Technology is moving to disrupt as many business models as it can and investment banks are not immune, an August 26 91 page Bank of America Merrill Lynch report points out. Banks in the European Union are struggling with different challenges than some of their US or Japanese counterparts. Inside banks, there are emerging approaches that differ from one bank to the next which can primarily be described based on how technology spending is categorized. It is this approach to managing the future and embracing or rejecting technology that could determine winners and losers in a segment beset by relatively low stock price-to-book value multiples.

Banks have been the only stock category trading below book value

In a stock market environment where banks are trading below book value — the only industry group to be doing so, as we have noted in ValueWalk — bank managers are searching for a solution. That solution could be found inside a powerful societal trend: eliminate humans and replace them with technology as the robots come for the jobs.

The major investment banks will not be the first in financial services to go down this path. It was the human trading floor that was first automated — most notably pushed aside by high-frequency trading. What resulted was a market structure where information traveled around the world in microseconds, the subject of a pitched battle at the Securities and Exchange Commission over the IEX Exchange. The next real battle that matters to banks is trading in SWAPs, which firms such as Citadel and Bloomberg are both looking to automate. Speed is one part of the technology-driven formula to reduce costs at major investment banks, but the exchange clearing systems typically also include the risk management benefit of the organization facilitating the trade not facing directional market risk.

Read Podcast: Quantum Computing Takes Flight

The August 26th 92 page BAML report, “Optimus Primer: how technology is transforming the investment bank,” touches on these issues but goes deeper. While it explores the time advantage, focusing mostly on European banks, it raises issues that apply regardless of geography. (The benefit of clearing swaps on a central exchange was not discussed in detail in the bank report.)

Robotics are a societal trend and banks can leverage IT to reduce costs 4% to 12%

The report documents the societal trend, part of their thematic work on millennials, that shows a preference for robotics despite concerns over cybercrime. In the financial services industry, it is witnessed in the rise of roboadvisors and low-fee Exchange Traded Funds over active mutual funds.

With general consumer preferences tending to favor robotic interactions as a powerful trend indicator, the report is about more than consumers. Perhaps the most material point is how technology can be used to reduce overhead burden and immediately improve the rate of return to shareholders.

Read also AI Advances Hint at Neural Networking Future

“Industry estimates have suggested savings could be significant,” the report said, pointing to areas automation disruption areas. “The status quo has a multitude of duplicated systems and processes that need humans to operate, maintain and reconcile them. Automating much of this process could yield substantial IT and staff cost savings.”

BAML estimates that by deploying innovative technologies it could cut costs anywhere from 4% to 12%. “An 8% reduction in group costs improves RoNAVs by 2-3%,” the report noted. But one of the problems with the cost reductions in a stock market world driven by quarterly earnings is that “some technology solutions seem long-dated.”

Banks are not embracing technology to revolutionize their business

With such a rich estimated return, one might think the banks would all be moving in unison. But they are not, the report noted.

The majority of bank IT spend, nearly three in four dollars, is directed towards maintenance, while a smaller percentage directed towards innovation. The banks have been under criticism for their failure to innovate, and the tech spending points to a divergence in thought process among the largest European players.

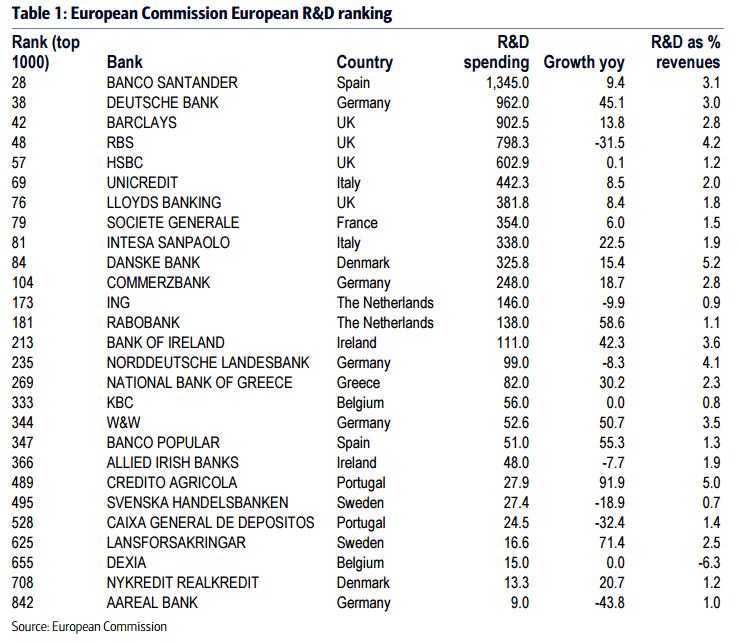

Banks at the top of the list in IT spending include Spains Banco Santander, Deutsche Bank, Barclays, RBS, and HSBC, with significant differentials in technology spend from top to bottom. France’s Societe Generale, for instance, spends 4 million on technology, 79th on the global spending list, while Banco Santander spends near .3 billion, at the top of the IT list. Numerous areas of cost reduction in bank process could be impacted:

Artificial intelligence comes in many forms which may be useful to banks. At the extreme, it can replace many functions currently carried out by humans. Key uses will be populating Big Data sets, carrying out maintenance reports, corporate audits, monitoring of conduct, compliance, risk, and trading.

