Originally published at Northern Trust

Relax … the title of this segment is not meant to suggest that we think a downturn is imminent. Recessions are rare, and forecasting one is extremely difficult. And if I were to make such a bold prediction, senior management might make it my last.

Nonetheless, economic surveys are reflecting a higher possibility that a recession could begin in the next 12 months. The odds are still modest: 17%, according to the latest Blue Chip survey. But these readings normally hover at 5% or less. Risks to the outlook have certainly risen since the start of the year.

Some are reluctant to use the word recession, given its dire connotations. Years ago, the economist Alfred Kahn was warned by his overseers in the Carter administration to avoid the term, so he substituted “banana” instead. But it is important at times like this to have an open discussion on this topic.

Recessions are often misunderstood, and people have different views on what constitutes a recession, and what causes one. There are rolling recessions, regional recessions, sector recessions and Great Recessions. So let’s shed some light on this murky subject.

Many countries define a recession simply as two consecutive quarters where gross domestic product (GDP) declines. The International Monetary Fund considers the world to be in recession if growth falls to 2%. In the United States, the declaration of turning points in the business cycle is handled by the Business Cycle Dating Committee of the National Bureau of Economic Research (NBER). This group looks at a series of indicators and determines the exact month when conditions turned down. Of course, they don’t figure the timing out until well after the fact, and often well after the recession has ended.

It is often said that economic expansions rarely die of natural causes; instead, something kills them. Typically, some kind of shock, policy error or both conspire to do the deed. In the United States, the subprime mortgage meltdown proved the fatal ingredient in 2008, just like the dot-com crash did the trick in 2001. The policy error of allowing rapid money supply growth in the 1970s founded the deep recession of 1980-82.

Because these kinds of events do not occur with regularity, recessions are hard to anticipate. We’ve had good fortune in the last generation; since 1982, we’ve had only three recessions, two of them very mild. And we’ve had three of the longest expansions in US history.

That run of success, at times, has gone to our heads. There were those who thought we had entered a “new paradigm” where enlightened policy makers combined with self-stabilizing markets to reduce the frequency and depth of recessions. But stability can breed instability. Long expansions can be very comforting, and risks may be underestimated. When times threaten to turn, the reaction can be swift and severe. That may be part of what is going on at the moment.

Psychology plays a pronounced role in the founding and progression of economic recessions. Worried consumers don’t spend as much, worried firms control expenses and worried investors take less risk. These actions can become self-fulfilling, and self-reinforcing.

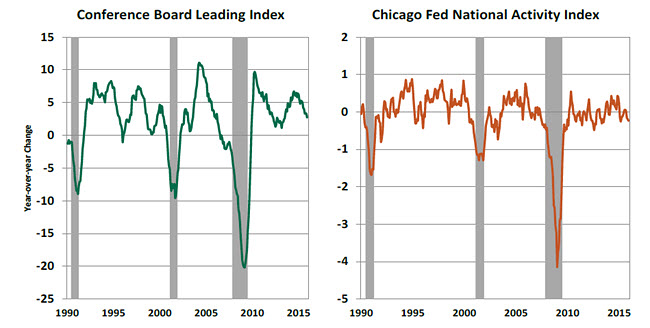

Quite a few indicators purport to presage recession. The Conference Board assembles an index of leading economic indicators, which is still on a solid upward trajectory. The Federal Reserve Bank of Chicago puts out a comprehensive national activity index, which combines 85 indicators. Readings below zero indicate some contraction in activity. Neither one of these is sending strong signals that a downturn is on the way.

Others rely on market-based measures. The shape of the yield curve for Treasury securities is often cited; flat or inverted curves reflect an expectation of falling interest rates, which would result from soft economic conditions. Rising risk premia for assets such as corporate bonds can signal concerns that credit defaults are on the horizon. And since major stock indices include shares from across the economic spectrum, their performance is thought by some to be a bellwether for the business cycle.

The difficulty with all of these approaches is that they send off a lot of false positives. The equity markets are especially poor predictors; there have been three recessions since 1982, but 26 phases where the major US stock indices have fallen by 10%. While big price swings certainly garner headlines, they don’t always signal fundamental problems.

That said, there are a number of potential threats to the business cycle. The realignment of oil prices has produced a lot of pain globally, but little gain. China could be losing its grip on its economy. A host of emerging markets are facing difficult times, and global interconnections can bring all of this very close to home. And the psychology of the situation is not being helped by the current US political campaign, which has brought out a lot of negativity.

Some have suggested that the Federal Reserve’s December decision to raise rates was a catalyst for the market’s infarction, which could ultimately end the expansion. That view is a bit challenging. The Fed had proper motivation for moving, previewed it extensively, and signaled a cautious posture for the future. And the move was only 25 basis points.

Ultimately, whatever is troubling the market may be too much for the expansion to overcome. But it bears noting that the US economy is not without considerable bright spots. The momentum in employment and wages has been impressive. Retail sales growth has been very solid over the past year. Banks are well capitalized and loans are growing nicely. Low inflation is increasing purchasing power. We have plenty of reasons to think that the worst can be avoided.

