Observe how two years later, the Fed’s expected ‘transitory’ factors are still here:

“Recent sizable declines in oil prices will likely hold down overall inflation in the near term. But as the effects of these oil price declines and other transitory factors dissipate and as resource utilization continues to rise, the Committee expects inflation to move gradually back toward its objective.” –Federal Reserve Chairman Janet Yellen, December 2014

“…once oil and import prices stop falling, the downward pressure on domestic inflation from those sources should wane, and as the labor market strengthens further, inflation is expected to rise gradually to 2 percent over the medium term.” -Yellen, February 2016

The Fed’s next move with interest rates is the biggest issue driving global credit and equity markets. The fundamental idea is that the economy is like a candle: if it burns too bright, it burns out faster; if it burns too low, it could snuff out. Moderating the flow of oxygen is a means of managing the candle’s flame.

Read California and Semiconductor Companies Point to Continued Slowdown, Says Leading Economic Forecaster

Interest rates are the oxygen for the economy: low rates turn up the economy, and high rates bring it down.

Inflation is regarded as the outcome of economic activity and the demand for limited resources (Yellen’s “resource utilization”). The Fed is on inflation watch and expects it to arrive. Yellen is making two key points:

- First, that the economy is strong and pushing up inflation (the “resource utilization”).

- Second, that oil prices have fallen and are masking the underlying inflation.

Is she correct? Yes and no. Yes, that inflation is coming, and no about the cause. And that’s the worrisome part.

The Fed Is Partially Right

Oil and food price deflation is holding down inflation, and the effect is transitory. See the chart below.

The Fed’s timing is off a bit. It keeps expecting oil deflation to run its course. Well, it’s been two years, and it is still around for a while yet. Oil deflation is still working its way through the economy, courtesy of trucking. In the US, nearly 70% of all goods are shipped via truck, and shipping prices continue to fall because gas price surcharges are sticky downwards and lagging. This means the effects will be around for most of this year. But overall, the big impact has already been felt.

Consider Russell Napier Forecasts Negative Rates in the US as Deflationary Pressures Spread

The Fed Is Mostly Wrong

It’s important to note the following:

- Economic demand is not about to drive up consumption-related inflation.

- Inflation comes from areas largely immune to interest rate changes.

- Inflation will remain mild.

Problem #1: Resource Utilization is Falling

Resource utilization is falling and is set to keep falling. Per Yellen, the Fed expects resource utilization to rise. In fact, as measured by manufacturing capacity utilization, resource consumption continues to drop. It’s been down for 15 months.

Now go back to the trucking data. Prices dropped partly from oil price pass-through and partly due to a decline in demand. The load-to-truck ratio is at its lowest in four years (the ratio measures volume needing to be shipped relative to available trucks).

Contrary to Fed expectations, resource utilization is not even close to rising.

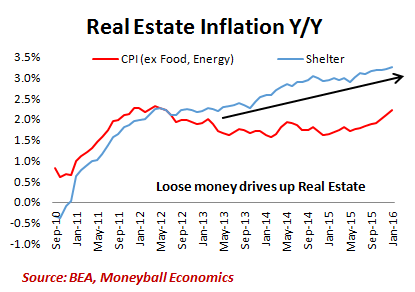

Problem #2: Inflation from Fed’s Real Estate-Propping Policies

The biggest source of inflation has been sheltered, aka real estate. Real estate inflation has been surging for years thanks to the Fed’s specific policies aimed at boosting real estate property prices.

It’s likely that recent tightening will slow this inflation.

The Fed created this part of the problem and is now – belatedly – addressing it. But it also means that this source of inflation is poised to slow.

Problem #3: Obamacare Triggered Inflation

When I had my first baby, the doctor conducted individual pre-natal tests. A few years later, and with my second baby on the way, the wonderful world of medicine had concocted a few more tests, all covered by insurance, naturally.

The reality in medical care is that, up and down the food chain, there is an incentive to spend more money. From the doctor’s perspective, more tests mean more money. There would be a cost avoidance element because of the very real threat of malpractice lawsuits if a ‘standard’ test was not performed.

Thanks to insurance coverage, firms are clearly motivated to develop new treatments. Obamacare turbo-charged this behavior because it effectively wrote a blank check and created a new customer base. Nearly everyone and everything are covered. Cost containment has never been a part of Obamacare, which has meant inflation in healthcare.

That’s exactly what we see: medical care inflation was dropping until Obamacare started. Guys like Martin Shkreli can – and do – jack up prices easily in a system with maximal coverage and minimal cost containment.

This inflation is not sensitive to interest rates, and that’s potentially where the Fed may miscalculate by misreading the inflationary signals and wanting to clamp down hard on an area that doesn’t respond to interest rate hikes.

Problem #4: Slight Labor Inflation from Minimum Wage Hikes

The media claims that labor demand is strong, and it’s driving up wage pressure. Unemployment rates have fallen to an unprecedented 4.9%. The truth is much different.

Even the Fed has said that the unemployment rate is not believable. As last week’s payroll data showed, overtime is dropping, and so are earnings and the hours worked each week. In other words, like factory utilization, labor demand is loosening.

The only reason for wage pressure is that beginning in 2014, many cities and states began to hike minimum wages. Before that mandated hiking, many companies started to raise hourly wages anyway. Laborers have no price power here: 7+ years of a recovery and unemployment in the leisure and hospitality sector is stuck at 7.7%.

The perverse irony being that we have a fiscal policy in the form of minimum wage hikes trying to counter the inflation created by monetary policy in the form of rising rental costs thanks to surging real estate prices.

The key point here is that wage pressure is emerging but for non-economic reasons.

Add It All Up

Here’s an overview of the components and suggestions for the next year:

While we lose the deflationary impact of energy and food, it’s difficult to see a corresponding uptick in the other factors. Shelter and healthcare inflation will stay the same, which leaves wages – and that seems to be abating.

Ultimately the Fed is pulling a hustle. Inflation remains mild, and there is no indication that it will rise.

In a normal environment, the discussion would be about loosening rates, not tightening them. Against the backdrop of a US manufacturing recession and a slowing service economy, as well as a strong dollar and falling global macroeconomy, rate hikes seem like bad logic.

Read also Ultra-Low Rates Could Last Another Decade

It would appear that the Fed is heading to policy error, which will make the markets panic.

The sad reality is that the Fed wants to raise rates to escape the zero interest rate regime (ZIRP). The state of the economy is irrelevant.