Originally posted at Briefing.com

We didn't expect much out of 2015 from a price return standpoint and so far the S&P 500 has lived down to our expectations, declining 0.8% year-to-date. Unfortunately, we're not all that enthused right now by the return outlook for 2016 either.

Valuation is stretched, interest rates are moving up, earnings growth estimates are falling, and, frankly, we're not altogether confident in the Federal Reserve's more hopeful view of how things might unfold.

Throw in some increasing geopolitical stress, divergent monetary policies, widening credit spreads, narrow market leadership, and presidential politics, and you have some grey clouds hanging over the market as we enter 2016.

Those clouds could rain, they could pour, or they could pass by to give way to sunnier skies. We don't know for certain. Nobody does, because the future is inherently uncertain. That's why our forecast will be subject to change as 2016 unfolds.

What we see in the weather pattern today though leads us to think the barometric pressure is falling, and not rising, for the stock market. For those who may not know, falling barometric pressure is generally a harbinger of an approaching storm.

Stretched

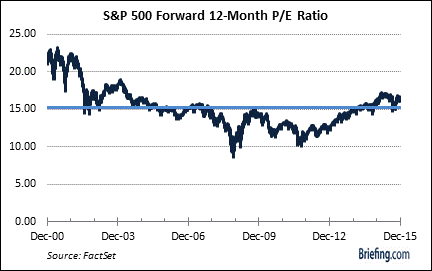

At recent closing prices, the S&P 500 was trading at 16.5x forward twelve-month earnings, according to FactSet. That's not an exorbitant valuation, but it is stretched relative to the 15-year average of 15.3x.

Others who follow Robert Shiller's cyclically adjusted price-to-earnings ratio, or CAPE ratio, will be quick to point out that it's more than stretched at 26x current earnings, which is a 56% premium to the long-term mean.

Whatever PE path one follows, the overarching point is that the stock market at current levels is fully valued at best and very overvalued at worst.

One can see in the chart below, too, that the forward multiple contracted over the course of the last tightening cycle which began in 2004.

We may not see the same type of multiple contraction we did in the last cycle if the Fed is able to follow a gradual path of tightening, but a faster pace of tightening would be more problematic.

Nevertheless, with profit margins near record highs, the dollar remaining strong, and global economic growth weak, the market is unlikely to be as willing as years past to pay up for each dollar of earnings with interest rates just starting to rise.

Said another way, we don't think investors will be willing to pay any price for growth in 2016 as they did with a number of market darlings in 2015.

Growth stocks may still be the preferred option if economic growth remains sub-par, yet we suspect the market will be more discerning with an approach of buying growth at a reasonable price (i.e. GARP investing).

If economic growth was to accelerate in a stronger-than-expected fashion, value investing could become—and probably should become—a more popular strategy.

The Big Risk

The issue of economic growth will be a key driver of things in 2016 given the related association with managing monetary policy. We know from the accommodative stance of the world's major central banks that the growth outlook isn't too stellar.

According to the Federal Reserve—the world's most influential central bank—the US outlook is looking better, so much so that the Fed moved the target range for the fed funds rate off the zero bound for the first time in exactly seven years this month.

It was a so-called "dovish hike," because it was accompanied by a contention that future rate hikes are likely to happen only gradually. If there is a key risk to the market in 2016, it is the Fed's approach to managing monetary policy.

If subsequent data show a marked deterioration in growth and/or inflation, the Fed will be accused of choking off the recovery effort by raising rates too soon.

If subsequent data show a much quicker pace of acceleration, the Fed will be accused of being behind the curve and will prompt concerns that it will have to raise rates faster than it (and the market) expected.

Check out: Preparing for the Final Phase of the Bull Market

The latter is the bigger risk, because the market is not buckled in to handle a faster pace of rate hikes. Having to take back the rate hike would be an initial disappointment, yet a move back to the zero bound we think would ultimately be viewed as a source of support—but from what level is the real question.

This goes to show how the Fed really needs to thread the needle with its policy approach to keep the market on a relatively even keel. That won't be an easy task with other central banks maintaining the status quo with their accommodative policy stances or making them even more accommodative.