Check out Matthew Mather's Darknet Shows Reality Is Not Far From Fiction

A large portion of technology spend cost reductions come in the compliance department, with automated systems monitoring and flagging inappropriate behavior at a significantly more efficient rate than humans:

…if a trade looks odd, if there is a problem, if the trade looks very different to how that client normally trades. Machine learning may be able to automate and resolve many of the issues, referring fewer exceptions to the trader.

The report, using “the industry rule of thumb” that one-third of all investment bank costs emanated from the back office, says this area could be best automated. Citing a study from SantanderInnoventures, BAML points to 20-50% of back office clearing and settlement costs could be eliminated with technology, for example. Technology and artificial intelligence solutions could also monitor trading and asset transfer regiments for red flags, tasks now monitored by humans.

Bank research could be automated — including the filtering of reports for the buy-side — but will research results ever be tracked?

One area that could be impacted is bank research, a notable topic of interest. Those inside bank profit centers have had research costs assigned to their division balance sheet. Bank research is projected to be a cost / revenue center of its own, with buy-side clients paying for the research. This will create an interesting dynamic where the valuable research will be identified through a free market system rather than the somewhat socialistic system where bank research is less accountable as a clear bottom line revenue generation number.

From BAML’s perspective, automation first streamlines the compliance function:

Research is a heavily regulated area with each regulator applying its own set of requirements. There are a myriad of regulations which require research divisions and its analysts to operate specific procedures to protect the quality of the research output. Analysts are generally required to distribute their views simultaneously to all their clients to prevent selective dissemination. That includes the salesforce and/or clients of their own firm.

This can take up valuable time (as the analyst works out the consequences of an economic event, finds relevant data, makes some charts, and then edits and publishes a report).

Not only will technology streamline research production, but also how it is consumed. Buy-side analysts are inundated with research. Technology could be used to help organize and differentiate among research thesis and information.

Could advanced technology — gasp — lead to success tracking of a researcher’s thesis, predictions, and modeling? While this might be a great fear among researchers — rarely is the success of their analysis fully tracked — it could likely separate the research wheat from the chafe. There will be winners and losers if this occurs.

Citadel and Bloomberg looking to disrupt traditional investment banks while investment banks pushing back in other ways

A new paradigm is reshaping banking and certain industry innovators are gunning to disrupt the status quo. The BAML report highlighted three primary forces targeting technological improvement that included two well-known names: Citadel and Bloomberg.

Some non-bank competitors have been far more successful than the banks in pushing down variable cost per trade which has allowed them to creep into areas that have traditionally been fulfilled by banks. New entrants have the luxury of building their infrastructure from scratch for the new rules, rather than needing to make alterations to legacy systems. Well-known examples include Citadel which has pushed into the trading of liquid, standardized swaps, or XTX which ranked top 10 in the latest Euromoney survey for FX trading. Bloomberg is also making in-roads into being a SEF in CDS and also encroaching into some of the traditional sell-side research roles of providing analysis of standardized data sets through Bloomberg Intelligence.

And the report also notes:

The tools of research broadly similar for 10 years – expect this to change A decade ago, the main tools of the average analyst were Excel, Word, email, pdfs, Bloomberg chat and a phone. Today, these are pretty much the same. Client relationship management systems are better, more integrated and matter more than they did 10 years ago. But essentially, the tools are unchanged. Meanwhile, Facebook has grown from 6m monthly users in 2005 to 1.6bn in 4Q15. In 2005, the best-selling phone was a Nokia 1110; the iphone was a mere glint in the eye of Sir Jonathan Ive (1st gen not launched until 2007); 2MB broadband had just been launched for UK households (now 100MB is fairly standard). The word “Fintech” would certainly not get past the editors.

It seems likely that research will need to make faster technological progress over the next decade. In our view, as the value of Research becomes more clearly defined, there is the potential for a raft of changes.

Perhaps in the behind-the-scenes race to watch will be who disrupts whom first? Will Bloomberg disrupt the banks first or will the banks disrupt Bloomberg?

By Mark Melin