Note from dshort: With this morning's release of the Consumer Price Index for September, we can now calculate Real Retail Sales for last month.

Official recession calls are the responsibility of the NBER Business Cycle Dating Committee, which is understandably vague about the specific indicators on which they base their decisions. This committee statement is about as close as they get to identifying their method.

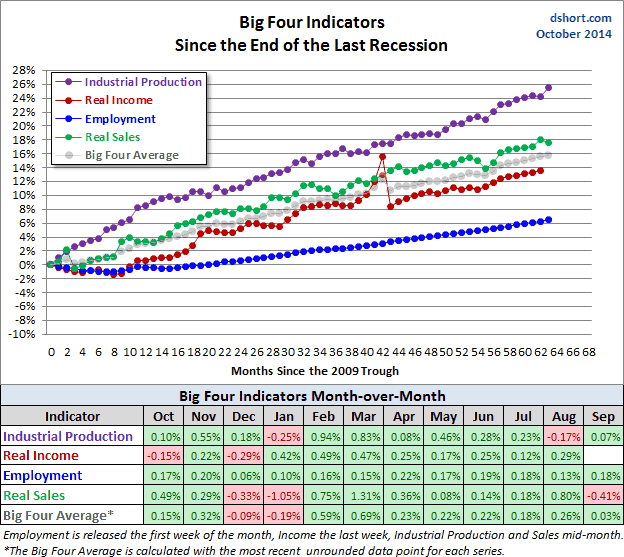

There is, however, a general belief that there are four big indicators that the committee weighs heavily in their cycle identification process. They are:

- Industrial Production

- Real Personal Income (excluding Transfer Payments)

- Nonfarm Employment

- Real Retail Sales

The Latest Indicator Data

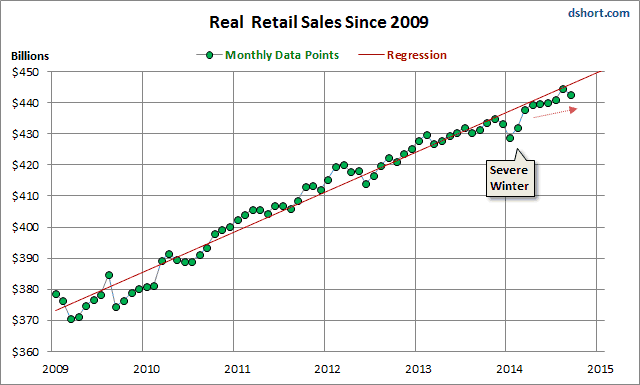

With this morning’s release of the September Consumer Price Index, we can now calculate Real Retail Sales. I reported the nominal Advance Retail Sales last week, which showed September at -0.3% (-0.32% at two decimals) month-over-month, down from 0.6% in August. That was much worse that the mainstream forecasts. When we adjust for inflation, September sales came in even worse at a -0.41%. The chart below illustrates the series since 2009 with a linear regression to help us analyze the trend.

The contraction in sales attributed to an unusually severe winter is clearly evident. April through July performed below trend. August saw a positive bounce that put us back to trend, but September appears to have reverted to the substandard summer growth.

The Census Bureau's Retail Sales series is, as I've pointed out elsewhere, subject to substantial revisions, to the latest month shouldn't be taken too seriously.

The Generic Big Four

The chart and table below illustrate the performance of the generic Big Four with an overlay of a simple average of the four since the end of the Great Recession. The data points show the cumulative percent change from a zero starting point for June 2009. We now have the three indicator updates for the 61th month following the recession. The Big Four Average is (gray line below).

Current Assessment and Outlook

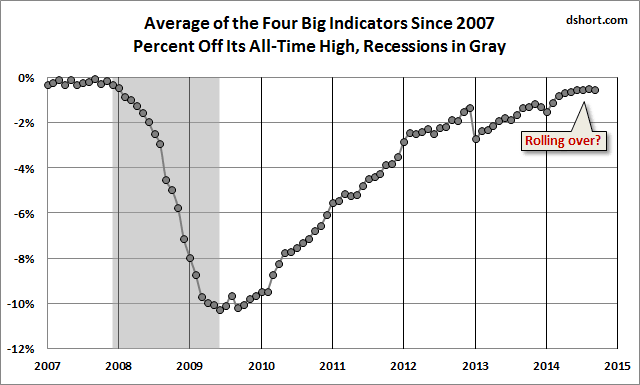

The overall picture of the US economy had been one of slow recovery from the Great Recession with a clearly documented contraction during the winter, as reflected in Q1 GDP. Data for Q2 supported the consensus view that severe winter weather was responsible for the Q1 contraction — that it was not the beginnings of a business cycle decline. However, the average of these indicators in recent months suggests that, despite the Q2 rebound in GDP, the economy remains near stall speed. We'll need some near-term improvement to avoid rolling over.

The next update of the Big Four be the month-end Real Personal Income less Transfer Payments.