Credit markets across the globe and particularly in Europe have improved over the last few weeks after ECB president Mario Draghi said the ECB would do “whatever it takes” to ease tensions in Europe. So far all we have are promises from Draghi and we have yet to see any concrete action but promises alone have been enough to bring down financial stress. That said, the Euro crisis is far from over as there are hundreds of billions of dollars of various governments in the Euro Zone that mature over the coming year and overall tensions remain elevated.

So Far Promises Are Enough

It appears market participants are taking Draghi’s words seriously as credit markets have eased since his “whatever it takes” remark a few weeks back with credit conditions also improving in the U.S. This can be seen by looking at Bloomberg’s Financial Conditions Index for the U.S (top panel) and Europe (bottom panel) which shows conditions have improved since weakening in June. Coincident with an improvement in financial conditions has been strength in the equity markets.

Source: Bloomberg

Equity markets in Europe have been particularly strong over the last few weeks with Germany’s DAX index 3.5% off a 52-week high and France’s CAC 40 Index 4.6% off from a new 52-week high. In the U.S., the S&P 500 is 1.16% away from making a new 52-week high and 10.8% away from making an all-time high. Clearly equity markets are expecting some type of action coming from the ECB in the coming weeks and Draghi’s “whatever it takes” comments may be viewed in the same light as Fed Chairman’s Bernanke’s August 2010 Jackson Hole comments which ignited a market rally prior to the Fed taking any concrete action.

Source: Bloomberg

In addition to improvement in the equity markets credit default swaps (CDS) for the Euro hot spots Spain and Italy have eased considerably since July and Spanish banks have seen a bit of a reprieve.

Source: Bloomberg

Coincident with the improvement in default rates for Spain and Italy is an improvement in 10-yr bond spreads relative to Germany. In the July peaks credit spreads for Spain and Italy with German have come down but not to the same extent as they did after the LTRO ECB announcement late last year. We may need to see concrete actions before we get any serious improvement in bond spreads but at least we are currently heading in the right direction.

Source: Bloomberg

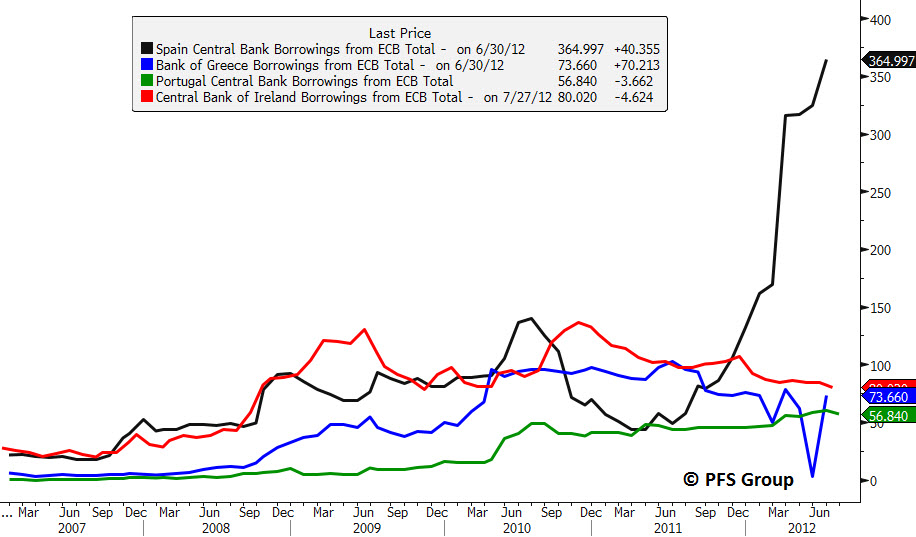

There is still a tremendous amount of sovereign debt to rollover in Europe and as long as yields remain high the ECB is likely to be lender of last resort. The debt crisis in Europe is far from over and right now Spain is taking center stage from Greece given its size and financing needs. As of now you can take the combined ECB borrowings by Greece, Portugal, and Ireland and they are still less than Spain’s as seen below.

Source: Bloomberg

While credit markets have eased over the last month they will likely remain jittery until the ECB begins to take concrete steps to address the sovereign debt markets. If Draghi’s bite is not equal to his bark then the markets disappointment will likely be reflected quickly with renewed weakness in the debt and equity markets. However, if Draghi does follow through with actions we may yet repeat the 2010/2011 cycles of strength in the final third of the year as the wash-rinse-repeat cycle continues.