Originally posted at Briefing.com.

Hillary Clinton is going to win the presidential election. That is the conventional wisdom these days anyway, which has been forged by a series of polls skewing in favor of Mrs. Clinton beyond the reported margins of error. However, what if those polls prove wrong? Obviously, it would mean that Donald Trump would be the next president.

Please hold your political feedback fire. Briefing.com doesn't take positions as a company in the market and we certainly don't take positions when it comes to politics.

Read Ugly! “Failure Almost Guaranteed” Regardless of Who Wins the Election

Our job is to analyze the capital markets. Accordingly, any foray into the political arena on these pages relates only to the impact political considerations appear to be having on the market.

And what we see in the market right now implies either that the market isn't totally convinced of the election outcome or that it isn't totally convinced anything really positive will come from the election.

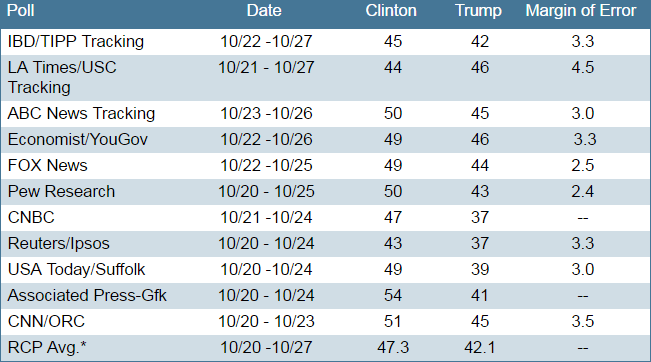

A Look at the Polls

First, let's take a look at some of the polls courtesy of RealClear Politics, which does a great job of aggregating the polling information.

Source: RealClear Politics (*Inclusive of other poll results not listed fully here)

The takeaway from the table above is that Mrs. Clinton leads in most polls; however, with Mr. Trump's numbers indicating a lead in at least one poll, and falling within the margin of error in a few others, the market has come to respect the fact that it can't necessarily take a Clinton victory for granted.

To be sure, it learned a costly lesson in the immediate aftermath of the Brexit vote when the polls, and the oddsmakers, leading up to the vote tilted pretty heavily in favor of UK voters electing to remain in the European Union.

Two Be or Not Two Be

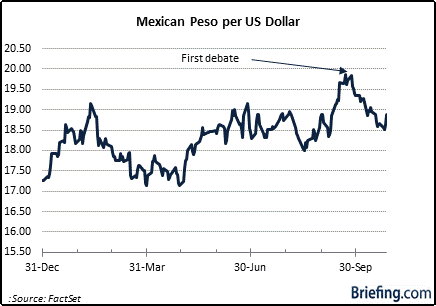

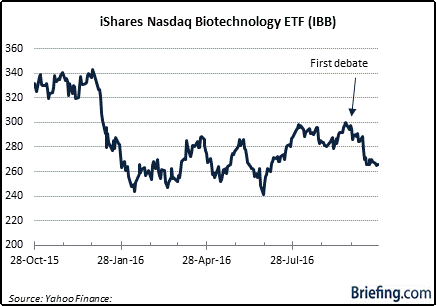

Many market pundits like to call attention to two indicators in particular that paint a growing belief in the prospect of Mrs. Clinton winning the election: the Mexican peso and the biotech stocks.

With Mr. Trump expressing a tough stance on immigration and a desire to build a wall on our border with Mexico—paid for by Mexico—the peso showed some noticeable weakening as Mr. Trump made his way to the Republican nomination and polled better leading up to the first presidential debate on September 26.

Read also Trump Destroyed Trump, Not the Media: “This Election Is Over”

Following that debate, however, the peso exhibited some renewed strength, which was construed by the market as a signal that Mrs. Clinton won that debate and improved her chances at being elected president. The peso has held the bulk of its gains following the first debate, yet it has begun to weaken again in the last week.

The biotech stocks, meanwhile, have not acted well since just before the first debate. Dating back to September 22, the iShares Nasdaq Biotechnology ETF (IBB) has fallen 14%.

That downturn has coincided with improving poll numbers for Mrs. Clinton, who has talked tough about reining in unjustified price hikes for long-available drugs. Furthermore, speculation has picked up that Democrats could potentially win a majority in both houses of Congress, thereby making it easier to enact price control legislation if Mrs. Clinton is in the White House.

