This weekend's Memorial Day holiday marks the unofficial start of summer. It is also the beginning of the Atlantic hurricane season which officially begins June 1st and runs until the end of November. The question many investors are asking right now: Is it time to "sell in May and go away?" Will the events of 2010/2011 be repeated again? Will the summer be sunny with mild balmy weather or tumultuous with thunderstorms, tornadoes and hurricanes? Our belief is that it depends on at least two main conditions:

1) Further policy responses

2) More positive economic news

The fate of global financial markets and economies are once again in the hands of policymakers. The third wave of global monetization is now coming to an end. The Fed's "Operation Twist"—switching short-term bonds for long-term bonds—ends in June. The Bank of England is easing off its latest round of quantitative easing, and the European Central Bank's LTRO program is now behind us. As the latest wave of global monetization ends there is growing evidence that the global financial system is once again hovering over a cliff. Policymakers are hoping the private sector will pick up the slack and no more stimuli will be needed. We see no evidence that the private sector is ready to step in and bridge the gap.

Europe's economy is now in recession, China's economy is slowing down, and recent economic news in the U.S. points to another soft patch. This leaves policymakers here in the U.S. with a choice to preemptively head off another downturn or wait for further evidence that the economy is in danger of heading into a recession. We are now at another tipping point where decisions will have to be made. Do we let conditions deteriorate and risk another global contagion or do we put out the current spate of brush fires before they turn into a forest fire?

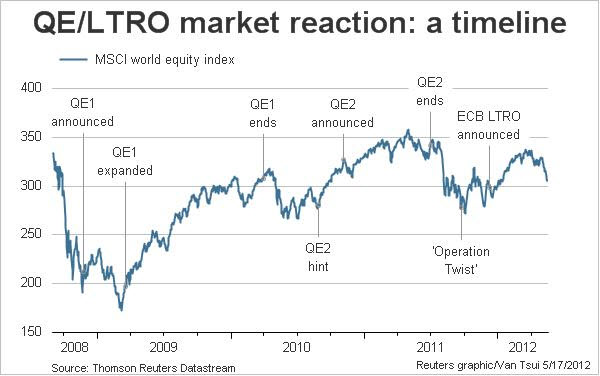

If recent history provides us with any clue as to the outcome it is that however the current crisis in Europe unfolds central banks will respond with more money printing. The next round of money printing will be global and it will be coordinated. The result is that the "risk off" trade will be reversed. Asset markets will respond and it will be back to the races again as shown in the graph below.

These are the issues that will need to be resolved in order to provide clarity to the financial markets heading into the summer and they will be upon us shortly:

1) Greek elections June 17th—will they exit the Euro or will they stay?

2) June FOMC meeting June 19-20th—QE3 or no QE3?

3) Supreme Court decision on ObamaCare

We would equate the current market environment to the events that precede a declaration of war. Prior to the declaration markets sell off due to the fears of uncertainty that precedes the breakout of hostilities. Once the war begins, and the bombs start dropping, the market stages a recovery because it is the beginning of the end. That is where we are now. The events above hang over the market and create unresolved uncertainties for investors. Once the monetary bombs start dropping that uncertainty will go away for a short period of time until the effects of the stimulus start to fade. This is a cycle that will repeat itself over the next decade as the process of deleveraging plays itself out and debts are paid down, defaulted upon on, restructured, or inflated away.

As Reinhart and Rogoff remind us in their highly acclaimed book, "This Time Is Different," deleveraging can last 10-15 years. Throughout history debt-to-GDP ratios have been reduced by: 1) economic growth, 2) substantial fiscal adjustment/austerity plans, 3) explicit default or restructuring of public and private debt, 4) a sudden burst of inflation, 5) a steady dosage of financial repression that is accompanied by an equally steady dosage of inflation.

In a recent interview in Barron's, Ray Dalio of Bridgewater Associates—the world's largest and most successful hedge fund—describes the various ways we are seeing deleveraging play out around the globe. According to him, there are three main ways this can play out: austerity, restructuring, or printing money. So far, Dalio believes the U.S. has done a "beautiful" job orchestrating this process:

A beautiful deleveraging balances the three options. In other words, there is a certain amount of austerity, there is a certain amount of debt restructuring, and there is a certain amount of printing of money. When done in the right mix, it isn't dramatic. It doesn't produce too much deflation or too much depression. There is slow growth, but it is positive slow growth. At the same time, ratios of debt-to-incomes go down. That's a beautiful deleveraging.1

It should now be obvious what the likely outcome will be going forward: more money-printing and more inflation—the very reason why Dalio is neutral on bonds as governments will print more money to keep real interest rates below the rate of inflation, a process that is called financial repression.

