No one was prepared for the orchestrated take-down of the price of gold and silver in the first half of 2013. Forecasted supply was generously overstated while demand... grossly under-estimated. Thus, the tremendous imbalance had to be resolved which came to be known as "The Great Gold Heist of 2013."

Not only were the investors taken by surprise from the huge price declines, but so were the Fed and member bullion banks -- one by price movement and the other by huge demand. To understand why I believe there was a gold heist, we have to dissect through some of the just released official data.

Thomson Reuters GFMS just came out with their 2013 Gold Survey Update by providing interesting data that can finally shed some light on what will become an important pivotal point in history. While I realize many individuals are quite skeptical of the data coming from the World Gold Council and Thomson Reuters GFMS, at least we can make some key assumptions from these statistics.

[Hear More: Geologist Keith Barron: Gold & Silver Below the Cost of Production – Supply Crunch Ahead]

If we go back to Thomas Reuters GFMS 2013 Gold Market Outlook from earlier this year (April), here were their supply & demand forecasts. (Note: I will be referring to Thomson Reuters GFMS as just GFMS in the figures and article below).

GFMS Early 2013 Gold Market Outlook (in tonnes):

Mine Supply = 2,877

Gold Scrap = 1,754

Total Supply = 4,631

Fabrication = 2,404

Physical Bar = 902

Net Official Govt Purchases = 490

Implied Net Investment = 825

Total Demand = 4,631

As you can see everything has to match up nicely by the supply and demand figures balancing out in the end. I omitted the net-producing figure in the demand area of the equation as it was insignificant. These forecasts were released before the gold market take-down of April & June.

In their most recent Sept. 2013 Gold Survey Update, they released the following:

GFMS Sept 2013 Gold Survey Update:

Mine Supply = 2,917

Gold Scrap = 1,397

Net Disinvestment = 213

Total Supply = 4,527

Fabrication = 2,960

Physical Bar = 1,166

Net Official Govt Purchases = 361

Implied Net Investment = 0

Total Demand = 4,527

The Change in Forecasted Supply

You will notice several alarming changes in the forecasts. If we focus on the supply portion we can see that mine supply has increased a little, but the real surprise was the decrease in gold scrap. Earlier in the year, GFMS stated that gold scrap would total 1,754 tonnes in 2013. However, they revised it down a hefty 357 tonnes to only 1,397 tonnes for the year.

This is indeed a significant 8% decline in total gold supply that was not expected. More about the "gold scrap situation" later in the article. In addition, you will notice that a new category has appeared in the update that wasn't included in the prior supply forecast.

GFMS has now added 213 tonnes of net disinvestment as supply. Basically, net disinvestment is gold that has been withdrawn from institutional holdings and put back on the open market. Thus, total supply for 2013 is now estimated 4,527 tonnes -- 104 tonnes less than the earlier forecast.

If we look at the demand picture, this is where the real damage took place greatly motivating the bullion banks to increase supply.

The Change in Forecasted Demand

First and foremost, total fabrication is estimated to now increase a staggering 550+ t (tonnes) from 2,404 t (forecasted earlier this year) to 2,960 t by the end of 2013. Total fabrication includes industrial, jewelry & coin.

Furthermore, physical bar investment is now slated to increase from 902 t to 1,166 t for 2013. This turns out to be a 30% jump of physical bar demand than previously forecasted. Official Government demand is shown to decline by 129 t from the 490 t early forecast to 361 t now updated for 2013.

Lastly, the big change comes in the "implied net investment" category. GFMS originally forecasted implied net investment would be 825 t in 2013. However, they have revised this to be zero. Implied net investment is the exact opposite of net disinvestment. Which means, the estimated 825 t of this investment demand has just disappeared... or so it seems.

For GFMS to match their new gold supply and demand forecast of 4,527 t, they had to add 213 t of supply from institutional liquidations from sources such as gold ETF's and had to vaporize 825 t of implied net investment.

[Listen: John Kaiser: Gold Demand Hurt by Global Slowdown]

While the full year forecasted imbalances are significant, they are nothing compared to the huge dislocation in the supply & demand forces that took place in the first half of the year.

