The good news this morning is that the 2nd estimate of the third quarter (3Q) GDP was revised up from 2.0% initially to 2.7%. This is up sharply from the 2Q print of 1.3%. As usual we will dig down into the numbers and look at the changes in the data but it is important to note that, as pointed out by Zero Hedge, Hurricane Sandy had NO EFFECT on the 3Q number as that event did not occur until the end of the 1st month of 4Q. The first chart below shows the gross change in the main components used for the calculation of GDP from Q2 to Q3.

The jump of .6 billion in 3Q was driven by a .4 billion increase in Personal Consumption (C), a .9 billion rise in Private Investment (I), .4 billion in Net Exports (X-M) and .3 billion in Government Spending (G). The next chart shows the percentage contribution to GDP that each of these primary components made towards the overall economy.

What is important to note is the large share, more than 70%, that the consumer makes up of the domestic economy. The purchase of services currently comprises more than 45% of consumption expenditures. The reason I make this point is that service related consumption has a very low multiplier effect in the economy versus manufacturing and production. The rest of the economy was driven by a 14.15% contribution of private businesses expending capital (notice that housing construction is a very small 2.72% contribution as I discussed yesterday), a negative 2.95% drag from net exports (exports less imports), and a 18.34% contribution from government spending which was primarily state and local.

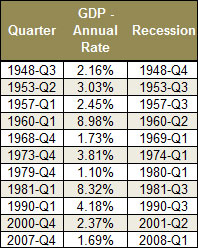

While this data is interesting it really doesn't us much. The immediate response by the media was that this report on economic growth was a clear sign that a recession was nowhere in sight. This complacency is somewhat dangerous because the economy is not currently growing at a rate strong enough to achieve the "escape velocity" needed to maintain sustained organic growth. While the economy is not currently in a recession there are two very important things to remember: 1) The NBER doesn't look solely at GDP in determining recessions and expansions but rather the trends of employment, production, retail sales and incomes, and 2) it is not historically uncommon for GDP to tick up just prior to a recession - particularly when the bumps come from inventory accumulation. The table shows the annual rate of GDP growth the quarter before the start of an official recession. Sustainability of current growth is the real concern as we go into 2013.

It is already estimated the Q4 growth in the economy will again contract back towards the Q2 levels of 1.3% as consumer spending continues to retrench. The chart below shows the trends of the PCE component of GDP.

The decline in the strength of consumption is of obvious concern when considering the weight that it carries within the economy. The data trends contradict some of the recent analysis from mainstream economists that have stated that "healthier household finances are driving gains in confidence and spending." While consumer confidence may have improved recently it is much less of a reflection on improved household finances but a testament to the psychological impact of the media on consumer psychology. While spending on goods, and durable goods, picked up in the most recent quarter it was not enough to offset the declines in services which, as shown above, is a large component of overall PCE. Furthermore, the surge in inventories, which is most likely unwanted given the weakness in consumer spending, was 90% of the Gross Private Investment component. The balance of the increase in GDP in 3Q came from government spending which has virtually a zero multiplier effect in the economy.

There was an anomaly though in the government spending component of the 3Q GDP. Of the .67% contribution to the 2.67% annualized economic growth rate - the entirety came from a massive surge in defense related spending. There are two issues with this: 1) in the previous three quarters defense spending was a drag on economic growth yet in the month just prior to the election defense spending has a massive .9 billion increase; and 2) manufacturers in the various regions should have seen increases in new orders and backlogs which hasn't been the case.

One explanation for the surge is that the government was spending dollars ahead of the fiscal cliff recognizing the future defense spending will be drastically cut. Considering that defense spending was a huge contributor to the current quarter growth - it doesn't bode well for economic growth in the future.

As we discussed recently in regards to housing the increase in residential investment did provide a bump to 3Q GDP - however, it is a relatively small impact to overall economic growth today versus where it was historically.

Prior to 1980 housing was a major contributor to the overall growth of the economy along with automobile manufacturing. That is no longer the case as services have become a much larger share of overall consumption and exports are comprising almost a 14% share of GDP. Even a doubling of residential construction from current levels will only return the contribution to the economy back to levels where it was previously seen during recessions.

Output Gap Still High

The output gap as a percentage of potential GDP did narrow this past quarter from 6.01% to 5.78%. The output gap, which is the difference between real and potential GDP, continues to run at levels normally seen during recessions. The problem is that it has been nearly four years since the peak of the previous recession and we are still at a very severe gap. A quick look at history tells you that something different is occurring this time within the economy which is why continued artificial interventions have been required to keep it afloat.

This output gap also shows up when looking at GDP from a per capita standpoint. My friend Doug Short stated in his analysis of real GDP per capita (I highly recommend you read his article) that:

"The real per-capita series gives us a better understanding of the depth and duration of GDP contractions. As we can see, since our 1960 starting point, the recession that began in December 2007 is associated with a deeper trough than previous contractions, which perhaps justifies its nickname as the Great Recession. In fact, at this point, 19 quarters beyond the 2007 GDP peak, real GDP per capita is still 1.45% off the all-time high following the deepest trough in the series."

Gross Domestic Income

Another big concern for the 3Q GDP is the decline in Gross Domestic Income (GDI). GDI is the total income received by all sectors of the economy including wages, profits and taxes less subsidies. In the latest quarter the annual rate of change in GDI rose at a 1.7% annual rate which was slower than real GDP. Since all income is derived from production (including the production of services) these two numbers should exactly equal. Furthermore, 2Q growth in real GDI was revised down to a -0.7%. History suggests that the weakness in GDI will lead to subsequent downward revisions to GDP growth in the future as shown in the chart below.

Real Final Sales

Lastly, the annual rate of change in real final sales of domestic product continues to decelerate and currently sits at 1.88%. Historically, when the annual rate of change of real final sales has been below 2%, the economy has been or was about to be in a recession.

The combination of rising levels of unsold goods (inventory), slowing sales growth and declining incomes all point to weaker GDP growth in Q4 and into the early quarters of 2013. Look for GDP growth in the 4Q to decelerate to 1.5% to 1.7%.

While there is currently not an official recession in the U.S. economy, as of yet, the details of the current economic growth are not ones of robust strength. Furthermore, we will have to wait for revisions to the current data until next year where we will see some of these anomalies revised away. With recent weakness in industrial production, capacity utilization rates and exports it is likely that there will be further deteroration of economic growth in the months to come.

If I am correct in my assumptions the economic underpinnings will continue to negatively impact fundamental valuations as profit margins continue to be compressed. Furthermore, the outlook by corporate CEO's for the next couple of quarters are not optimistic as top line sales and revenues slide. Any impact from the "fiscal cliff" or "debt ceiling" debate, a resurgence of the Eurozone crisis or some other exogenous event could quickly impact the markets.

While most of the media, and mainstream analysts, continue to focus on the state of the economy from one quarter to the next - the trend of the data clearly shows the need for concern. Of course, this also why Bernanke is already considering QE4. As I stated previously, while economic growth did pick up this quarter it is the makeup, and more importantly the sustainability, of that growth is what we need to continue to focus on.

Source: Street Talk Live