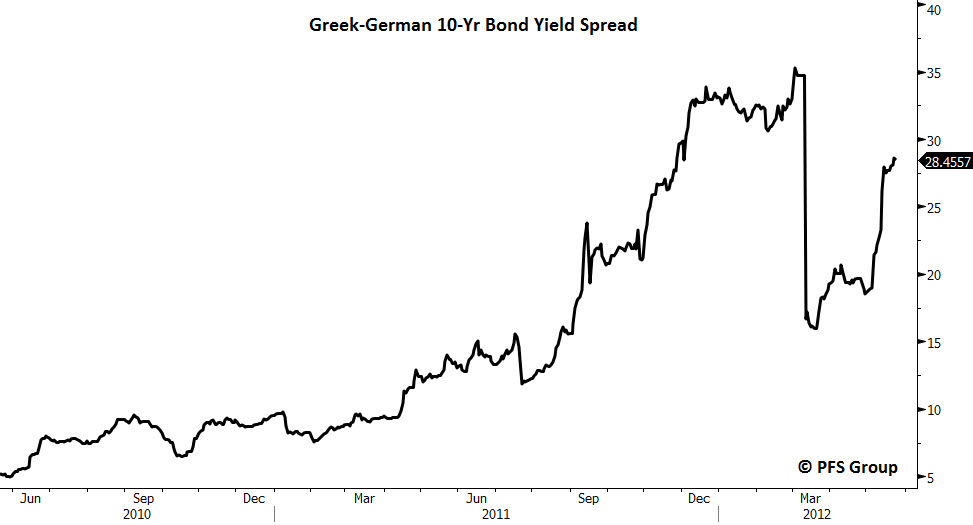

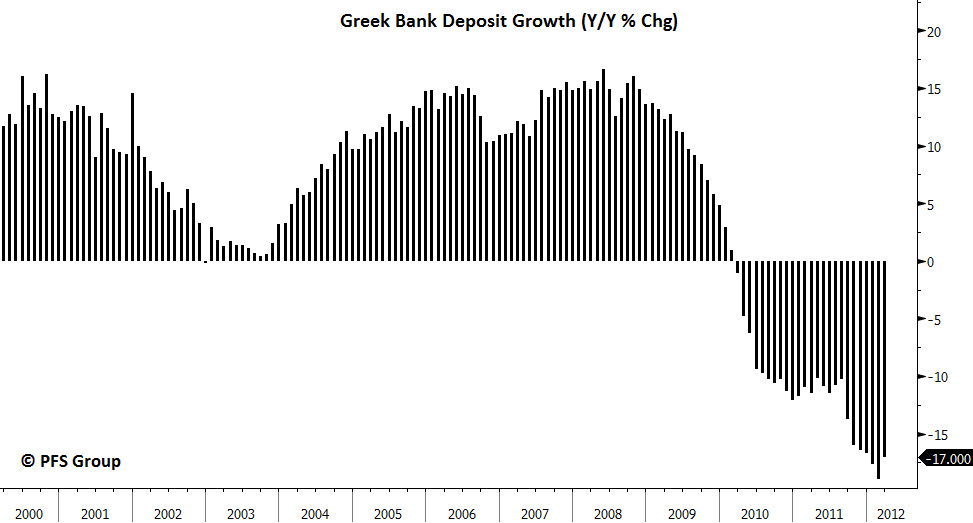

Now on to the crises that lie directly in front of us: Not since the days of Alexander the Great has the country of Greece had such a profound influence on the rest of the world. As my friend Don Coxe recently put it: today's Greece doesn't have an Alexander the Great to go in and straighten the mess out. Instead we have a hodgepodge of political hacks with no clear consensus. The only consensus seems to be to get your money out of a Greek bank—8 million in deposits have been withdrawn since May 6th. This leaves Greek banks even more dependent than previously on the European Central Bank to meet funding needs. The Bank of Greece has accumulated 120.23 billion euros in debt to the ECB through the Eurosystem payment network, known as Target2, because the country imports more than it exports. If Greece leaves the euro area, it may not be able to pay those euro-denominated debts.