The Great Gold Heist: The Gold ETF Shake-Out

As I mentioned in the beginning of the article, investors were shocked by the huge decline in the price of gold whereas the Fed and member banks were completely surprised by the exploding physical demand.

GFMS originally forecasted for the first half of 2013 to be 1,501 t of mine supply and 736 t of gold scrap to equal a total of 2,237 t. Demand would mainly be 1,369 t of total fabrication, 170 t net government purchases, 441 t physical bar and 243 t of implied net investment to equal 2,237 t.

However, the huge decline in the price of gold had a serious impact on physical demand. Moreover, the falling gold price affected the gold scrap market as well.

The actual figures for the 1H 2013 were, mine supply of 1,416 t and gold scrap at 662 t for a total of 2,078 t supply (not including net disinvestment which was a staggering 456 t). Fabrication demand was 1,591 t, 191 t net govt purchases, 725 t of physical bar, and a zero implied net investment for a total of 2,533 t for 1H 2013. Again, I have left out a few tonnes associated with net hedging.

To get a better understanding of just how much more physical gold was purchased in the 1H 2013 than forecasted, let's focus on the main three categories. Net increases from fabrication were 222t, physical bar were 284 t and net govt purchases were 21 t which came to a grand total of 527 tonnes.

On top of that, actual mine supply fell 85 t and gold scrap declined 74 t for a total of 159 tonnes. Thus, the net change from supply and actual demand was 686 tonnes (527 demands + 159 loss of supply).

Where was the market going to find an extra 686 tonnes of gold lying around to meet this insatiable demand if available forecasted supply would fall short? In comes Gold ETF liquidations -- in mass.

According to the World Gold Council's Q2 2013 Demand Trends Update, liquidations from "ETF's and similar products" were 177 t in Q1 2013 and 402 t in Q2 2013 for a total of 579 tonnes. Of course this isn't the full 686 t shortfall, but it's a good place to start.

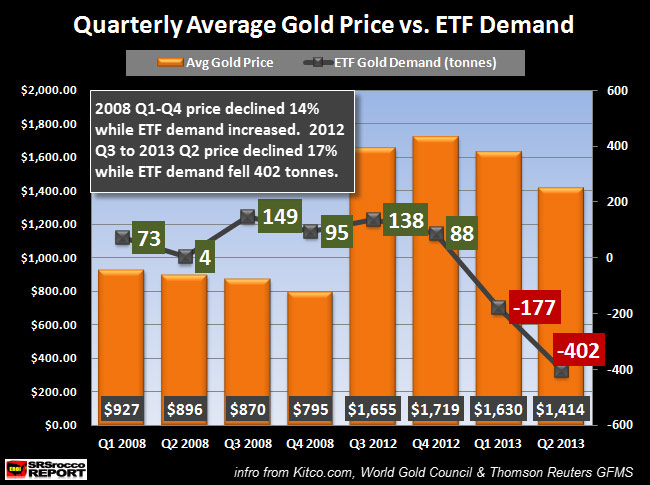

Looking at the chart below, we can see the change in average quarterly price of gold compared to the change in net gold ETF flows:

In order for the bullion banks (custodians of many of the gold ETF's) to get additional supply to meet the huge demand coming mainly from China & India, the market scare tactic of announcing a "sell recommendation", while covering record shorts was utilized.

As individual and institutional investors saw the price of gold getting relentlessly hammered, they sold out of their positions which allowed the bullion banks to cover their shorts and to liquidate much-needed physical bullion from the GLD & other ETFs.

However, a price decline of the magnitude witnessed during the first half of 2013 did not have the same market reaction of huge ETF withdrawals during 2008. If we look at the chart above, we can see the average change in price of gold compared to the net change in gold ETF flows.

In 2008, gold hit an average high of 7 during the first quarter, while flows into the gold ETFs were 73 tonnes. But, by the end of 2008, the average price of gold had fallen 14% to 5 whereas the total gold ETF levels actually increased 95 tonnes.

