Derivatives Deconstructed

In a sense, the term “derivatives” has become a ‘catch-all’ to broadly define most, if not all, that ails our financial system.

Few people realize that derivatives have their roots in the agri-complex. From an historical context, it was agricultural commodities futures [mainly grain] that first gained traction as viable financial instruments. The genesis of these products dates back to the founding of the Chicago Board of Trade [CBT] in the mid-eighteen hundreds.

First and foremost, what is a derivative?

Derivatives are financial instruments whose values depend on the value of other underlying financial instruments. The main types of derivatives are futures, forwards, options and swaps.

The main use of derivatives is to reduce risk for one party. The diverse range of potential underlying assets and pay-off alternatives leads to a wide range of derivatives contracts available to be traded in the market. Derivatives can be based on different types of assets such as commodities, equities (stocks), residential mortgages, commercial real estate loans, bonds, interest rates, exchange rates, or indices (such as a stock market index, consumer price index (CPI) — see inflation derivatives — or even an index of weather conditions, or other derivatives). Credit derivatives have become an increasingly large part of the derivative market.

So, derivatives come in many flavors.

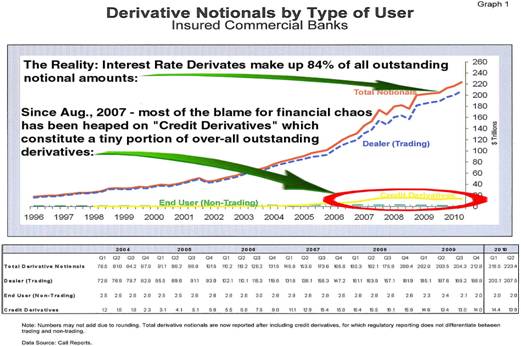

The Populist’s View

When the sub-prime crisis came to light in August 2007, much of the “blame” for our financial system melt-down was placed on the proliferation and reckless use of Credit Derivatives:

source: Comptroller of the Currency

The rise in the use of credit derivatives paralleled the rise in securitization of mortgages [credit derivatives were used to “guarantee” the falsified values of toxic mortgaged-backed securities –MBS]. But over-all derivatives growth was spiraling upward – despite there being no identifiable end users, on record, for these products] LONG BEFORE the advent and proliferation of credit derivatives. This was a tip-off that malfeasance was ‘already in play’. As such, credit derivatives and toxic MBS can be seen as more of latter day symptoms than a cause of what has so severely and systemically affected our global financial system.

The Real Derivatives Culprit

The true origins of our financial systems’ malaise can be better traced back to the Federal Reserves’ commandeering of the ENTIRE INTEREST RATE CURVE:

source: Comptroller of the Currency

Historically, the Federal Reserve ONLY had complete control of the VERY short end of the interest rate curve – specifically the Fed Funds rate [the rate at which banks and investment dealers borrow and lend to each other on an overnight basis]. But with the advent and proliferation of interest rate derivatives – specifically Interest Rate Swaps, many of which have imbedded government bond trades – concentrated in the hands of Fed proxy institutions – the Fed gained effective control of the “long end” of the interest rate curve.

Remember folks, the housing market and demand for housing is EXTREMELY sensitive to “LONG TERM INTEREST RATES” – not short term rates.

source: Comptroller of the Currency

Monetary elites at the Federal Reserve were well aware that irredeemable fiat money was SYSTEMICALLY FAILING as early as the mid 1990’s at the latest. At that time [being the devout Keynesians they are] the Fed and their partners at the U.S. Treasury – rather than admitting the serious failings of their Keynesian clap-trap - embarked on an undeclared war of economic market manipulation and malfeasance which fundamentally undermined the laws of usury. This dis-info war dictated that inflation rates and reporting would be falsified, employment data altered and hedonically adjusted, the gold price [the canary in the mine] artificially suppressed and currency values heavily manipulated / interfered with. This also sheds light on why the Glass–Steagall Act was repealed in 1999. Remember folks, the Glass-Steagall Act – at its roots – was designed to control / prevent speculation. As such, it stood as an obstacle.

The cost of capital, globally, is NO LONGER determined by economic fundamentals. The cost of capital is now ARBITRARILY set [owing to the fact that the U.S. Dollar is still the world’s reserve currency] in the offices of the Federal Reserve and the U.S. Treasury.

The fact that capital is fundamentally and grotesquely mis-priced “IS” the reason why the world’s capital markets have turned into speculative CASINOS. It’s the reason why so many different asset bubbles have developed. It’s precisely because the financial elites have debased the value fiat money itself – predominantly through manipulation / control of the usury mechanism itself – that our financial system has been so defiled.

The systemic financial FAILURE we’ve all been witness to is not and should not be construed as a failure of Free Market Capitalism. Instead, it should be seen for what it truly is – the manifestation of what results when Central Planning over-runs Free Market Capitalism.

Today’s Market

Overseas equity markets began the week on a negative note with Japan’s Nikkei Index gving up 25 points to finish at 9,401. North American markets did better with the DOW ahead 31.5 to 11.164, the NASDAQ ahead 11.46 to 2,490.85 and the S & P up 2.50 to 1,185.60. NYMEX crude oil futures added .59 to finish the day at 82.28 per barrel.

On foreign exchange markets the U.S. Dollar Index lost .30 to 77.08.

Benchmark interest rates – the 5 yr. gov’t bond ended the day at 1.17 % whiel the 10 yr. bond finished the day at 2.55 %.

The precious metals complex was broadly higher with COMEX gold futures adding 11.90 to 1,340.60 per ounce while COMEX silver futures gained .31 to 23.62 per ounce. The XAU Index added 2.80 to 199.62 and the HUI Index ended the day at 507.35 – up 7.29 on the day.

On tap for tomorrow, at 9:00 a.m. Aug. Case Shiller Index data is due – expected 2.0 % vs. prior 3.18 %. At 10:00 a.m. Oct Consumer Confidence data is due – expected 48.0 vs. prior 48.5. Also at 10:00 a.m. Aug. FHFA Home Price data is due – last reported [negative] -0.5 %.

Wishing you all a pleasant evening!