Presumably, the biotech stocks would be acting better if Mr. Trump was thought to be the presidential frontrunner since he has not expressed a similarly hard view on price controls, although he has noted that he would favor allowing Medicare to negotiate drug prices with the pharmaceutical companies.

Setting political considerations aside, let's also not forget that the biotech stocks had a torrid run off the financial crisis lows, with the IBB gaining as much as 582% between its March 2009 low and its July 2015 peak.

Worries about potential price controls have been an overhang in the pullback from the July 2015 peak, yet valuation concerns and fear of crowded positioning have also to be accounted for in the retreat from those highs. In other words, it is easy to cite the political card right now when looking at the weakness in the biotech stocks, but it isn't just politics.

For instance, Illumina (ILMN), which is a top 10 holding in the IBB, recently issued a nasty revenue warning for its third and fourth quarters, and it doesn't even sell drugs. It is a provider of sequencing and array-based solutions for genetic analysis. Its stock dropped 25% the day after its warning, which had everything to do with weaker than expected demand and nothing to do with drug price controls.

We digress, so let's now look at the S&P 500 as a so-called election gauge.

The Other Side

In looking at the S&P 500 as a whole, it doesn't appear to be casting any clear-cut vote on the election outcome—certainly not since the first presidential debate, which was held after the close on September 26.

The S&P 500 closed September 26 at 2146.10. At its high on Thursday, October 27, it stood at 2147.13.

It is notable that the S&P 500 saw a quick selloff on Friday, October 28 when a headline hit suggesting the FBI is probing new emails written by Mrs. Clinton. One might cite that instantaneous retreat as an example of the market's belief in the idea that Mrs. Clinton is expected to win the election. Why else would it sell off if it didn't think this new investigation weakened her chances of winning?

That very response gets to the heart of why the market might also be bothered by the idea that nothing positive will come for the economy on the other side of the election.

Assume for a moment that Mrs. Clinton wins the election on November 8, and this new investigation isn't completed by then, but subsequently reveals some incriminating information. We heard one commentator suggest an impeachment proceeding would take place.

Talk of an impeachment proceeding right away for a candidate who hasn't even been elected president? It was a fitting observation for what has been a circus-like election season.

Another subplot in the market's post-election view is the notion that either candidate as president will push for fiscal stimulus to improve the nation's infrastructure. That sounds all well and good, but adopting a fiscal stimulus plan would mean issuing more debt. That issuance might not be tolerated well by the Treasury market, which is cognizant the US National debt is already at 106.5% of GDP.

A sudden spike in long-term rates following the announcement of a fiscal stimulus plan—assuming it even got approved by Congress—would be a counter-productive force for the US economy.

What It All Means

It's reasonable to argue that the stock market isn't convinced how this election will play out and that, even if it plays out in accordance with the conventional wisdom being dictated right now by the polls, that it will unequivocally mean good things for the economy.

That element of uncertainty is wrapped up in the objective data showing the S&P 500 is down less than 1.0% from where it was trading right before the first presidential debate and with its reportedly preferred candidate leading in most polls.

Over the same period, the market has had to deal with a Federal Reserve sounding as if it is primed to raise the fed funds rate again, long-term rates pressing higher, and building angst that central banks have hit their policy limits.

The conventional wisdom among the TV pundits is that a Clinton victory would be better for the market and the economy. Maybe. Maybe not.

What happens with interest rates and earnings growth has more to do with the performance of the market and the economy than who occupies the White House, particularly if the occupant of the White House doesn't have a political mandate with their party holding a majority in Congress as well.

That's a big reason why the market and the economy have gone up some years with both Republicans and Democrats in the White House and why the market and the economy have gone down some years with both Republicans and Democrats in the White House.

Politics have captivated the market for the last few months and have even transfixed it. There have been some not-so-subtle moves that have suggested this market is playing politics, yet the subtle action of the market overall implies an understanding that nothing is a given no matter who is reportedly leading in the polls and that nothing is a given no matter who is elected president.

That was a lesson learned with the Brexit vote.

What's a given (hopefully) is that there will be a president-elect on November 8. The identity of the victor that night could cause some near-term gyrations in the market—up or down—yet the true identity of the market beyond election day will ultimately be determined by the level of interest rates and earnings growth.