One of the world's most powerful supercomputers, retrofitted for trading the stock market, appears to be betting on a crash in the months ahead.

The Financial Crisis Observatory (FCO) at ETH Zurich released its latest Global Bubble Status Report on July 1st. As we discussed with FCO’s director, Didier Sornette, on our podcast in May, they use one of the world’s leading supercomputers to monitor global markets each day for two distinct bubble-like characteristics: faster than exponential price movement and accelerating oscillations (see Podcast: Using a Supercomputer to Trade the Market).

Their July report notes an increasing trend of positive bubbles across multiple asset classes.

Here’s what they say in their “big picture” section:

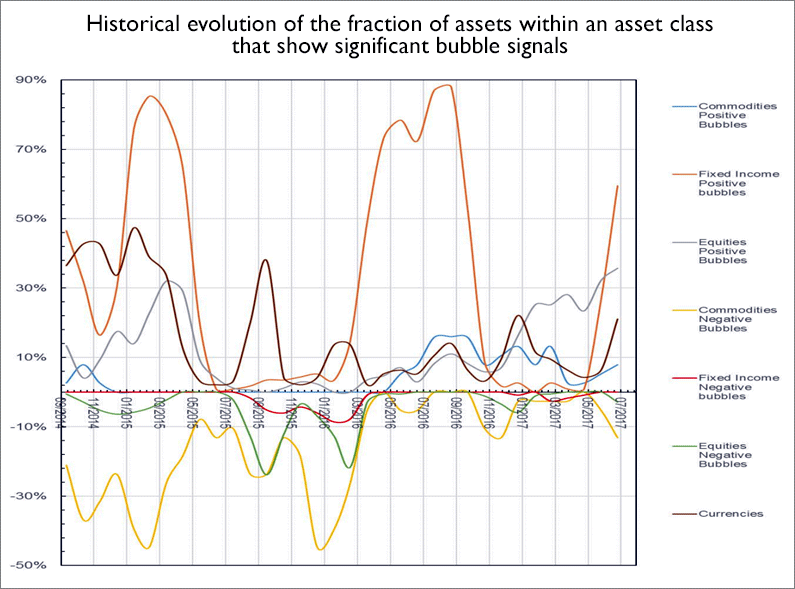

“One can observe the continuation of a trend in the growth of positive bubbles in the fixed income asset class for the second month. The fraction of stocks diagnosed in a positive bubble state increased this month to exceed 36% compared with 32% last month. Mixed bubble signals still occur only in few commodity indices. We also observe renewed bubble activity in currency pairs.” [source]

Here is the chart where they show the “historical evolution of the fraction of assets within an asset class that show significant bubble signals”:

Based on their daily scan of global markets, the Financial Crisis Observatory assigns individual stocks into four different quadrants based on their bubble strength and value score. These four quadrants are then used to create a trading strategy consisting of four different portfolios, which they define as follows (click image to enlarge):

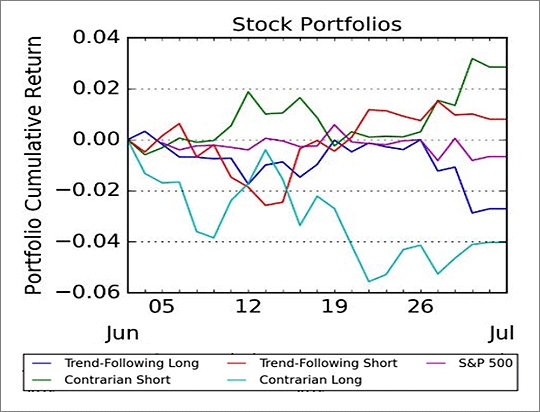

In looking at each of the four portfolios, it appears that the supercomputer was mostly initiating long positions since March. However, starting in June, the researchers note that there has been a rebound in Contrarian Short portfolios in recent weeks:

“This month, we find that Long portfolios started to develop a drawdown in most portfolios initiated in March, April, May and June 2017. This reflects the stopping of the previously booming markets. Especially, the Contrarian Short portfolios rebounded in recent weeks. Contrarian Portfolios are more delicate to use due to their sensitivity to timing the expected reversal and exhibit very volatile performances, indicating that most of bubbles in the market are still dominating and that fundamentals have not yet played out. We expect trend-following positions to perform in the months following the position set-up and then contrarian positions to over-perform over longer time scales as the predicted corrections play out.”

Here is a chart illustrating each of their four portfolios since June with the rebound in Contrarian Shorts shown in green, which they expect to “over-perform over longer time scales as the predicted corrections play out.”

Based on the large and growing list of positions in its Contrarian Short portfolio—which includes the FANG stocks—it would appear that FCO's supercomputer is setting up for some sort of market crash or correction in the months ahead.

To listen to our May interview with Didier Sornette, please log in and click here. To access this month’s Global Bubble Status report with its full list of positions, click here.