In today’s podcast, Patrick Nipper of Renaissance Macro (a.k.a. RenMac) cautioned listeners that a “global overhang of draining liquidity” is weighing on the markets and that when you look at the aggregate picture of global central banking balance sheets, liquidity conditions are now negative on a year-over-year basis.

But what about the recent monetary “bazooka” launched by the European Central Bank, you ask?

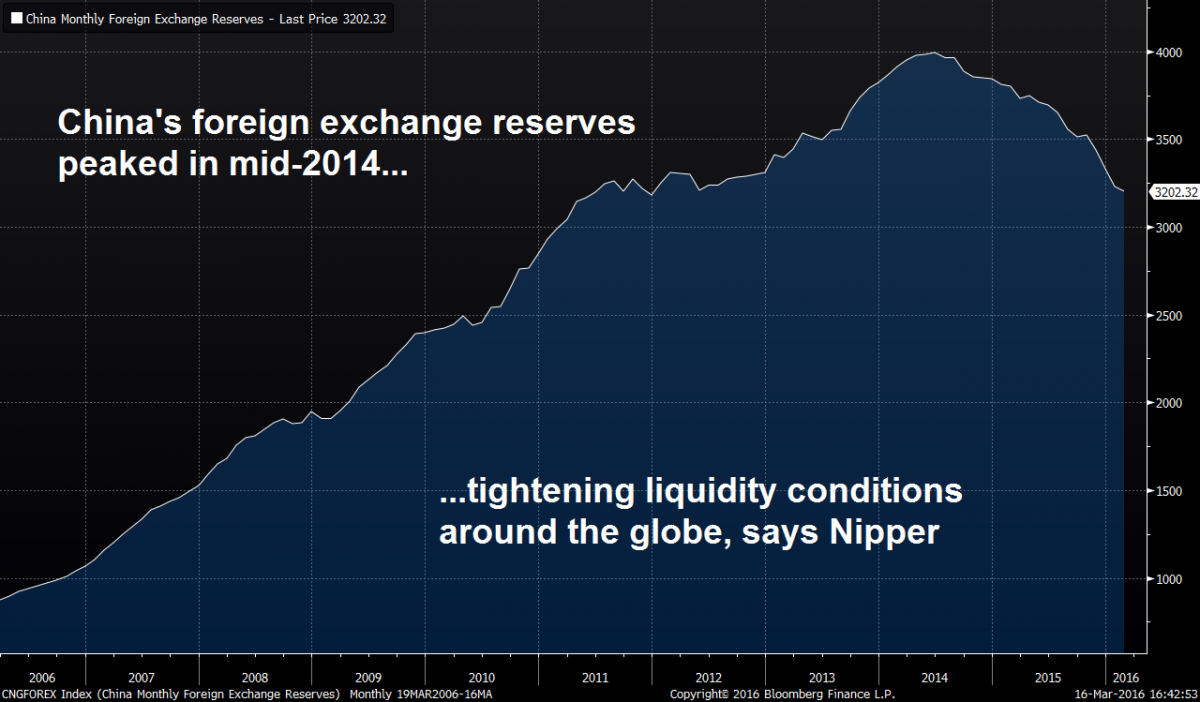

According to Nipper, what’s happening in China—particularly the continued drawdown of their foreign exchange reserves—is counteracting the efforts of other central banks to keep liquidity conditions favorable.

Nipper also comments on the message currently given by the credit markets—what he calls “smart money”—and says that although conditions have improved in the short-term, credit spreads (a measure of market risk) are still trending in an unfavorable direction.

Here’s some more of what Patrick Nipper had to say in today’s podcast:

“The tricky part of dealing with any bear market is when you have a rally like this and you have a lot of short covering, you do need to look and see what the credit indicators are telling you. And the reason we like credit so much is because it's not subject as much to retail psychology as the equities markets are.

So we look to see what the smart money in credit is doing and...we have seen some improvement off the lows...[but] they haven't improved enough to really break the downtrend that they've been in...so from our standpoint credit spreads have not come in enough to signal the all-clear for the equity market…

We're in a regime globally where liquidity is still draining and while Europe is adding as much as it possibly can—and certainly Japan is making a yeoman's effort at trying to boost markets through QE—it's really dwarfed by what you see coming out of China.”

Scroll down to read more of his comments, or click to hear a preview of his interview below.

“China’s foreign exchange reserve drawdown has been, over the last six to twelve months, as high as 0 billion a month. Now contrast that with the ECB's program of billion a month in euros, which can be as much as billion in US dollars; when you contrast that to the draining of liquidity that China is taking out of global markets, it actually overwhelms what you see Europe adding. So the net result of that is you have a global overhang of draining liquidity that makes it tough to make markets advance…

The situation in China is that as they slow down, China has become such a big part of the globe right now and their economy has grown so they are an important player much more so than they were 10 or 20 years ago and what you see is when they start to drain liquidity for their own domestic purposes—to prop up their currency for instance—capital is global, capital is liquid...it flows across borders and it really countermands the efforts of the ECB and the Bank of Japan and we've aggregated all this into a chart and when you add up what the Fed balance sheet is doing and the ECB's and the Bank of Japan's and China—both from a central bank asset standpoint and from an FX-reserve standpoint—and then you even throw in the size of sovereign wealth funds, and just aggregate together the size of a global central banking balance sheet if you will or global government balance sheet, it's falling and it's actually negative on a year-over-year basis…”

Listen to this full podcast with Renaissance Macro’s Senior Technical Analyst, Patrick Nipper, by logging in and clicking here. Not a subscriber? Click here.