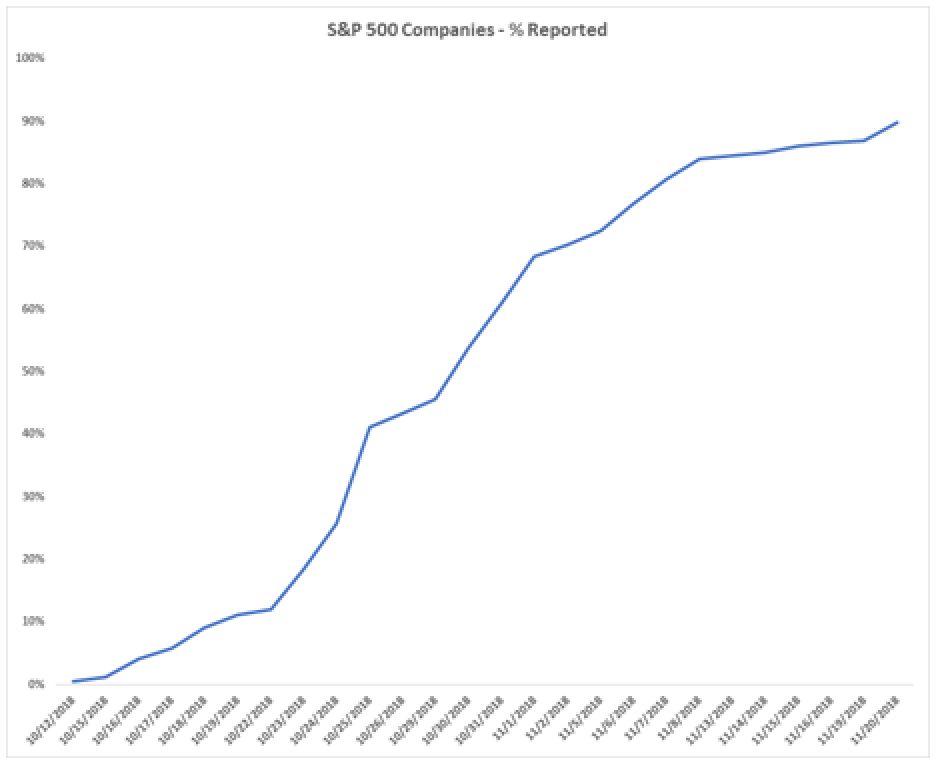

October was nothing short of a whirlwind for the markets as nearly two-thirds of the entire U.S. stock market just went through a bear market. Contributing to the year’s market rollercoaster were third quarter earnings; a majority of companies within the S&P 500 reported in October as you can see illustrated below:

As of Nov. 12, 84 percent of S&P 500 companies have reported earnings. Companies with positive results saw flat to little price appreciation, but companies reporting negative results have been severely penalized. As earnings season ends, I would like to highlight some of the factors that have made the most impact in the markets this season.

Of the companies reporting , less than three-quarters beat their estimates. Take a look at the infamous FANG stocks that held the S&P 500 performance up throughout the year.

Facebook, Amazon and Google beat earnings this quarter but missed on revenues causing their share prices to plunge. Netflix, on the other hand, surged after beating earnings and meeting expectations for revenue projections (I subscribed recently so they can thank me for this).

Price reaction for stocks this season were based on revenue stories demonstrated in the FANG stocks. One can see a similar pattern when looking at effects on the average price reaction for returns on a beat/miss on earnings vs. revenues from this quarters’ earnings season:

One of the October sell-off causes can be traced to unexpected margin weakness—the same issue that led to the 2011 correction in the U.S. stock market. Rising transportation and input costs are starting to take a toll on profit margins for companies within the index.

We could see larger problems for profit margins should tariffs from the U.S.-China trade war be imposed. However, if trade negotiations are better than expected, it would benefit U.S. companies whose revenues are intertwined with China.

Last week markets started to gain some headway after a historically bad October with the S&P falling 6.9 percent— the greatest drop since September 2011. The S&P is surpassing expectations for EPS growth this quarter, rising above a predicted 21 percent. It’s now on track to hit a 26.3 percent year-over-year EPS expansion, beating the second quarter peak of 26 percent.

It’s widely believed there will be a global growth slowdown in 2019, projected in earnings expectations at a 10 percent year-over-year growth. With peaking earnings growth and changing economic conditions, it looks like next year will be another wild ride, stay tuned.