What does a Trump Presidency mean for the economy and the markets, and does it alter our defensive posture? The short answer is no, and here's why.

Trump has made it clear that he wants to lower taxes, roll back suffocating regulations on businesses, and increase fiscal spending on infrastructure projects. This is clearly pro-growth and should this strategy achieve its desired effects to stimulate the economy, our outlook for a potential recession in 2017 could be delayed.

However, there are two very important points we should keep in mind: the government does not have a magic wand or a crystal ball! Fiscal stimulus programs are subject to very long delays and, in terms of timing, are almost always enacted long after a recession has already started.

If you think about it, this makes perfect sense since calls for fiscal stimulus aren’t typically acted upon until it’s obviously needed and by then, of course, it’s too late. Consider Maybe Too Little, Always Too Late:

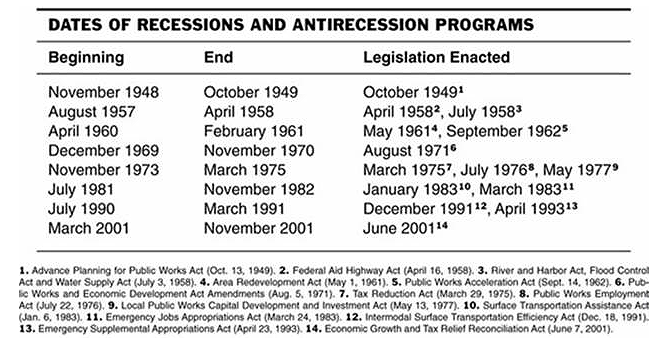

The history of anti-recession efforts is that they are almost always initiated too late to do any good. This chart, based on recession timelines from the National Bureau of Economic Research, shows the enactment of stimulus plans is a fairly accurate indicator that we have hit the bottom of the business cycle, meaning the economy will improve even if the government does nothing.

Consider the following:

- Obama won the 2008 election and his 0 billion "shovel ready" infrastructure package was unveiled in 2009, well after the recession had already started.

- George W. Bush won the 2000 election only to inherit a recession in 2001; similarly, his fiscal policies weren't enacted until the economy was already in recession.

- Ronald Reagan won the 1980 election and yet faced a recession in his first year in office.

The few examples above should make it clear that an incoming president is not powerful enough to repeal the business cycle. Even the Republican sweep under the first two years of the Dwight D. Eisenhower Presidency, which led to the massive Federal Aid Highway Act, was not able to prevent a recession from occurring the very next year.

As of now, we are faced with an economy that is decelerating and showing faltering growth characteristics, the hallmark of a business cycle in its latter phases. While Trump's fiscal agenda may stimulate the economy once enacted, there is still a great deal of uncertainty over his trade policies, which may themselves lead to a recession, as the Peterson Institute for International Economics warned in September. Suffice to say that a bullish economic expansion for 2017 is by no means guaranteed.

While the uncertainty of US elections is now firmly behind us, many other uncertainties still remain and will likely keep investors on their toes in coming months and quarters. Generally speaking, voters all over the world seem to be getting out of their chairs and yelling, "I'm mad as hell and I am not going to take this anymore," in their own version of the famous scene from the 1976 film Network.

We saw this first with Britain's exit from the EU ("Brexit"), now with Trump, and we have the potential to see this again in December with Italy.

Depending on how the Italian referendum goes, the wheels may be put in motion for Italy to become the next country to leave the European Union, which would have tremendous economic and financial market implications given their country has the third largest amount of public debt in the world.

The movement against established political systems is one of the largest sweeping changes we've seen probably since the Arab Spring. One of our most popular guests, Felix Zulauf, described this trend and how he thought it would impact investments, global capital flows, and various asset classes in our conversation with him on our podcast in August. Click here to listen.

Overall, due to the heightened geopolitical and economic risks we see continuing in the months ahead, we are not yet ready to give the all-clear. A Trump Presidency will clearly impact various sectors and the investment climate in general but, for now, we still believe a defensive posture is prudent.