What we do not know at this time is the outcome of those elections and how quickly EU policymakers respond to the unfolding crisis. Currently policymakers are looking to implement a line of defense around the fragile banking systems of Italy, Spain, and Portugal. There is talk of creating some form of deposit insurance to reassure investors as bank runs on these European banks have also begun. The 0 billion Greek economy plays a relatively insignificant role in the global financial system. The problem lies if a bank run followed by the exit of Greece from the euro zone could ignite a spark that sets off a similar bank run on healthy euro-area banks. If that were to happen it would require a massive response from the ECB.

There are two issues here: one is preventing a systemic banking crisis that could be triggered by a run on the banks and the other is to preserve the euro. Some form of deposit insurance would go a long way to curing worries of a bank run while the construction of a euro bond market would bring euro members closer to a fiscal union and deeper integration.

The problem with Europe is that they really don't have a country. Ray Dalio equates the current affair in Europe with the Maastrict Treaty that created the European Union and the euro currency to the U.S.'s Articles of Confederation. It wasn't until we created a constitution and a central government that we had the ability to tax, issue bonds, and borrow. Europe has neither of these abilities—it can't tax, it can't borrow, nor does it have a treasury that can coordinate fiscal policy.

The markets fear that a Greek exit would be equivalent to another Lehman-like event; however, there is a major difference today. A Greek exit could clear the air for the markets, which abhor uncertainty. Is the Greek crisis something new that the markets are just now discovering? The financial world is less leveraged today than where it was back in 2008 when Wall Street banks were leveraged 30-40/1. Many Wall Street firms, money market funds, and U.S. financial institutions have already divested much of their European debt. The Greek crisis needs to be put into perspective. Greece's GDP is around 0 billion a year. By comparison, IBM's free cash flow will be 0 billion over the next five years. Which matters more, a small economy or what major companies are saying about future income streams?

If Greece exits the euro and the ECB fails to act then there are other alternatives to deal with the crisis. We could see a massive coordinated intervention by the world's major central banks from the Fed, ECB, BOE, BOJ, and the PBoC. If the ECB fails to act on its own some form of rescue will be orchestrated between the Fed, ECB, and the IMF. Either outcome will mean another round of money printing, which is what the gold market may be sensing.

The next issue is what will the Fed do? We know that financial and economic conditions are now ideal for the launch of yet another round of quantitative easing. We now have the Bernanke Trifecta as my son, Chris, recently wrote in "Panic Like Its March 2009"—falling commodity prices, falling inflation expectations, and a weakening economy. I would add a fourth factor: a falling stock market. Do not be surprised if you wake up one morning and you see coordinated central bank action similar to the currency swap orchestrated between the central banks of the U.S., Europe, Canada, England, Japan, and Switzerland in November of last year.

The Fed could telegraph its move before taking action as it did in August of 2010 at the annual Jackson Hole conclave. Suffice to say the Fed has the tools as Fed President Narayana Kocherlakota reminded us on the day this was written in response to a reporter's question:

Reporter: Would you ever be in favor of adding accommodation?

Kocherlakota: The answer to this is simple: yes. If the outlook for inflation fell sufficiently and/or the outlook for unemployment rose sufficiently, then I would recommend adding accommodation. There are a number of ways that this could be done. My own preference would be for the FOMC to purchase additional Treasuries or securities issued by Fannie Mae and Freddie Mac in an attempt to drive down longer-term interest rates.2

In that statement you have the plan and the response. In addition, 2012 is a presidential election year. The Fed has four more meetings before the November elections: June 19-20, July/August 31-1, September 12-13, and October 23-24. If the economy were to continue to soften as it is now doing the Fed has June to react. Launching another round of QE right before an election would be seen as too political. There are currently a number of members of both parties in Congress that are considering legislation to reign in the powers delegated to the Fed. Ron Paul is not alone in this thought process.

There is another aspect to Fed easing that also has relevance to the economy and the markets going forward: There is a lag time between when monetary easing is announced/implemented and the time those effects impact the economy and financial markets. The impact on the economy from monetary policy lags by 3-6 months. The first area to respond to easing would be the financial markets. In fact, on the day this is written, the markets came back from an oversold condition to finish positive on the day. The turnaround was attributed to the comments made by Fed President Kocherlakota, highlighted above, that the Fed has the tools to respond to any adverse developments coming out of Europe.

