These comments will mean little to market outcomes in the next few days or months, perhaps even years for all I know. I’d like to address a big-picture macro that I think will be important somewhere down the road and will act perhaps as a behavioral bookend to the beginning of the bond bull market in the early 1980’s. But indeed if I’m anywhere even near the mark on this one, bonds will only be one part of a much larger story.

Let me set the stage. Although many of you may be far too young to remember, Arthur Burns was the Fed Chairman when true inflation really started to heat up materially in the 1970’s. Although Paul Volcker was and should be credited with having the intestinal fortitude as a central banker to break the back of inflationary psychology as well as price acceleration reality, his predecessor Arthur Burns did not sit back and allow inflationary pressures to brew unattended. Unfortunately for and unbeknownst to Mr. Burns at the time, the markets were not in the mood for incremental action. Another unfortunate issue is that since Mr. Volcker, we have seen little central banker intestinal fortitude leading us to our present circumstances, but that’s beside the point. As Burns incrementally raised the Funds rate in the mid to latter 1970’s, the markets took long rates on an ever higher upward joyride far ahead of incremental Fed action, scaring the living daylights out of bondholders from sea to shining sea. In like manner, gold ultimately took off like a bottle rocket. Just what were gold and the bond market conveying at that time in terms of the message of price action? During the latter reign of Mr. Burns and initial reign of Mr. Volcker, the markets were unequivocally clear in message as bond yields, gold and other inflation hedges zoomed upward – the market had lost confidence in the Fed.

Of course history is also clear that though what many may have deemed shocking central banker action at the time, Mr. Volcker ultimately restored that confidence in the Fed as a potent monetary decision making institution. Believe me, I could rant and rave on and on about what has transpired under Greenspan and Bernanke, but that’s water under the bridge and will not help us in forward decision making. Although this is far from a guarantee, I have been asking myself lately if the bond bull and risk-on versus risk-off mentality of today will also at some point come to an end in bookend fashion in the current cycle with the very same character point - an ultimate loss of market confidence in the Fed and really central bankers globally. I think it’s worth at least an assignment of some probability to this type of outcome. Moreover, that means I need to start looking for confidence crack fingerprints. If they are to come, they will first be hairline, barely noticeable and not meaningful to short term outcomes, but will grow wider as confidence is increasingly lost.

I promise, this is not about perma pessimism or darkness. This discussion is about the anticipation of a potential financial market perceptual construct that may develop before the current cycle has concluded. Let’s call it “the cycle of historic central banker intervention” for lack of a better or conventional term. Who knows, this loss of confidence may never appear, but my stomach acid is compelling me to think about this now, especially as investors of the moment are so intently focused on and make important decisions around current Fed choice of short term vocabulary. Moreover, central bankers globally are in the midst of a historically unprecedented experiment of balance sheet expansion. There is no roadmap. There are no models. They have zero experience not only in initiating, but also ultimately reconciling the current magnitude of policy expansion actions. And this will all transpire with nary a concern on the part of global capital over the complete cycle? That sure seems one tall order.

So just where may we be seeing these initial hairline confidence cracks?

Equity Fund Flows

Although I’ll spare you the charts as you can easily find them, a key character point of the current cycle is that equity mutual funds have been under virtually consistent liquidation. Usually associated with “public flows”, the current cycle is very much the anomaly relative to historical experience. Even given the equity market run we’ve seen since last October, last week’s equity fund flow numbers showed us the largest one week outflow for 2012. YTD, equity fund outflows are now twice what were seen last year. And this is IRA/401(k), etc. funding season!

Yes, flows into ETFs have been strong, but into fixed income oriented ETFs. I’ll save this for another discussion entirely, but in looking at the flow data really since 2009, the public has loaded up on bond funds/ETFs. Is this a sign that the public has lost faith and simply is not coming back to equities in any meaningful manner for the current cycle? In one sense have they lost confidence in a Fed that has gone to historically extraordinary lengths to herd investors/capital into higher risk assets? It sure appears that way, at least for now. And of course this points directly back to the ramifications of an ultimate Fed monetary policy unwind. The public is now directly in the crosshairs of unwind fallout having committed the largest nominal dollar flow into bond funds ever seen.

Consumer Confidence As Expressed In Credit Acceleration

Although headline consumer confidence surveys have brightened a bit as of late, what consumers do and what they say are two different things. True expressions of “economic” confidence can be seen in corporate capital spending and at the consumer level in the acceleration of consumer credit. The report card so far in the current cycle is clear. Stripped of the very meaningful perceptual influence of student loans, nominal dollar US consumer credit outstanding now stands at a level that was seen in August – of 2004! Consumer credit ex-student loans has declined in both January and February of this year after hitting a current cycle peak in December. Odd given the apparent rebound in employment as of late, isn’t it? The current cycle stands in stark contrast to the 2001-late 2008 experience. In that cycle not even an extended period of jobless recovery (2001-2003) could stop the consumer credit acceleration freight train from consistently moving forward. In the current cycle the train, if you will, has not even left the station.

Maybe it’s unfair to label this a direct loss of confidence in the Fed per se by the public. But given that the Fed has gone to historical extremes to induce credit acceleration, the current cycle contrast of actual public behavior is more than glaring. If you ask me, this is a picture of confidence lost at the public level.

