Over the course of the current cycle I’ve pointed to one glaring dichotomy based on historical precedent again and again – the lack of a small business fundamental recovery. While the large multi-national blue chips have basked in the sun of global central bank sponsored stimulus, small businesses have struggled under increased regulation and a domestic economic recovery that has been one of the most shallow on record. Without beating a dead horse, history tells us small businesses have been crucial in sustaining employment recoveries. Additionally, capital spending on the part of small business has been meaningfully additive to overall economic recovery character in prior cycles. The rhythm of small business conditions being “in synch” with their larger corporate brethren has been broken up to this point in the current cycle as a definitive “fingerprint” character point.

But is this about to change? Last week our friends at the NFIB delivered December’s small business optimism survey. It deserves a bit of attention. To the point, one of two things is occurring. Either small business is getting stronger and conditions are improving at long last. Or, as I’ve written about recently, along the lines of Francois Trahan’s current thinking, in a zero bound rate environment, the short term change in input prices acts as the Fed Funds rate would act in a more normal cycle. A decline in input pricing pressure for business essentially acts as stimulus, and vice versa, with a definable lag period. Is this what’s making small business feel a bit better? If so, just how long will this positive lag effect be a benefit? In other words, is this just another blip up in small business confidence like we saw in 2010, only to be followed by renewed weakness?

Below is a quick look at where macro small business optimism stands as we move into the New Year. The recent multi-month improvement in overall optimism is definitely a plus. But of course in absolute terms small business optimism has not yet topped its 2010 highs and at in current absolute terms remains near the recession lows of the early 1990 and 2001.

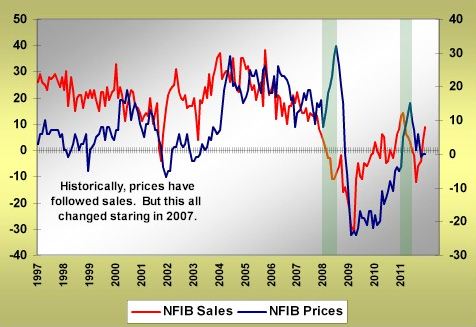

In addition to headline optimism increasing, very notable has been the recent multi-month rise in small business sales expectations. In the chart below we’re looking at the small business outlook for both sales and prices. Historically, these two data series have been highly directionally correlated with pricing following sales, but that’s clearly not the case at present and has not been since the whole cycle of deleveraging kicked off in earnest in 2008/2009. You can see that in early 2008 when pricing expectations were rising significantly, sales expectations were falling. Prices determined activity, activity did not determine price.

I think this set of small business survey component circumstances in a sense corroborates the thinking of input costs being a short-term driver of macro economic and now small business reality. If prices fall, small businesses expect sales to increase. If prices rise, as they did in 2008, small business expected sales to fall (and they were correct). This concept applies to macro economic stats as well as small business numbers specifically.

Hopefully as a last point corroborating just how important commodity prices have become in the zero bound environment to the perceptual outlook of small business folks is what you see below. Without question small business price outlook is incredibly highly correlated with the CRB itself. And of course this lends itself to the question, just what happens if the CRB has bottomed? We’ll have our answer about 6 months after this ultimately occurs.

So don’t get me wrong, it’s absolutely wonderful to see small businesses feeling better about life. The key question becomes, is this temporary, or the beginning of a true cyclical recovery? As you already know, this is also the key macro economic question for the US. Are the improving economic stats as of late pointing to a much needed sustainable growth spurt, or are we temporarily reaping the benefit of commodity prices that have fallen since last April, but are now stabilizing?

I’ll leave you with one last thought. Whether large or small, the real measure of business optimism, if you ask me, is capital spending. Despite renewed strength in a number of macro economic stats these days, capital spending at the macro level has weakened. In terms of small business, without question pent up demand should be very strong for capex. This is where the rubber will hit the road. If indeed the small business sector is now on the cusp of true cyclical recovery, we’ll see small business capital spending pick up meaningfully. Of course the reverse is also true. In the past, the small business capital spending outlook has followed sales expectations directionally. Prices are down, small businesses now expect sales to be up. So now we watch small business capital spending. So what was the December small biz capital spending outlook? Flat relative to the prior month, despite the jump in sales expectations. Whether this is a false start or the beginning of a true cyclical upturn, it’s too early to pass judgment. Is the rear guard (small business) finally about to get into the game? Stay tuned.