(I’m looking at the macro fundamentals and I think an inflection is coming up in a few months…and that means opportunity.)

At the highest level, global growth is coming from a few places:

- China stimulus: backstopping materials prices and also juicing up Asia/E.U. activity.

- E.U. stimulus: propping up activity via negative rates and public spending to integrate migrants (now running ~$80 billion annually).

- Favorable Comps: The first half 2016 (H1) was terrible, so H1 2017 has been fantastic

The stimulus is losing effectiveness: nominal levels of goods consumption remains stuck at 2015 levels. And capacity just keeps growing.

You may also like Goldman's Tousley on Global Economic Expansion, International Small Caps

Meanwhile, the current growth waves are set to slow in the next 4 months.

China Is Already Slowing

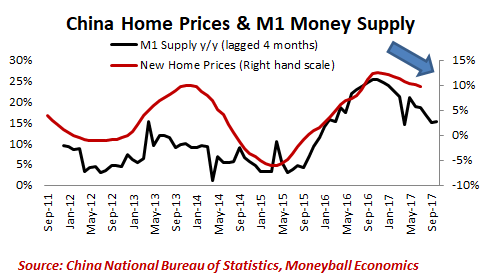

Money supply is critical to keeping China’s domestic economy afloat. It’s underpinning domestic demand:

Simply looking at M1 supply above, you can see the slowdown coming to China.

Everything is already slumping (OK – most countries would still kill for 6%+ Industrial production growth. But this is a slump compared to the 10%+ they had just a couple years ago).

And if China wants a “soft landing” (being able to transition their economy to consumer-oriented like the U.S.), then the current slow growth trajectory will continue.

E.U. Is Starting to Catch China’s Cold

China’s slower growth is bad news for EU, which relies on China’s private sector demand.

E.U. consumer goods are very popular in China. As is machinery and materials.

For a sign of what’s to come, Germany’s most recent Factory Orders Exports didn’t grow at all (came in at 0% growth). Accelerating this trend will be the new German auto factories coming online in China.

Masking this decline is E.U. migrant integration stimulus.

Domestic consumption is surging, which it should be given the ~ billion (B) earmarked in 2017 public spending. Germany alone has budgeted B.

That’s a lot of housing, food, and healthcare spending. ut the pace of those capital injections begins to taper off in 2018.

Already, the signs of a peak are evident.

The Moneyball E.U. Shipping Index shows that peak growth already came. (As a reminder, this data measures a specific set of cargo shipments of high-value, intermediate goods).

To put this into context, the volume of cargo passing in and out of the Port of Hamburg is stuck at 2012 levels. The growth we see in the E.U. is better than 2015 but still weak.

The current trajectory in trade suggests continued growth through the rest of this year.

But expect problems to emerge in Q1 2018 because growth waves are tapering at the same time (China demand, migrant stimulus, and favorable comps). And this is before any possible tightening from the European Central Bank.

The US Is Also Set to Slow Down in the Coming Months

How mediocre is US growth?

Check out Ned Davis: "We Are in the Very Late Innings"

It’s been barely cranking out 2% GDP despite 0% interest rates for 9 years. And even today where we have <2% inflation. And this year – H1 2017 -enjoyed some now-fading drivers

- Favorable comps: Q4’15 and Q1’16 GDP were ~0.5%, so any year-over-year (yr/yr) comparison looks fabulous. But H2 2016 was a lot stronger.

- Catch-up spending: a lot of H1′17 has been replenishing stockpiles and re-engaging necessary spending. (A substantial amount of ordinary CAPEX spend was tabled 2015-2016 and now fundamental maintenance requires some spending.)

But like the E.U., the growth has come from refilling the bucket and not really advancing the economy.

Capacity Utilization jumped after the election as stocks were “re-filled.” But now it’s fading again.

The end of the “Trump Stimulus” hope will add drag in Q4 and beyond.

Obvious Signs of Stress

The hallmark of peak consumer spending is when sales teams push unnatural acts.

When normal growth becomes unsustainable, the sales team is pushed to look for ways to keep the momentum going.

That’s happening right now in the auto sector where loan quality has eroded (less qualified buyers, longer-term loans, etc). Auto Sales didn’t peak in 2017, they peaked last year. They remained high because sales teams scrambled to sell cars any way they could because organic demand was slow.

It takes a while to see, but the current slow auto sales environment is coming despite the unnatural sales acts. That is, after trying every trick in the book – sales are still slowing.

Read Is the US Economy Doing Just Fine?

Now comes the blowback: subprime delinquencies have surged, 84-month loans are at 6% of total auto sales – a sign of the desperation out there. It’s pulling in future sales today.

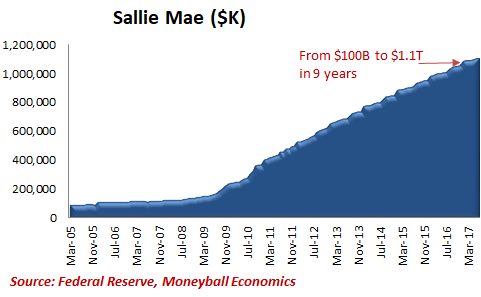

So now take the auto sector and extrapolate from there – what other sectors have boosted today’s sales at the expense of tomorrow’s? And how much has depended on student loans?

Understand that ~80% of student loans are not used for tuition. It went to cars, vacations, home buying and so on.

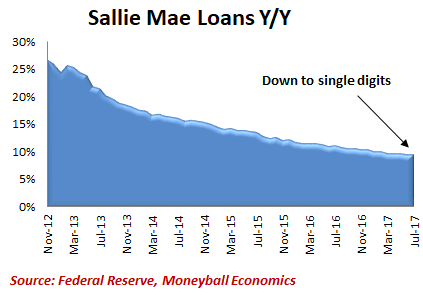

That capital flow is still massive (+$100B yr/yr) but it is also slowing: the yr/yr growth rate has fallen <10%.

Basically, another force driving the US economy is starting to taper.

Going forward: macro data will slip.

As we get deeper into Q4, the comps get less favorable. Then we get more Chinese-driven deflation as their demand continues to slow and that hits material prices again. The E.U. will also start to flash slower growth. Same with US.

The Supply Chain Is Preparing for Slower Growth in 2018

An interesting bit of color is coming from the semiconductor space which has been on a phenomenal roll.

Like the rest of the industrial space, semiconductor companies hit the brakes on expansion in 2015. As demand caught up and supply was restrained, customers faced limited supplies and have been paying higher component prices.

But semiconductor producers are also aware that the cycle turns down and they expect it to slow again in 2018. In fact, they are planning for it.

KEY TAKEAWAY: All of this slower growth narrative runs counter to consensus expectations. 2018 E.U. GDP is expected to be faster than this year’s.

So what should we expect? With Central Banks talking a tightening trajectory, fundamentals are going to come back in fashion.

- Timing: Q1 seems to be the inflection point when macro starts to look consistently worse.

- Degree: Lots of debt exposure in the private sector. It’s more manageable than in 2007, but it’s also nominally higher and just as central to the economy. Fire sales may not be as widespread or deep, but it will be ugly nevertheless

- What to watch:

- US: inflation (trucking prices), wage growth (esp. Jobless claims y/y), corporate profits

- EU: trade esp. Sweden (the canary in the German coalmine)

- China: M1 supply, trade

Under these conditions, Stronger US dollar is likely for the usual reasons (currency manipulation, flight to safety, etc).