Summary

- World markets are in the midst of a growth scare.

- Greatest concern is centered on Europe, which should continue to decelerate.

- Stock market breadth has worsened as the bears are now in control.

- While major indexes show mild declines, stealth bear market has occurred in most stocks.

Global stock markets are being pressured to the downside amidst a global growth and deflationary scare. Since August most developed country economic reports have surprised to the downside as seen by the Citigroup Economic Surprise Indexes. The only major economic region still in positive territory is the U.S. (blue line) but even in the U.S. the magnitude of positive economic surprises has moderated since September.

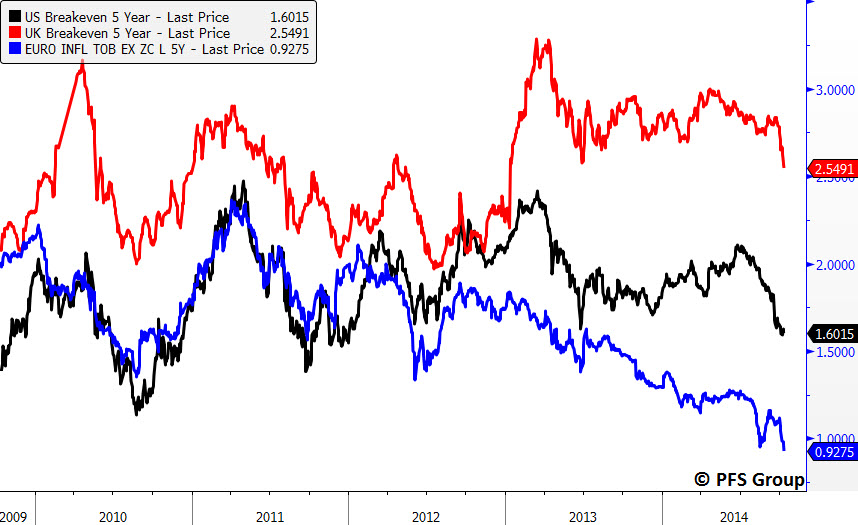

The deflation scare is sending commodity prices tumbling and the U.S.D higher and global breakeven inflation rates tumbling with Euro breakeven inflation rates hitting a new low and U.S. breakevens probing 3-year lows.

To throw more coals on the fire the International Monetary Fund (IMF) cut its forecast for world growth on Tuesday as it warned that stagnation in Europe coupled with a slowdown in emerging markets and ongoing political tensions with Russia will weigh on a fragile global economy. The IMF cut its forecast for global growth down to 3.3% from 3.7% for 2014 while at the same time upped its 2014 U.S. forecast from 1.7% to 2.2%.

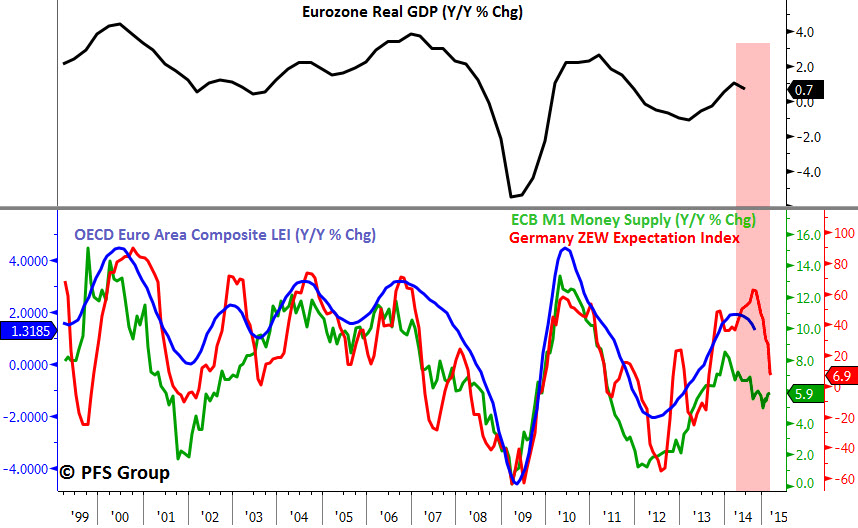

Growth worries are primarily centered on Europe as the German ZEW Index has taken a nosedive recently and suggests a sharp deceleration in Eurozone GDP given Germany is Europe’s economic engine. Based on M1 money supply growth rates for the Eurozone as well as the OECD Euro Area leading economic indicator (LEI) it is highly likely European GDP growth has peaked and will decline heading into 2015.

