The global economy is slowing as are inflationary pressures. This is the type of backdrop from which we have seen increased monetary stimulus. If the past history of the last three years has been any guide, we should expect the world’s biggest central banks to begin easing once again, with any talks of “tapering” largely premature.

The Perfect Cover To Print

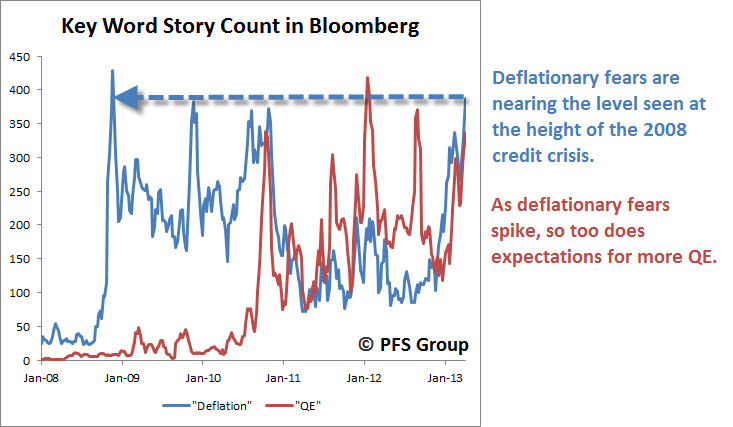

Since the middle of last year we have seen fears over a resurgence of deflation pick up. In fact, measuring the news count for stories with the word “deflation” in them have spiked to levels not seen since the height of the 2008 credit crisis. Associated with deflationary fears is the belief of more “QE” by central banks as seen below where spikes in “deflation” coincide with spikes in “QE.”

Source: Bloomberg

Fears over deflation are stemming from the fact that the developed economies of the world have been in a disinflationary mode since the middle of 2011, with many countries annual inflation rates resting at levels not seen since early 2009.

Source: Bloomberg

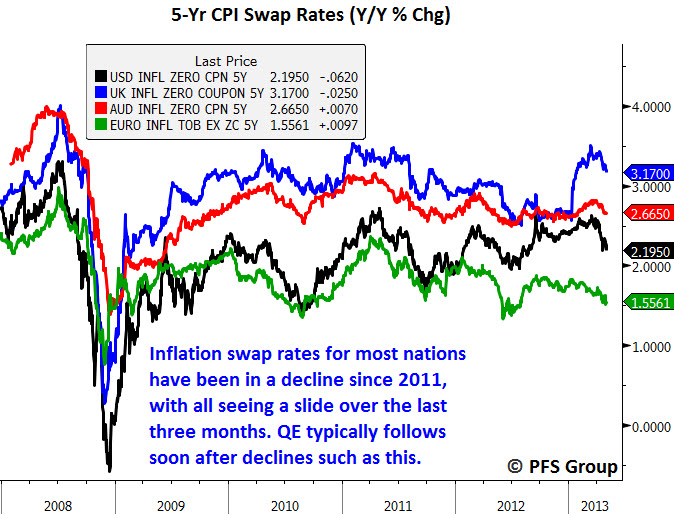

Inflation expectations as measured by 5-year CPI swap rates have also been on the decline since 2011 with the U.S. and U.K. seeing the sharpest recent declines in inflation expectations.

Source: Bloomberg

Part of the reason behind declining inflation rates since 2011 is that economic growth rates have largely stalled in developed nations after peaking in 2011. The Eurozone is currently in contraction territory with a PMI less than 50 (above 50 indicates growth, below 50 indicates contraction) while the U.S. is barely positive at a reading of 50.70 and the world’s economic juggernaut, China, rests at a stall speed of 50.60. The only country seeing real improvement this year is Japan after hitting a low of 45 last December which has since pushed into growth territory with a reading of 51.10 in April.

Source: Bloomberg

One of the things I pointed out last week in my article was that we had an about face by the G20 financial ministers who, as we entered the year, were denouncing “Abenomics” in Japan and accusing the nation of starting another global currency war. However, at a recent meeting the G20 ministers appeared to have a change of heart as the following article illustrates.

Shares rebound, dollar dips vs yen

Japanese officials said that the Group of 20 nations accepted that the country's .4 trillion stimulus program is aimed at conquering 15 years of deflation rather than at weakening the yen.

