Overview:

- Falling oil prices should lead to positive economic surprises in coming months

- Reflationary global central bank response is building to help global growth in 2nd half of 2015

- Relative performance of early to late cyclicals already discounting global economic trough

“I skate to where the puck is going to be, not where it has been.”

–Wayne Gretzky

In my last article I highlighted that investors should be on high alert for a market decline as we are seeing building financial stress across the globe. That said, I am seeing some potential opportunities in the months ahead since we are starting to see signs of a recovery in Europe (see here), which may also coincide with improving global economic data given the sharp slide in oil-related costs. Since oil prices tend to lead economic surprises by several months, it'll be important to monitor the Citigroup G10 Economic Surprise Index for a potential move higher.

Source: Bloomberg

A deflationary wave has swept across the globe over the last year, pushing global bond yields down and inflation rates below 1%. The list of countries with inflation at or below 1% continues to build with many now experiencing outright deflation.

Source: Bloomberg

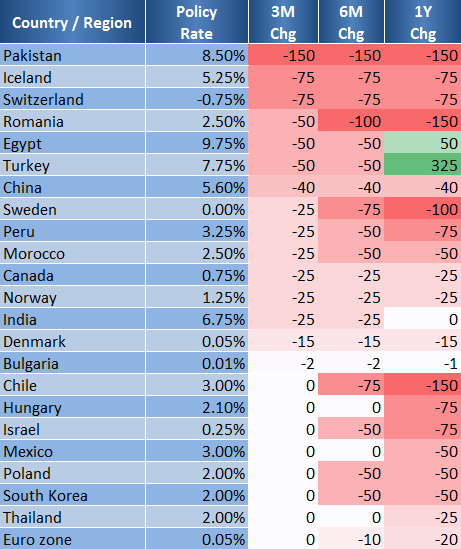

In response, many central banks are slashing interest rates with some, like the Swiss, even going into negative territory. Here is a table of current policy rates for various countries, which have all been cutting over the past 3-6 months.

Source: Bloomberg

As central banks across the globe cut interest rates, the list of countries with yields at or below 1% has grown.

Source: Bloomberg

To put all this in perspective, here are some amazing facts from Bank of America Merrill Lynch:

- 83% of global equity market cap is currently supported by zero interest rate policies (ZIRP)

- 52% of all global government bonds yield less than 1%

- There is now .3 trillion of negatively-yielding government debt in the Eurozone, Switzerland and Japan.

- 1.4 billion people are experiencing negative real interest rates across the globe

Additionally, currencies across the globe have plunged relative to the dollar and the decline in their currencies should provide a lift to exports as their goods become cheaper. A list of sharply declining currencies over the last year is shown below with Russia and Ukraine taking the lead.

Source: Bloomberg

Even the Fed appears to be finally paying attention to international affairs more closely. It recently added "international developments" to its list of reasons to be patient on raising rates:

“This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. Based on its current assessment, the Committee judges that it can be patient in beginning to normalize the stance of monetary policy.”

Based on the global reflationary wave from central banks and the tailwinds from falling commodity prices, inflation, and currencies, the global economy should begin to reaccelerate in February/March of this year. I highlighted last week that the relative performance of early to late cyclicals is a great leading economic indicator (LEI) that often leads other well-known LEIs and, based on the improved relative performance, I made the case for a European recovery. Looking at global early to late cyclicals shows that Europe will not leave the rest of the world behind as we should see a trough in the OECD LEI in February/March of this year.

Source: Bloomberg

Summary:

It is always darkest before the dawn and currently we are seeing the biggest global reflationary wave since 2008/2009 as central banks across the globe are slashing interest rates and expanding their balance sheets. Monetary policy acts with a lag and in the months ahead we are likely to see its effects as global growth should pick up with the added tailwinds from falling commodity prices and inflation. Based on the performance of early to late cyclicals we could see a bottom in global growth beginning in February and March, which could lead to a strong rally in risk assets.

While a significant bottom in global growth is likely in the months ahead, risk assets are still susceptible to market weakness as they’ve been diverging from the credit markets for several months. For the all-clear to be seen, credit markets will need to move in the right direction. Until that happens, investors should remain vigilant and defensive.