Last Monday, President Obama spoke at two town hall meetings. At the meeting in Canon Falls, Minnesota, he was happy to report to all those present that while financial markets were tossing about earlier this month, US Treasury prices were bid up by investors moving into “the best risk-free investment” there is. He claimed this was because investors still believe “America is one of their best bets.”

Mr. Obama is indeed correct; Treasury prices have gone up since the end of July. But the President failed to mention what has proven to be another of investors’ “best bets.” When compared to Treasuries, gold has been rising at an even faster rate. Gold and the 10 Year T-Notes have been moving up in price for the better part of three years. Still, since the Crash of 2008, gold has appreciated roughly twice as much as the 10 Year T-Note. With all the political bickering in Washington over raising the debt ceiling, traders kept bidding gold higher, and the S&P downgrade was just icing on the cake.

It is not at all surprising that the President neglected to mention gold as one of the “best bets” for Americans. The cap on interest rates until 2013 promised by the Federal Reserve essentially places a floor under bond prices. As Carmen Reinhart argues in her March 2011 academic paper, “The Liquidation of Government Debt”, the US Government can finance its debt by placing “caps on interest rates” and by creating a “captive domestic audience” to invest in US Treasuries. Negative real interest rates in the face of a steady, although not necessarily extreme inflation rate will conveniently eat away at the value of government debt. Reinhart labels this “financial repression”. It seems like lawmakers have chosen this strategy to manage the US debt, as it allows them to continue spending.

Naturally, the adverse effect of financial repression would be the surreptitious erosion of the value of the savings accounts of the masses. To baby boomers that are looking to retire, and to the working and middle class, this is financial repression at its finest. Those that are already retired and living on fixed income will likely be hit the hardest as the value of their incomes diminish steadily. With a good chunk of our economy already dedicated to the subject of legally reducing or avoiding income and other taxes, perhaps it would be prudent for Americans to make plans to avoid the inflation tax.

While gold is not a dividend paying investment, it acts as an alternative to dollar denominated savings and checking accounts. Obviously, Americans moving their savings into precious metals or foreign assets will not help the US Government in the quest to liquidate its debt. Not surprisingly, in the past we have seen numerous efforts by the US Government to monitor, tax, and restrict Americans’ ability to remove their wealth from the US Dollar system. More of this will most likely come soon. Reinhart acknowledges that the government would have to find some way of legally discouraging, limiting or outright outlawing investment in such assets for financial repression to effectively create a “captive domestic audience.”

Of course, it does not help politicians that gold has been steadily moving higher over the past several years. Recently, more and more people have come to see the yellow metal as a legitimate alternative to investments in US debt instruments. Bond prices are being actively and overtly supported by the Fed’s policy. Regardless of the many claims of de jure suppression of the gold price by the Fed and bullion banks, it is clear that policy makers deliberately avoid mentioning the metal unless they absolutely must.

Still On the March…Gold Seasonality and Equities

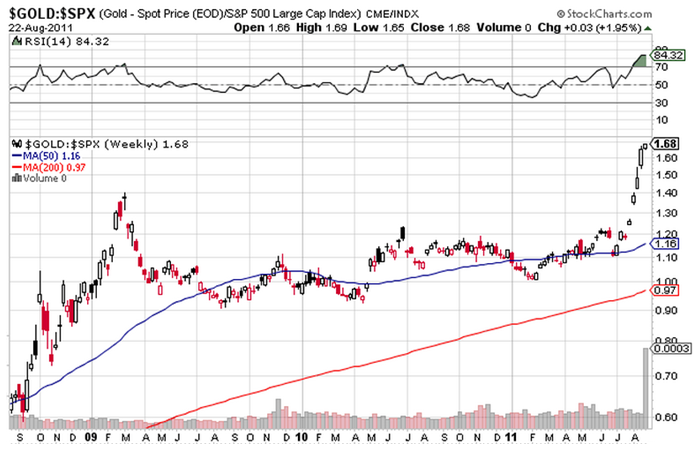

Numerous papers have shown a strong correlation between rising equity prices and the Fed’s easy money programs. What is interesting to note, is the current gold:S&P ratio. The ratio has been consolidating for more than two years since it fell from its high set in March 2009. It was at this moment when the Federal Reserve dispatched its first sortie of Quantitative Easing on the financial markets, when gold was at its seasonal weak point of the year. As a result, the gold:S&P ratio fell, due for a correction after doubling from where it was in the summer of 2008.

Contrast that scenario to the ratio’s rapid rise in recent weeks that broke through the previous high of gold set in March of 2009. Even after a solid rise, gold is entering the time of year where it tends to perform well. But now, the question is, would a call for more monetary stimulus from Bernanke at Jackson Hole or a promise for more QE in the near future send stocks higher at a faster rate than gold? Is further easing likely to cause even a short term reversal of the recent uptrend in the gold:S&P ratio as it did in 2009, when Bernanke’s helicopter first took flight?

Independent of whatever decisions the Federal Reserve Chairman makes at the annual banker retreat in the foothills of the Grand Tetons, gold is entering its seasonal “sweet spot” for the year.

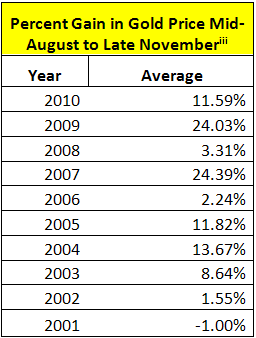

The statistics are pretty simple. Holding gold from mid-August to the last week of November over the past ten years yielded a positive return every single year, except 2001, when gold lost a grand total of 1%.

Since 2002, gold has averaged an over 11% return during this time period. Even during the commodities crash in 2008, gold managed to stay up over 3% from mid-August to the later part of November. Not much of a commodity, after all, is it?

Crisp and clear, gold is now entering its seasonal time to shine this month after rising for the past several weeks. The last spike in the gold:S&P ratio lasted over a period of six months, beginning in late summer of 2009. Given the recent breakout of the gold:S&P ratio above the 2009 high, it remains to be seen if gold will continue with its late summer/fall trend or if it will break its established pattern. Odds are, it won’t.

Disclaimer: I own both gold and US Government debt.