"The stock market is the story of cycles and of the human behavior that is responsible for overreactions in both directions." — Seth Klarman

Nearly three quarters of S&P 500 companies have reported Q3 earnings and so far results have been decent. As of Friday, 74% of companies that reported have beat earnings estimates and 53% have beat revenue estimates. This puts earnings growth at roughly 3.1% year-over-year if the trend continues. The big gripe that investors have been complaining about is the lack of revenue performance. Investors tend to rely more on revenue growth for indications that companies (and the economy) are expanding than on earnings growth. This is because earnings growth is easily manipulated by anything from cost cutting measures to accounting gimmicks.

As companies "lean-out" their income statements to drive earnings growth, labor is often one of the first places they look. Thus the need to maintain earnings growth on flat-lining revenues can add even more headwind to the employment situation.

I've been wondering for a while now whether the labor market problems are becoming more structural rather than cyclical. It seems the Fed and everyone else are convinced that all we have to do is get the economy growing again and jobs will abound. I'm not entirely convinced this is the case.

In a prior life, I worked in data analytics and statistical modeling for a large retailer. My team sat in the corporate offices and executed initiative after initiative to automate the decision making processes of various departments. Our goal was simple - leverage technology, automation and process improvement to make better business decisions with lower head count. Our efforts were often "sold" to the employees as a way to improve efficiency - and those in the affected areas were told that we were "freeing up their time so that they could focus more on strategy than on execution." That sounds nice doesn't it?

The point here is that every single company these days now places major emphasis on leveraging technology rather than labor. I'm not going to provide a lot of examples because I think this is self-evident, but there is one I'll mention simply for its obtrusiveness. Anyone driving through San Diego will notice sign-spinners on many street corners. Recently there has been a movement towards mechanical sign-spinners. These are machines designed as attention-grabbing females (mostly) that owners can place outside their place of business, replacing yet one more job.

I wonder where all this ends and whether someday even these sites will be written by a highly intelligent version of Siri (the digital personal assistant to Apple's line of products for you non-Apple fans). I also wonder whether this trend is adding fuel to the ever-increasing wealth gap in our country. It would only make sense since cash is being redirected from all the employees whose jobs are being replaced to a handful of owners of the corporations responsible for the replacing technology.

[Hear More: Barry Ritholtz on the Double-Edged Sword of Technology, Automation]

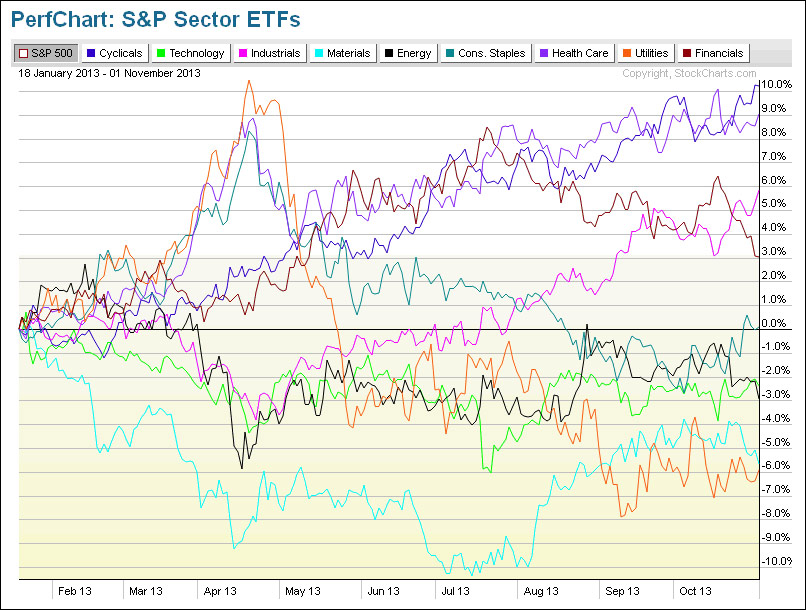

I thought we would take a look at sector performance for 2013 to get an idea of where money has been flowing. The chart below shows the performance of the S&P Sector ETFs in relation to the performance of the S&P 500. Sectors above the 0% line have outperformed the S&P 500 by the percent shown and sectors below the 0% line have underperformed the index by the percent shown.

As of yesterday, Cyclicals (dark purple line) have been the strongest performing sector year-to-date. This is a good sign if you buy into the general sector rotation thesis which underscores buying cyclicals when the economy is growing and moving money back to defensive names (like consumer staples, utilities) during economic downturns.

For those who need more logic behind this, the idea is that some companies like Ford will perform much better in a booming economy when consumers are spending heavily. These are considered cyclical companies because they tend to outperform when the business cycle is booming. Other companies, such as Proctor & Gamble, produce products (like toothpaste) which have relatively static demand regardless of where we are in the business cycle. These types of companies generally perform better in down economies.

So the fact that cyclicals are outperforming the more defensive sectors like consumer staples and utilities indicates that investors still anticipate growth in the economy. It is interesting to note the small and recent upward momentum in consumer staples. This could be a sign of a subtle change in investor sentiment as some anticipate slowing growth.

Health care is the number two performing sector this year and is likely to be a good performer for years down the road as the aging of America continues.

Utilities are the worst performing sector YTD which is indicative of investor distaste during a growing economy. But utilities have also been impacted by interest rate swings. Investors like utilities for their stable performance in down economies, but also for their yield. The increase in rates starting in May (see chart of 10-year Treasury Yield below) caused many investors to move funds away from utilities and into Treasuries - notice how the orange utility line above starts decreasing right at the beginning of May, corresponding to the rise in interest rates seen in the chart below. Why take on the additional risk of equities if you don't have to?

To read the rest of Richard Russell’s Dow Theory Letters and receive daily updates, click here to subscribe.