So let’s not lose faith on the basis of a few difficult weeks in the financial markets. We will certainly have another banana someday, but hopefully, that day isn’t going to come very soon.

Retail Sales: A Race Between Bricks and Clicks

The retail marketplace will change more in the next five years than it has during the last two decades. Investors in retail real estate are concerned about how online sales will affect their investment. A rapid transformation is taking place behind scenes as e-commerce grows.

The last holiday season was marked by strong online purchases but more modest sales at brick-and-mortar stores. Changing consumer habits have a more prominent place in the list of investor considerations in retail real estate than they did a few years ago.

E-commerce sales have registered double-digit gains in eight of the last ten years and are projected to add up to more than 0 billion in 2015. Online sales currently make up less than 10% of total retail sales, but industry experts project this share to expand to 30% in the next 15 years.

As mouse clicks do the walking to purchase clothes, books, toys and the like, demand for retail space should suffer and vacancy rates should increase. Indeed, there are more unoccupied retail spaces now than there were 10 years ago.

There are two factors at play. One, the abrupt reduction in demand following the Great Recession explains a large part of the increase in the vacancy rate. But, it is worrisome that even after nearly seven years of economic growth, the vacancy rate for retail space stands at an elevated level. Two, the growth in online retail sales has probably left investors questioning the long-term profitability of traditional retail centers.

Reflecting the high vacancy rate, the effective rent (asking rent less discounts) shows only a modest acceleration in the entire expansion. The most recent effective rent is close to the peak seen in 2007, which is a long wait for retail real estate investors.

Amid these developments in the traditional sector, the division between industrial and retail space is blurring. The rise of e-commerce and the need for distribution centers to stock traditional stores and to satisfy online customers is evolving fast.

Record stores, Blockbuster, Borders and Circuit City are popular victims of e-commerce. Computers and consumer electronics account for over one-fourth of all online sales, with clothing purchases following close behind.

The new retail model goes under the moniker “omnichannel retailing,” and will combine traditional supply chains with the capability to directly fill online orders of customers. The demand for distribution space to address this new delivery system will be a big force behind growth in the retail-industrial real estate market.

Labor market conditions have improved significantly in the last few months and these developments suggest that discretionary spending should be moderately helpful for retail space. The shrinking time between click-and-knock favors online shopping over trips to the store. Consumers seem to have a preference for “experiences” as opposed to buying “things.” These shifts in consumer fads present an important consideration in the retail landscape.

Online sales are here to stay and will eventually constitute a large share of retail sales. Creative use of existing and future retail properties to ensure consumer engagement will continue to affect both retail and industrial real estate investment.

The Inflation Expectations Conundrum

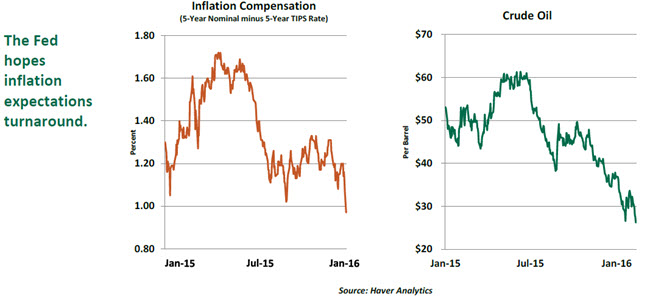

With low unemployment and sustained growth, inflation should move up when commodity prices and the dollar stabilize. The Fed believes this scenario will play out and it is watching actual inflation and inflation expectations closely. Of late, inflation expectations have tumbled; this puts the Fed in a tough spot.

There are different methods to measure inflation expectations: market-based and survey-based. The latter has dropped but is “reasonably stable” in Fed Chair Janet Yellen’s opinion.

The market-based measure, the gap between five-year Treasuries and inflation-protected securities (TIPS), rises and falls with investors’ estimate of how much inflation is likely in the future. Historically, it moves around a very narrow range close to the Fed’s 2.0% inflation target. However, this spread has declined in the recent months and it is slightly less than 100 basis points now.

Yellen pointed out there are other factors affecting market-based inflation expectations. Typically, nominal bonds that are not inflation protected require an “inflation premium.” But, a flight to safety can lower nominal bond yields and compress inflation expectations. This makes it hard to gauge the true nature of inflation expectations. Also, investors in less-traded TIPS may require a “liquidity premium” to hold these securities, which would reduce the difference between nominal bonds and these securities (inflation expectations). Inflation and liquidity premiums change over time and sometimes offset each other and complicate the assessment of inflation expectations. As Yellen noted in her prepared testimony, the Fed believes that changes in the premiums noted above are playing an important role in the downward trend of inflation expectations.

It is also apparent from the data that there is a very high correlation between market-based inflation measures and oil prices, even though the latter make up a very small component of the consumer price indices. If this relationship holds, expectations should return to more reasonable levels when energy prices stabilize and normalize.

Is the Fed willing to tighten in an environment of low inflation and inflation expectations and run the risk of disrupting growth? Given the uncertain signals coming from market-based inflation measures, it is difficult to make a firm conclusion. This is among the reasons that US monetary policy is on hold at the moment, and is likely to stay that way for quite some time.