The Institutional Juggernaut

If indeed the consistency of public equity fund redemptions and lack of consumer credit acceleration in the current economic/financial market cycle is a fingerprint crack of confidence, it has meant little to financial market outcomes in what very much is an institutionally dominated financial market environment.

Do you remember Marty Zweig? A near fixture on Lou Rukeyser’s Wall Street Week for years. It was when Zweig was a professor pre his Wall Street days that he coined the now ubiquitous Street mantra of “Don’t Fight The Fed” (along with “don’t fight the tape”). This was far in advance of what have become the real central banker poster children for this truism that was Greenspan and is now Bernanke. Question: Have we now taken this ingrained mantra to its institutional apex in the current cycle, unlike any cycle prior? Are we now looking at the apex of institutional confidence in the Fed’s ability to influence market outcomes? If the following chart does not suggest as much, I don’t know what does. But what that also suggests to me is that if we are at or near an apex in institutional confidence concerning the Fed, then any confidence “surprises” can only be to the downside.

In my mind the “don’t fight the Fed” behavioral roadmap of life has never been more closely followed than has been the case with equity market action since 2009. The “mapping” of directional market movement with Fed policy actions is clear, no?

But as we look a bit closer, it almost seems the “don’t fight the Fed” supposed confidence correlation seen in equity prices is not necessarily a resounding vote of institutional investor confidence, per se, but rather one of “business” resignation as is told by the tale of volume. Volume expresses true investor conviction and enthusiasm. In my mind it’s the true expression of confidence. That’s not what we see in the chart above. As always, we need to remember that institutional investment management is a business and the needs of the business can and do supercede honest personal conviction at times.

We know the daily character of the equity market has changed meaningfully with the advent of HFT. I will not bore you by recanting studies done of market performance over the last few years. Anyone in the business knows that price changes in the futures markets have dominated ultimate cash market outcomes in determining total return over any monthly, quarterly, or annual period since 2009. Just how many times have we seen the cash market price in futures and premarket activity in the say the first half hour and then trade in a very narrow band (HFT churn) for the remainder of the day? It happens all the time in the current cycle. Does this tell us exactly why volume trends have looked as they have with each iteration of Fed policy action since 2009? It is absolutely more than clear that meaningful volume expansion has only been seen on the downside since 2009.

So, the question I’m asking myself is, can institutional confidence in (don’t fight) the Fed become any greater than is already the case and has played out in this cycle? Have we hit an institutional behavioral confidence peak in the Fed with the monetary modus operandi that is QE? This is exactly what I think we are seeing, but you already know my little perceptual thesis will only be proven or disproven with time. Just as Mr. Greenspan and Bernanke could not identify a bubble peak in advance, neither can we identify a peak in institutional investor confidence in the Fed prior to a peak. But the hairline crack in that institutional confidence could easily be the anomaly for the current cycle that is volume expansion, or lack thereof to be specific.

As you know, I’ve led you on a little philosophical journey. A journey of questions and observations as opposed to concrete answers or forecasts. Looking ahead, I personally expect some additional form of QE. Two folks very tied in are telling us exactly the same thing – Mr. Hatzius at Goldman and Mr. Gross at PIMCO. Who knows, a little equity correction and a few “lower than expected” economic stats could have us there before long. The markets have already been dancing to Fed sponsored QE vocabulary over the course of the current year. A very important issue will be market reaction once another QE iteration actually becomes a reality. Personally, when that day arrives, the “apex of institutional confidence in the Fed” will be a behavioral concept I’ll be revisiting. Imagine equities peaking on the announcement after such vocabulary induced anticipation. Could something like that occur?

Remember, in the late 1970’s investors actually hit a low in confidence concerning the Fed. And that low was expressed in higher interest rates and zooming inflation hedge asset prices. Are we now in the process of bookending that confidence low with an institutional confidence peak in the Fed as per QE in the current cycle? Personally I think this is exactly what is occurring.

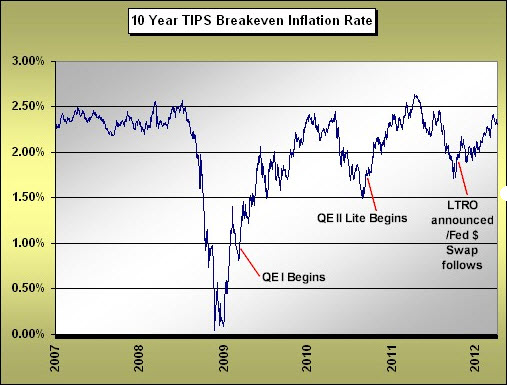

I’ll leave you with one last chart to keep an eye upon and update when the next QE is made official. Each QE has started at a “higher high” in terms of TIPS breakeven rates. If this were a stock price chart, just what would the pattern be suggesting to you?

A potential loss of confidence in the Fed is not a guarantee. But likewise it is not an impossibility as per historical experience. What compels me to at least bring up this issue as a potential outcome is the fact that I see no one talking about it and/or the ramifications of such an event. We need to benchmark behavioral anecdotes as we continue through this cycle and think beyond conventional constructs.