On the other hand, things were much different in 2013 when the average price of gold only declined 3% more than it did in 2008 at 17% from an average of ,719 Q4 2012 to ,414 in Q2 2013. In 2008 a 14% decline in the price of gold resulted in a positive flow of gold to the ETFS, while in 2013 a 17% change culminated a staggering 579 tonne outflow.

Of course the banks and official gold sources stated that the reasons for the huge liquidations of gold from the ETFs were due to the "end of the gold bull market" or the threat that the Fed would start pulling back on the "Infamous Tapering." While this rhetoric makes sense to the uneducated investors who are not privy to the fine art of precious metal manipulation, the end result was the same.

Again, the price decline in 2008 (,011 - 2) was about 30% from high to low, exactly the same percent change as in 1H of to 2013 (,694 - ,192). So, how do you motivate investors to sell their gold positions... you put the fear of god in them -- or should I say, the devil.

Without the huge 579 tonne liquidations of the gold ETFs, the market would have not been able to satisfy the massive physical demand. Moreover, the Comex gold inventories declined approximately 3.5 million ounces since the beginning of the year which added another 100+ tonnes of needed supply. With the added liquidation of the Comex gold inventories we are now getting closer to 686 tonne shortfall in supply.

The paper gold cartel was able to orchestrate the liquidation of the gold ETFs to satisfy the huge physical demand, but this was a one time event. Furthermore, there is another aspect of the gold market that will put more pressure on the supply-demand equation going forward.

The Continued Decline in the World Gold Scrap Supply

Many thought as the price of gold increased, we would see more in the way of gold scrap to come on the market. Unfortunately for those who were counting on this to occur, it has not been true. The chart below shows the decrease of gold scrap since 2009.

Here we can see world gold scrap has declined from 1,735 tonnes in 2009 to only 1,591 tonnes in 2012. Thus, total scrap supply actually declined 8% as the price of gold increased 72% from 2009 to 2012.

Adding insult to injury, first-half 2013 gold scrap supply declined 110 tonnes (14%) to 662 tonnes compared to the same period last year. GFMS forecasts that total gold scrap will reach 1,397 tonnes in 2013. This means they expect gold scraps to increase to 735 tonnes in the second half of 2013. What happens if they are incorrect and the actual figure turns out to be about the same or less than the first half?

If the market didn't show an increase in total scrap when the price of gold increased 72% in three years, why would it expect it to increase on a 17% average price decline? The very real problem the world is now facing is that it's running low on supplies of available gold scrap.

I believe gold scrap for the second half will be closer to 650-675 tonnes which would put the total for 2013 to be approximately 1,337 tonnes, or 60 t less than forecasted. Either way, if GFMS is correct and the market does supply 1,397 tonnes of gold scrap in 2013, it's still nearly 200 tonnes (12%) less than it was in 2012.

The Gold Cartel's Days Are Numbered

The proof is in the pudding, without the huge liquidations of the gold ETFs along with additional supply from warehouse stocks, there wouldn't have been the available supply to meet the massive physical demand coming mainly from the east. The huge take-down in the price of gold directly impacted demand -- it exploded.

While the MSM still regurgitates that the gold bull market is over and much lower prices are on the horizon, the global economic and financial system continues to disintegrate. The only thing keeping the fiat monetary system afloat is faith, deceit and more faith.

The rhetoric that the Fed might taper, won't taper or will taper is totally meaningless in the end. It really doesn't matter what the Fed does to be honest, the seeds of the destruction of the fiat monetary system have been sown years ago. While it becomes extremely frustrating to watch and listen to grown adults continue to lie as well as fabricate economic data, no one can hold back fundamentals forever.

The world is waking up to the fact that fragile financial system cannot be trusted to continue as it has in the past. There are way too many debts and worthless pieces of paper garbage floating around that have no real backing. Even though the paper gold cartel has been able to pull one over on the public this time, it's a trick that cannot be repeated.

The days of the paper gold cartel are numbered.

Additional note: Energy is the major factor that will impact the economy and financial system going forward. Shale oil and gas are only temporary fix to keep the world believing business as usual will continue. I will be publishing updates on how energy will impact the precious metals, mining and overall economy at the SRSrocco Report.

Comments are always welcome at SRSrocco @ gmail.com