The month of May has seen a number of weakening developments on the economic front. The regional manufacturing indices have been mixed, with many of them turning down or heading into negative territory. This could portend a drop in the national manufacturing index and indicate that we have moved back into recession territory. Also, the ECRI's Weekly Leading Index has fallen, the RecessionAlert Super Index is topping out, and the Wolfe Trahan WTLEI is heading down again.

Source: RecessionAlert

Source: Wolfe Trahan

This is not good news if you are the President of the United States running for reelection or the head of the Fed looking to get reappointed. That is why we believe we will see some form of policy response to weakening economic conditions both here and in Europe. This would line up with the global easing cycle which continues to unfold from China's central bank hinting at rate cuts and a reduction in bank reserves along with the IMF urging the BoE to cut rates, the UK government preparing a massive increase in government backed investment in housing, to Spanish Prime Minster Mariano Rajoy asking the ECB to buy Spanish debt. In conclusion, we think the stage is being set for massive coordinated intervention in the financial markets: translation, another round of money printing. In the larger scheme of things we think the condition of the U.S. economy is more important to financial markets than what is happening in Greece.

It wouldn't take much to change the market's current negative sentiment—an improvement in monthly payroll reports, continued improvement in housing and retail sales, or another surge in the LEI's could reflect a shift in the right direction.

From a contrarian perspective investor sentiment is at levels last seen during the bottoms of 2009, 2010, and 2011. Investors have been bailing out of stocks and putting money into bond funds at record levels. Wall Street strategists are as bearish as they were at the market's bottom in March of 2009. Given current economic conditions I believe the fear factor is overdone judging by the numerous references that we are approaching another cataclysmic event, a repeat of 2008 or, worse, 1932.

This brings me back to where I began. Will we repeat the downside performances of the last two years? It depends on policy response and economic conditions in the U.S. We are not as pessimistic as many current investment managers. I have often repeated the phrase the U.S. has the best looking house in a bad neighborhood. Ray Dalio at Bridgewater expressed it in better words than I could:

The economy will be slowing into the end of the year, and then it will become more risky in 2013. Then, in 2013, we have the so-called fiscal cliff and the prospect of significantly higher taxes, as well as worsening conditions in Europe to contend with. This is coming immediately after the U.S. presidential election, which makes it more difficult. This can be successfully dealt with, but it won't necessarily be successfully dealt with. We have the equipment and the policymakers, and as long as policy is well managed, we'll be okay.

In terms of the next crisis to emerge—after events sort themselves out in Europe—we have the upcoming fiscal cliff that takes effect January 1st of 2013. I suspect the thing President Obama wants more than anything else in this world is to get reelected. What the president will not want to face is another debt ceiling crisis in September and October right before the November elections. Another crisis he will want to avoid is a sharp stock market selloff this fall as investors contemplate a 67% increase in the capital gains rate, and a 200% increase in the taxes on investment income. Shrewd investors will start selling off shares long before voters hit the polling booth. A drop in the stock market similar to 2008 sunk John McCain's chance to become president. I don't believe this president will want to make the same mistake if he can prevent it. I suspect his strident ideological views will moderate the closer we get to the November election. The tendency for politicians is to move closer to the center the closer they get to the election. You may not agree with the president's economic philosophy but he must be given credit for being a very able and astute politician. The president's strength lies not in governing but in campaigning. He is known as the Campaigner in Chief.

That's why we expect some sort of "grand" bargain will be reached that will allow both sides to avoid the serious issues and postpone them until after the election. There are already plans floating in Congress from both sides to kick the can down the road. The best outcome would be to extend existing tax cuts and spending decisions for another year. Let the new president and new Congress sort out the problem rather than deal with another "Hail Mary" play in the final 7 weeks of the year.

We are hoping for the best but are prepared to take further action if policymakers sit on the fence. We remain alert and vigilant and are sticking to our discipline and models. You can expect further updates as events unfold as we step up communication to keep you ahead of the news.

From the flight deck,

JP

[1] Dalio's World, Barron's, Saturday, May 19th, 2012

[2] Thoughts about the Outlook, Narayana Kocherlakota, White Bear Lake Chamber Of Commerce, White Bear Lake, Minnesota