currently alter our bullish outlook for the market and economy.

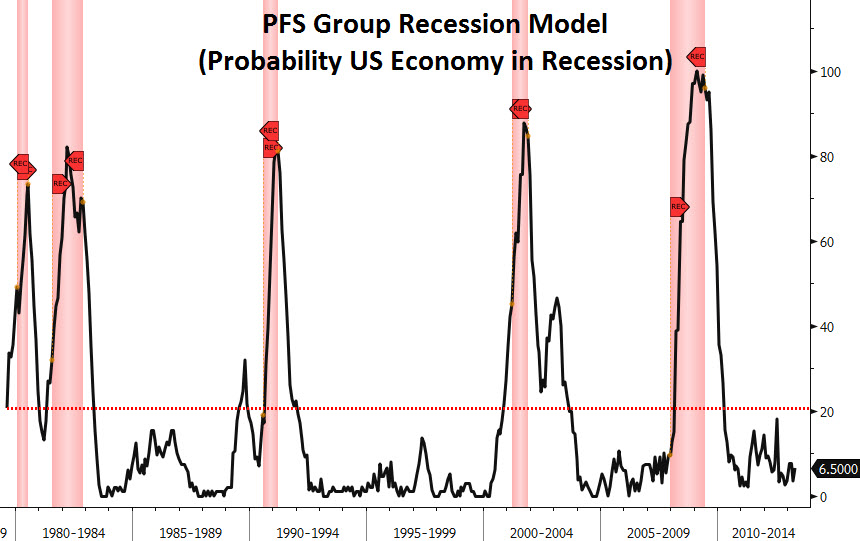

As seen below, our recession probability model suggests only a 6.5% chance that the economy is currently in a recession. Typically, leading up to a recession we see a sharp spike, which, along with others, is used for making necessary portfolio adjustments. At 6.5% and nowhere near the 20% threshold, the outlook for any major slowing in the economy, and potential drag this would place on the markets, is currently low.

There are two things we’ve written about months ago that we thought would be bullish catalysts for a strong second half of 2013. They are: a recovery in Europe and an improvement in US employment.

- Europe Should See a Strong 2H, Helping to Alleviate Global Growth Concerns (04/19/13)

- Leading Employment Indicators Suggest Higher Highs Into the Fall (05/15/2013)

Several pieces of economic data released this week suggest those two catalysts are beginning to play out. Eurozone industrial production (IP) came out this week and showed the recession in Europe is moderating as IP has been ticking up now for three straight months:

Source: Cornerstone Macro - S&P And EM Stock Markets Have Decoupled (06/12/13)

We were also treated to the Job Openings and Labor Turnover Survey (JOLT report) for the US which showed that job openings in the US are picking up steam, which is positive as job openings lead actual new hires and suggests we see accelerating payroll gains in the second half of the year:

Source: Cornerstone Macro - S&P And EM Stock Markets Have Decoupled (06/12/13)

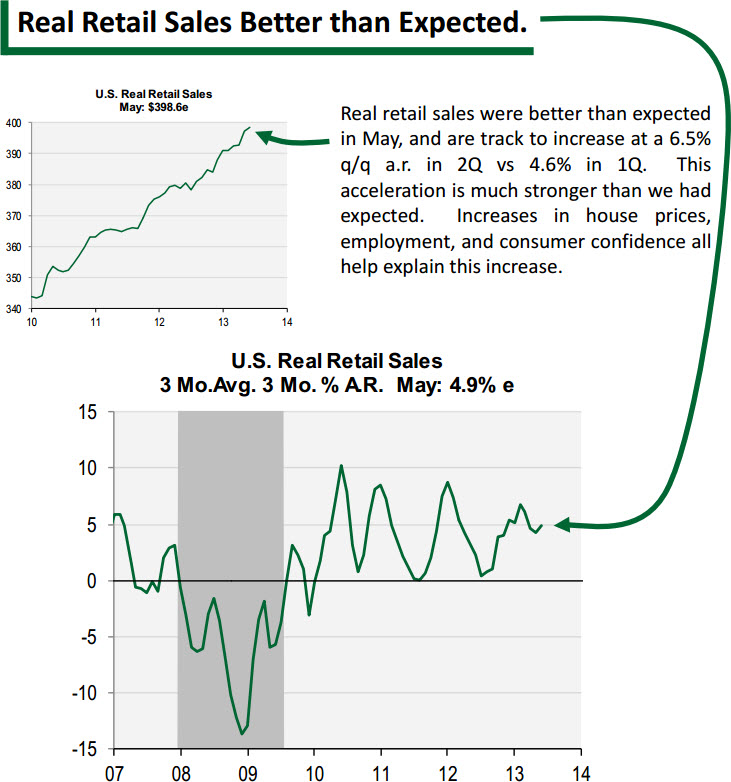

Employment gains are directly tied to retail sales growth and a pickup in employment suggests retail sales pickup. Given 70% of the economy is based on the US consumer, this bodes very well for growth ahead and yesterday’s retail sales report for May came out better than expected:

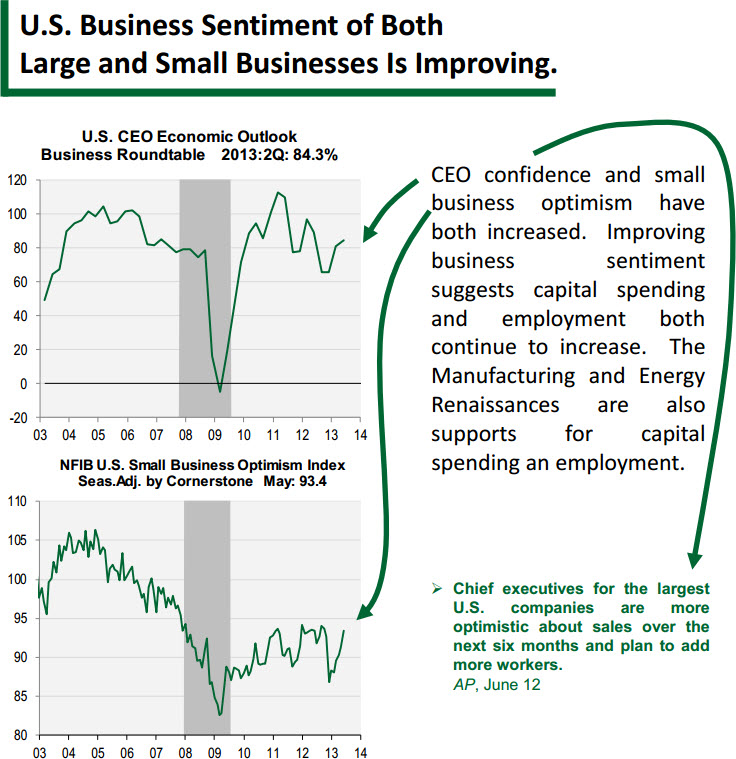

The improvement in the employment situation, easing credit standards by banks, and improving retail sales is leading to improved outlooks by large and small business:

One of the benefits of the current pullback has been a reversal in investor sentiment. The equity put-to-call ratio has reached levels associated with significant bottoms and is at the highest level since the June 2012 bottom.

Source: Bloomberg

In addition to the a high put-call ratio, the American Association of Individual Investor (AAII) sentiment report showed the percent bulls took a steep decline while the % bears picked up. This suggests a lot of the froth evident in the May peak has largely been worked off.

Source: Bloomberg

So, while we are seeing a bit of a breather in the markets, the underlining internals for the economy (and thus the stock market) are on solid footing and the thesis of a strong second half appears to be on track.