With the unemployment rate in the high single-digits and with national average gasoline prices approaching last years' highs of $4/gallon, one would think that the consumer discretionary sector, which lives and breathes by the spending habits of the US consumer, would be struggling. However, nothing could be further from the truth.

The consumer discretionary sector is currently displaying the strongest breadth out of any sector in the market with the S&P 500 Retailing Index continuing to make new 52-week and all-time highs.

Given more than 70% of US GDP comes from consumption, the positive action in the consumer discretionary sector can be taken as not only a positive sign for US GDP but also for the stock market. Until we see broad-based deterioration in the sector both the economy and the stock market should be given the bullish benefit of doubt as both look to head higher in the months ahead despite a likely pause in the near term.

S&P 500 Retail Index Hits New All-Time High

Because the US economy is based on services and consumption, tracking retail stocks in particular and the consumer discretionary sector in general provides valuable clues to the stock market and economy. The retailing industry often leads the stock market at key turning points and given the stock market leads the economy, the retail industry provides and early warning for both and is a valuable leading indicator. This is shown in the graphic below with the most recent recession shaded in red. The fact that the index is hitting an all-time high gives support to the bulls that the US economy and stock market are likely to head higher in the months ahead.

Source: Bloomberg

Breadth Shows Consumer Strength Is Broad Based

Often at major market tops investors begin to seek safety by pouring into the largest and most liquid stocks, which can mask internal erosion of market strength since many indexes like the S&P 500 are market cap weighted. Typically, this acts to drive the prices of large cap stocks higher and smaller cap stocks lower into their own private bear markets. Thus, monitoring breadth is vital to judge the health of any rally to look for cracks in the bullish thesis. When looking at the percentage of sector members within the S&P 500 hitting new 52-week highs over the last month, it is quite bullish to see the consumer discretionary sector as the strongest sector with 43% of its members hitting new highs, well above the second strongest sector, which is technology with 31% of its members hitting new highs.

Source: Bloomberg

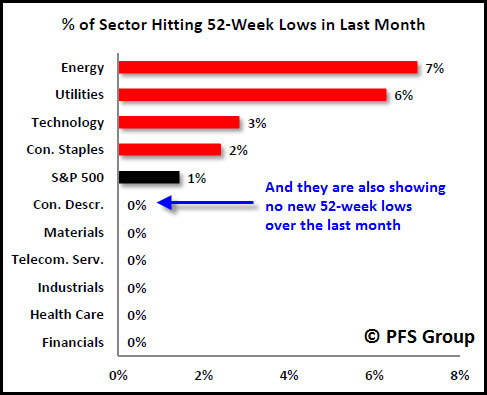

Additionally, not only is nearly half of the sector hitting new 52-week highs, no single member hit a 52-week low over the last month as the strength in the sector, and the entirety of the S&P 500, has been incredibly strong.

Source: Bloomberg

Zeroing in on the retail sector, equally weighted indexes are valuable in that the largest market cap stocks do not mask the smaller members' influence on the index. The S&P Retail Select Industry Index, which the SPDR S&P Retail ETF (XRT) is based off of, is an equally weighted index with all 94 members having the same influence. Over the last month, 43 of the index’s 94 members hit a new 52-week high while 2 hit a new 52-week low, which shows more than 21 new highs for every new low.

Not only has breadth been stellar for the retail industry but so has performance. For the 43 members within the index hitting new 52-week highs the gains year-to-date have been spectacular with returns ranging from Priceline.com, at the high-end, of 52.85% to HSN Inc, on the low end, of 4.41%, with the average being 23.62%.

Source: Bloomberg

Consumer Sector and Leading Economic Indicators Singing the Same Tune

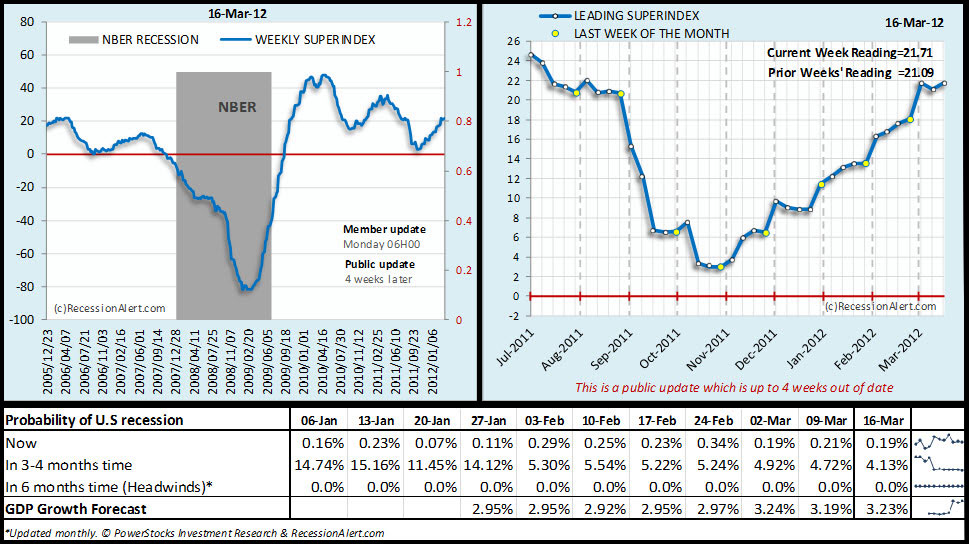

With such broad-based strength in the consumer discretionary sector and retail in particular, there does not appear to be any alarm for a coming bear market or recession given that consumption makes up more than 70% of GDP. Corroborating the message of the consumer discretionary sector is the research from RecessionAlert.com as their Weekly SuperIndex continues to climb and suggests only a 4.13% probability of a U.S. recession occurring in the next 3-4 months. Also noted in the table below, their Headwinds model suggests a 0% probability of a recession in the U.S. in the next six months.

Source: https://recessionalert.com/

Summary

The consumer discretionary sector has historically provided early warning signals for stock market peaks and troughs and shows an even greater lead time to economic turning points. For this reason the sector’s broad-based strength with nearly half of the sector hitting new 52-week highs over the last month is quite bullish for the market and economy’s outlook ahead. Corroborating the message from the consumer sector is the data from RecessionAlert.com, which shows less than a 5% probability of the U.S. slipping into a recession in the next 3-4 months according to their Weekly SuperIndex. It appears that the US stock market and economy are on solid footing for at least the first half of 2012, although we are likely to see some turbulence as we approach the November elections. Markets hate uncertainty and we will be getting closer to the monster tax increases that are set to occur in 2013. While the market’s technical backdrop is very healthy, do not be surprised to see a period of consolidation as the market digests the gains off the October 2011 lows.