The markets continue to display impressive strength with a bullish outlook for the short to long-term view. We have a broad-based rally where every sector is participating as well as every market cap. The only thing cautionary point right now is that the market is clearly overbought even as market breadth confirms recent new highs.

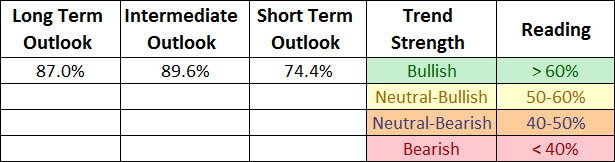

S&P 500 Trend Strength

* Note: Numbers reflect the percentage of members with rising moving averages, 200d MA is used for long term outlook, 50d MA is used for intermediate outlook, and 20d MA is used for short term outlook.

S&P 500 Member Trend Strength

Breaking out the 500 stocks within the S&P 500 into their respective sectors and viewing their long (200d SMA) and intermediate trends (50d SMA) shows the defensive sectors are surfacing as short-term leaders as they possess the strongest short-term breadth (% of members above their 20 day moving average). The most important section of the table below is the 200d SMA column which sheds light on the market’s long-term health. As seen in the far right columns, you have 87% of the S&P 500 members with rising 200d SMAs and 85.2% of its members above their 200d SMA with all ten sectors in bullish territory as more than 60% of their members have rising 200d SMAs.

Source: Bloomberg

Market Momentum

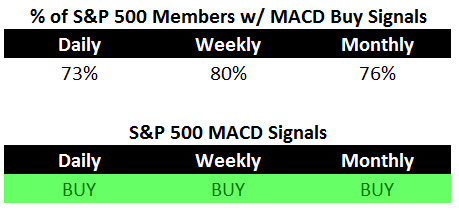

The Moving Average Convergence/Divergence (MACD) technical indicator is used to gauge the S&P 500’s momentum, on a daily, weekly, and monthly basis for short, intermediate, and long term trends. The daily momentum for the market remains bullish as the percent of stocks within the S&P 500 with daily MACD BUY signals currently rests at 73%.

The intermediate momentum of the market remained steady at a strong 80% this week. Further evidence that there has been no dent in the markets longer-term outlook is the slight improvement with the percent of S&P 500 members with monthly MACD BUY signals rising to 76%.

With the daily, weekly, and monthly numbers in bullish territory, it’s not surprising to see that the S&P 500 itself has a BUY signal for all time frames.

52-Week Highs and Lows Data

We have a well-represented market rally as more than one third of the entire S&P 500 hit a 1-year high in the last five days. As seen below, we have a very robust market rally on our hands and there is very little red below except in the commodity-sensitive sectors like energy and materials. A bullish sign for the market is that the cyclical financial sector is the top performer with more than half its members hitting 1-year highs in the last five days.

Taking a historical look at 52-week highs and lows we see that 52-week lows remain absent while 52-week highs continue to remain strong. While we are becoming overbought and due for a pullback, I would expect any pullback to be mild in nature and unlike the two corrections in 2012 as we are not seeing the same degree of negative divergences in new 52-week highs now as we did leading up to those two tops.

Source: Bloomberg

Indicator Summary

The trend and momentum breadth sections above highlight a very healthy market in which there is broad-based participation occurring versus a few select sectors leading the market higher. However, we are currently overbought and due for a short-term pullback as the percent of S&P 500 advancing issues (blue panel) and up volume (red panel) recently hit two standard deviations above the mean. Additionally, sentiment is currently not at favorable levels and may pose a risk to the market’s ability to advance much further before cooling off.

Source: Bloomberg

Summary

The market continues to march higher in 2013 as the short-term to long-term trends and momentum for the S&P 500 remain bullish. The market is currently rallying on broad-based participation and thus is not showing any of the major warning signs of a significant top which is typically characterized by selectivity. While the market’s internals remain very healthy, the market is overbought and sentiment levels remain elevated, leading the market prone to a pullback.