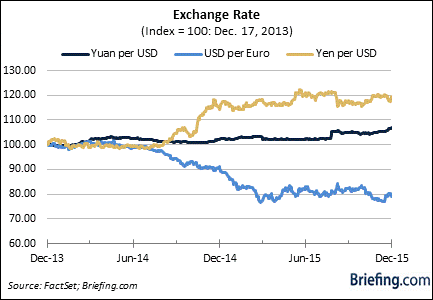

This divergence in central bank policies carries the potential to cause a storm in the currency markets if it leads to a continued strengthening in the dollar. That would rain further on commodity prices, emerging markets, and the earnings prospects for multinational companies—the combined impact of which would have a boomerang effect on the US stock market and severely challenge the Fed's assumptions.

There has been a lot of chatter in recent years about currency wars, yet there is latent potential in the depreciating yuan, the depreciating euro, and the depreciating yen to cause some currency and policy storms in 2016.

A Trend That Is Not One's Friend

We saw in 2015 how the strong dollar crimped the earnings prospects of multinational companies. A bullish view toward 2016 is predicated in part on a rebound in earnings growth that flows partly from a relaxation of the dollar's strength and a recovery in oil prices.

We struggle to see the dollar weakening to any great degree if other central banks keep their foot on the policy stimulus pedal while the Fed starts applying the brakes.

We know today that the consensus earnings per share (EPS) growth estimate for calendar 2016 is 7.9%, according to S&P Capital IQ. That sounds good relative to the 0.8% decline currently projected for calendar 2015. Then again, at the end of 2014 calendar EPS growth for 2015 was projected to be 8.8%.

The relentless slide in energy prices, and the hit to earnings for the energy sector, drove the downward revision for 2015.

At the moment, every sector, with the exception of the energy sector, is projected to deliver EPS growth in 2016, yet every sector has seen growth estimates come in since the start of the third quarter reporting period.

Source: S&P Capital IQ

We're not convinced given the weak global growth, the dollar's persistent strength, the consumer's newfound propensity to save more than he/she spends, and the ongoing decline in commodity prices that 2016 EPS growth estimates won't be subject to further downward revision.

This consideration is a main reason why we're not as enthused by 2016 return prospects as EPS growth estimates suggest we should be.

We could become more enthused with a reversal in earnings growth estimate trends and will watch that as a potential driver of an upgraded market view in coming months.

What It All Means

It is set up right now to be a tough investing environment in 2016.

The chatter heard today that it will be a stock picker's market is probably right. It sets up as such with the broader market's valuation already stretched and monetary policy moving from a coordinated approach to a less coordinated approach.

The volatility seen in the second half of 2015 is expected to carry over into 2016, with the movement in commodity prices, credit spreads, and incoming economic data playing a key part there since they will all influence the market's thinking with respect to the Fed's monetary policy approach.

It's a year that investors won't be criticized for starting in observation mode considering 2015 has been drawing to a close with more of a whimper in the stock market amid bangs heard elsewhere, which have included the Fed's first rate hike in more than 10 years, OPEC's recalcitrant stance and infighting on production levels, emerging signs of distress in the junk bond market, a terrorist act in France, and widely-held Apple (AAPL) flirting with entering bear market territory.

Read: US Corporate Earnings, Overseas Sales and the Dollar

Based on less accommodating fundamental factors, our view is that investors with a time horizon that doesn't stretch past 2016 should have a more conservative mindset when it comes to investing in the stock market.

That doesn't mean one should simply favor defensive-oriented sectors. It really means to be careful about picking and choosing your stocks in all sectors, and remembering that cash is an appropriate investment alternative at times to stocks and bonds. It also means the US stock market as a whole may not be the best place to look for excess returns in 2016.

Investors with a longer-term orientation have the implicit benefit of additional time on their side. That key element might allow for a more opportunistic approach that includes starting to build long-term positions in beaten-down areas like energy, materials, retail, and transportation. Still, the focus there should be on companies with the best balance sheets because the sledding could still be tough over the near term for these groups.

There are grey clouds lurking above, so don't forget an umbrella to protect you from any rain that might fall from them in 2016. In the meantime, I'll do what I can each week to keep you abreast of the changes I see in the weather.