"The lack of pushback by the G20 effectively gives the BOJ room to ease further if needed and should keep the yen biased broadly lower," said Omer Esiner, chief market analyst with Commonwealth Foreign Exchange Inc in Washington, DC.

The G20's actions removed any remaining obstacles to further yen weakness, setting up a test of the symbolic 100 yen to the dollar level and boosting demand for Japanese stocks.

The change in heart towards Japan likely reflects other nation’s desires to print more money against the backdrop of declining inflation and economic growth rates. Expansion of monetary stimulus will likely be seen in the coming months in hopes of reviving economic growth rates as Japan has done this year.

It’s The End Of Austerity As We Know It….And I Feel Fine

At the same time we see slowing economic growth and waning inflationary pressures, there is also a renewed rejection of the principle of austerity and fiscal discipline. If the move towards austerity is rejected in Europe we could see the monetary flood gates open as there appears to be a face-off between Germany and the rest of Europe.

Italian showdown with Germany as Enrico Letta rejects 'death by austerity'

Italy’s new premier Enrico Letta is on a collision course with Germany after vowing to end death by austerity, and warned that Europe itself faces a “crisis of legitimacy” unless it charges course…

It comes as France, too, appeared close to breaking ranks with German-imposed policy doctrines. A leaked version of French president Francois Hollande’s Socialist Party’s text openly attacked “German austerity” and the “egoistic intransigence of Mrs Merkel”.

While the text has since been toned down to the “liberal politics of the German Right”, the episode has stunned Berlin and threatens irreparable damage to the Franco-German relationship that anchors the EU Project.

The ground is also shifting in Brussels, where EU employment chief Laszlo Andor called on Monday for a radical change in EU crisis strategy. “If there is no growth, I don’t see how countries can cut their debt levels,” he told the Süddeutsche Zeitung.

In a direct attack on Berlin, he said the German practice of “wage dumping” within EMU to gain larger export surpluses “could not be justified”. The surplus states have to changes their policies as well as the crisis states. “Otherwise the currency union will break apart. Cohesion is already half lost,” he said.

As the following dichotomy between Germany and the rest of the Eurozone’s unemployment rate shows, clearly Europe as a whole would like to see more monetary stimulus and more restraint on fiscal tightening (austerity) while Germany is doing just fine. That said, the German unemployment rate has stopped falling after three years of decline and actually ticked up late in 2012 and may be on upswing. While Angela Merkel may have support at home for sound monetary policy when unemployment rates are falling, her domestic support at home may begin to deteriorate against a backdrop of rising unemployment.

Source: Bloomberg

The attacks on austerity are likely to continue as the following article illustrates:

Debt and Growth - Attacking Reinhart-Rogoff to revive the spending machine.

Perhaps you've read that America's debt burden is no longer a problem. Former White House economist Larry Summers says the U.S. should borrow even more money today because interest rates are low, and his Keynesian brethren are busy trying to discredit economists Kenneth Rogoff and Carmen Reinhart for their famous claim that a country's economic growth begins to fall when debt hits 90% of GDP. Time for Stimulus 5.0!...

The Keynesians are attacking Reinhart-Rogoff with such vitriol now precisely so they can rev up the spending engines once again. In their economic model, more government spending equals more GDP. So governments must keep spending more no matter what they spend it on.

Summary:

We are witnessing the perfect backdrop to see renewed monetary stimulus by the world’s central banks as both inflationary pressures and economic growth rates decline from peak levels seen in 2011. Japan appears to have kicked things off this year with the initial reaction by the G20 as clearly disapproving, though the complete change in rhetoric towards Japan suggests the G20 is likely planning on ramping monetary stimulus themselves and would be hypocritical in condemning Japan. Austerity has been the big move in Europe over the last few years but with a massive divergence in unemployment rates between Germany and the rest of Europe, how long can Germany keep the austerity move going by its neighbors, particularly when German unemployment appears to be on the rise.

The fuse for the rejection of austerity is likely to be the realization of a math error in the Reinhart-Rogoff study, which argues for austerity when debt levels begin to reduce economic growth rates. Keynesians across the globe are seizing upon the realization of this error in hopes of ending the austerity move and ramping up both monetary and fiscal stimulus. If we do end up seeing a coordinated move by global central banks to print more money, we may be setting up for a strong second half rally in global equities.