Last week, the Fed made an unprecedented dovish turn. Nick Reece of Merk Investments joined FS insider to discuss this along with record-loose U.S. financial conditions and the importance of U.S. oil production in terms of inflation and future Fed tightening.

“Financial conditions in the U.S. are at the loosest levels of the cycle according to the Chicago Fed’s National Financial Conditions Index,” Reece said. “Now that the Fed has communicated their plans on balance sheet normalization and have said they’re going to stop quantitative tightening in September... they’re really only left with the tool of interest rates.”

Reece added that he believes we’re in a cycle that’s still going, especially since “financial conditions continue to be extremely loose and extremely favorable,” citing the Chicago Fed National Conditions Index below as one such indicator that shows financial stress levels are quite low. He said his best-case scenario would be that the Fed continues with “another hike or two” in this cycle.

According to their dot plot, the Fed is planning to raise rates one more time in 2020 but stay put for the remainder of the 2019. The Fed will release an updated dot plot in June and Reece believes “we could get a dot plot…that is all of a sudden looking like we’re going to have to do a few more hikes, maybe one or two more.” He said the reason for this could be due to the appreciation we've seen in oil prices since late last year, which will start pushing up inflation. “So, if this trend continues in oil,” Reece said, “the year-over-year comparison is actually going to be adding to headline inflation in the second half of the year.”

Subscribe to our Podcast! Click here for a FREE trial

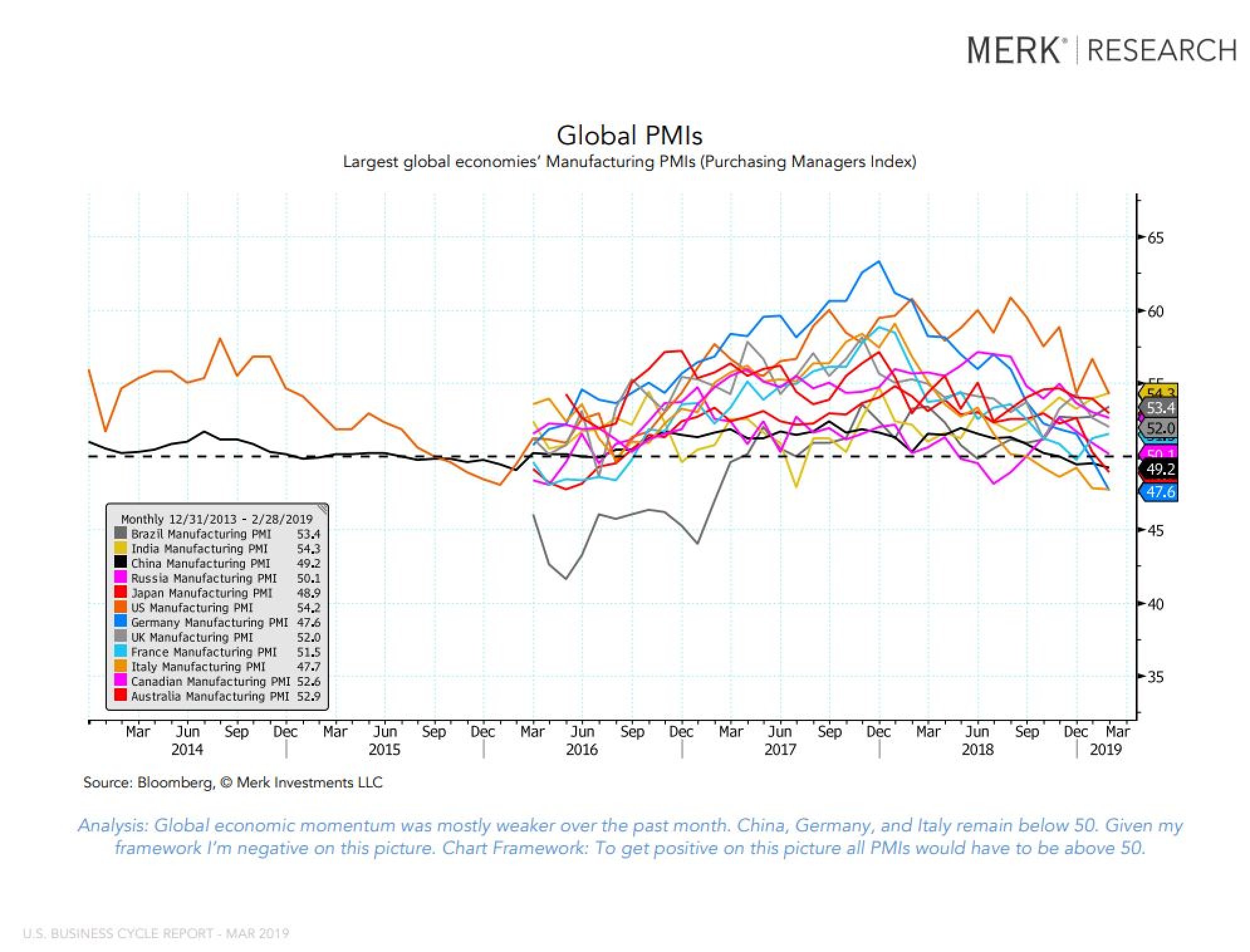

“There is a strong relationship between oil prices and inflation expectations, which is relevant to Fed policy,” Reece explained. He sees three main factors that led to the decline in oil prices in 2018. The first is the global slowdown, which is quite apparent when you look at the global PMI downtrend last year and continuing into this year, as can be seen in Reece’s chart below.

The second factor Reece identified is speculative positioning. “Futures speculators were extremely levered long in the oil market following the trend and a lot of that had to unwind, which added to the downward pressure to oil prices in the fourth quarter.”

Supply increases are the third factor Reece named. Oil supply increases have in large part come from the U.S. making the oil sector that much more of an important piece in the U.S. economy. This relationship between oil supply and the U.S. economy could be a contributing factor, Reece said, “as to why oil prices have been such a good real-time indicator for manufacturing PMI in America.” Consider the history of U.S. oil production from 1920 to 2019. After hitting a low in the late 2000s at around 4 million barrels per day, it has since skyrocketed to a record 12 million barrels per day!

The U.S. has now overtaken Saudi Arabia and Russia as the largest producer oil, completely reversing the 30-40 year downtrend in place since the 70s. This is extremely significant and perhaps one of the most overlooked factors when it comes to the outlook for inflation, Fed monetary policy, and the business cycle.

What's more important is that this massive spike in oil production has taken place only during this economic cycle, from 2009 to today. We've never seen anything like this during any other cycle in U.S. history.

Log in to listen to Reece's full interview with FS Insider. Not a subscriber? Click here for a free trial.

For more information about Financial Sense® Wealth Management and our current investment strategies, click here.