As shown above, the last growth scare in Europe came in 2011 through 2012 and back then concerns about sovereign debt defaults in Europe ran rampant with the advent on the term “PIIGS” (Portugal, Italy, Ireland, Greece, Spain) surfacing as those were the hotspot countries. Interestingly, this time around investors are not worried about sovereign bond defaults given the lack of upward movement in credit default swaps (CDS) for various European countries relative to the dramatic spikes seen in 2011.

|

|

Source: Bloomberg

It thus appears investors believe the European Central Bank (ECB) will act as a financial backstop but at the same time investors are also factoring in that the efforts by the ECB will be too slow moving and not dramatic enough to turnaround economic growth, which is illustrated in the epic /barrel plunge in Brent crude oil prices in the last four months.

The concerns over a European slowdown are impacting U.S. markets where large cap companies have significant exposure to Europe. Analysts are ratcheting down their earnings expectations as stock prices continue to fall. It appears investors began to discount the growth scare well in advance as market breadth began to deteriorate several months ago. In a July 25th article (click for link), I highlighted that the deteriorating breadth data in 52-week new highs and lows suggested caution as fewer troops were following the generals up the hill. In the article I highlighted how monitoring 52-week new highs and lows data could be used for identifying major market tops with commentary reprinted below:

Respecting the Message of Bob Farrell’s Rule #7

Intuitively, during market rallies new 52-week highs will obviously be larger than if the markets were declining and new 52-week lows will be expanding more during declines than rallies. What is key though is looking at the size of spikes in new 52-week highs during rallies in a bull market compared to spikes in 52-week lows during bull market pullbacks. During the process of putting in a bull market top, breadth deteriorates and stocks begin to move into their own individual bear markets beneath the surface while the major indexes move to new highs. Near the market’s peak we see a hand-off between the bulls and the bears in which the spike in new 52-week lows during a pullback exceeds the spike in new 52-week highs during the preceding rally.

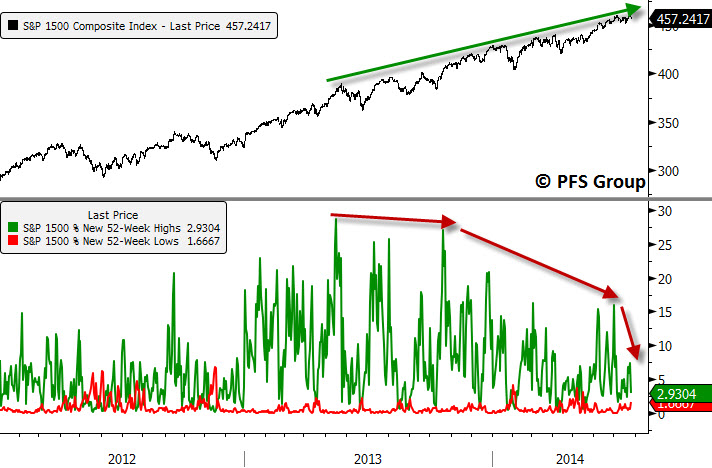

Here is a chart I presented showing that new 52-week highs on rallies continued to dominate new 52-week lows on pullbacks, but what concerned me was that breadth was narrowing as fewer stocks were making new highs along with the market hitting new highs.

Not anymore. The recent decline in the market has led to a spike in new 52-week lows in the 1500-member S&P Composite, which now exceeds the prior spike in new 52-week highs during the September rally. The last time this occurred was during the mini bear market in 2011 and before that in July 2007 as the market was peaking.

The health of the market has now suffered some internal damage and, given new 52-week lows have surpassed 52-week highs, investors should be on high alert for greater losses until signs of stabilization are present. While the decline in the major indices appears to be mild, it has been anything but as the mega cap stocks are masking the damage in the wider market.

Looking at the Russell 3000, which comprises 98% of the entire U.S. equity market cap, shows the 3000-member index down 5.53% from its highs as of 10/09/14 while its average member is already in a bear market with a 23.4% decline. The average small cap stock in the Russell 2000 Index is down 27.35% from its 52-week high while the index itself is only down 12.5%. Moving over to the NASDAQ shows even a greater decline with its average member down 30% while the index is only down 6.4%.

Summary:

Markets are currently in a deflationary scare environment, which is putting bond yields, stocks, and commodities all under pressure. The greatest source of growth angst is coming from Europe as economic growth should continue to weaken for the rest of 2014. While U.S. growth remains solid, U.S. investors are focusing their attention abroad due to most large cap U.S. companies holding a portion of their sales abroad.

The damage done to the markets is far greater than appears on the surface as major indices have only experienced mild pullbacks. However, looking at the average decline among thousands of stocks listed on U.S. exchanges and within large indices reveals a stealth bear market occurring and investors should continue to play defense until signs of stabilization emerge. With new 52-week lows now exceeding the prior spike in new 52-week highs, the bears are in control of this market and the burden of proof has now shifted to the bulls to make their case.