Many of the readers of my articles should know by now that I place a large emphasis on monitoring the business cycle. The chief reason for this is that the business cycle plays a huge role in investment returns. During economic expansions equities typically outperform fixed income investments while the converse is typically the case during economic downturns. Additionally, equity returns among various sectors such as early cyclicals (financials, consumer discretionary), late-stage cyclicals (energy, basic materials), and non-cyclicals (consumer staples, health care) fluctuate depending on where we are, which is often referred to as sector rotation. Knowing where we are within the business cycle can help investors to better position themselves for superior returns. Current analysis of the business cycle suggests a period of slower growth ahead, not just in the U.S. but also globally.

Head of ECRI Calling for Global Slowdown Ahead

Lakshman Achuthan, founder and managing director of the Economic Cycle Research Institute (ECRI), is calling for a slowdown in global economic growth by this summer, and made this call in January in a report to their clients, well ahead of the now visible cracks in global growth. Shown below is the ECRI’s Leading Indicator of Industrial Growth (top line of figure below) that provides a long lead time to global industrial production and commodity inflation. It peaked late in 2010 and is forecasting a slowdown in industrial growth by this summer and weakness persisting through much of the rest of the year.

Global Industrial Growth Downturn

Based on our Long Leading Index of global industrial growth, we expect a downturn to start by summer. Beforehand, prominent shorter-leading indicators of industrial growth, like JoC-ECRI industrial commodity price inflation, will start weakening.

Source: ECRI

Explaining their call for a global growth slowdown ahead, Lakshman Achuthan was recently interviewed on Yahoo’s The Daily Ticker, with excerpts from the interview provided below (emphasis added).

Global Slowdown to Hit by Summer, Even for U.S., Says Achuthan

The world is headed for an economic slowdown, according to the Economic Cycle Research Institute's (ECRI) Long Leading Index of global industrial growth.

"It is not country specific, but imagine if you could add up all the activity in factories around the world and see if it was accelerating or

decelerating, that is what this indicator is focused on," says Lakshman Achuthan founder and managing director of the research center. "And it has been telling us very clearly, unambiguously, that we have a peak in global industrial growth this summer…”

The Good And The Bad

The good news as the slowdown quickly approaches is that Achuthan does not believe another recession is headed our way.

The bad news is he says "the U.S. economy will not escape" the downturn, but will "participate in it…and in one way, shape or form, it is going to impact this recovery."

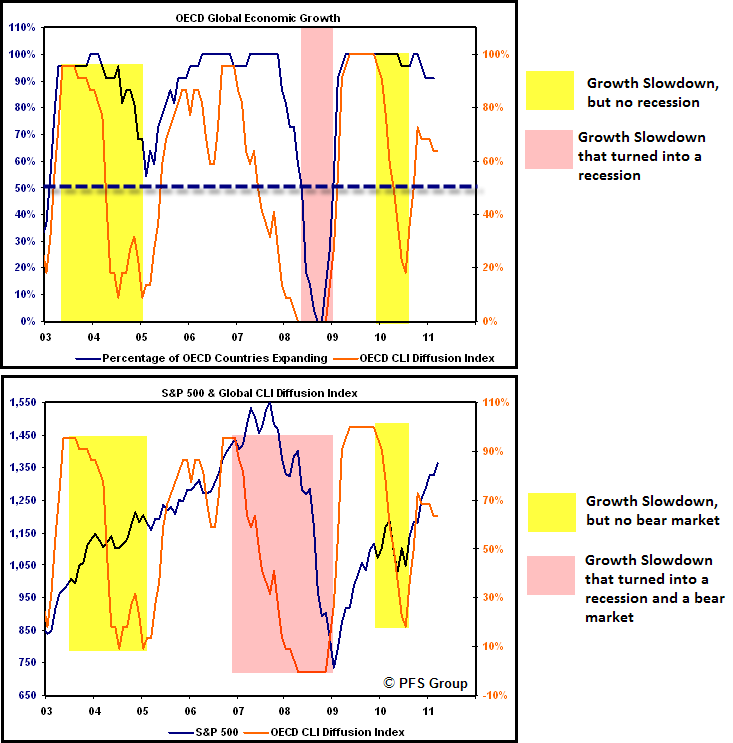

My own analysis lines up with Mr. Achuthan as my OECD CLI Diffusion Index (orange line below) has peaked and has been turning down now for several months as fewer and fewer OECD nations are experiencing accelerating growth. While many global economies are already beginning to decelerate, more than 90% of OECD countries are experiencing positive economic growth. This can be seen by the blue line below which shows the percentage of OECD nations with expanding economies. We have had two growth slowdowns over the last eight years that did not lead to a global recession. We had one in late 2004 as well as 2010 as my OECD Diffusion Index fell off sharply, though the percentage of OECD economies expanding showed more countries expanding (> 50%) than contracting.

Source: Bloomberg

Both of those global slowdowns witnessed flat to negative 1-year returns in the S&P 500 but no bear market. This was not the case in 2008 as the global slowdown turned into an outright recession as we went from 86% of OECD countries experiencing expanding growth heading into 2008 which then plummeted to 0% by the fall, which also produced the first bear market in the U.S. since 2000.

As we sit right now, there is clear evidence that the U.S., as well as the global economy, will experience a growth relapse ahead according to the ECRI. The three U.S. regional Federal Reserve surveys below are rolling over and the prices paid component suggests U.S. growth may continue to slow throughout the rest of the year.

Source: Bloomberg

While the case for a growth slowdown ahead is easily made, there is not enough evidence to make a recession call. Our recession model typically provides several months warning before a recession begins and the 20% mark is often the line in the sand with only one false signal (1987) over the last thirty years. Given the current reading rests at a 3% probability of a recession beginning over the next 6 months, I am in agreement with the ECRI’s Lakshman Achuthan that a recession is not in the cards as of yet.

Source: Bloomberg

Investment Implications

Rather than reinventing the wheel, I’ll refer readers to the article I wrote last week in which the last portion of the article highlighted what the investment implications were for a slowdown ahead (Why Bill Gross is Wrong…In the Short Term). In a nutshell, defense is likely to outperform over the next six months which would mean that in terms of asset classes, bonds will likely outperform stocks. In terms of sectors the non-cyclical sectors such as health care and consumer staples will benefit from sector rotation as investors decrease their allocation to cyclical sectors like consumer discretionary and financials and lower their portfolio’s risk profile.

Incoming data will be key to monitor ahead to gauge whether we will reaccelerate like we did at the end of last summer or if the coming growth slowdown will morph into another recession.