In our “NBER Recession Model – Confirmation of last resort” research note we constructed a co-incident U.S economic composite based on the 4 indicators watched by the NBER, namely Industrial production, Personal Incomes, Retail sales and Payroll employment.

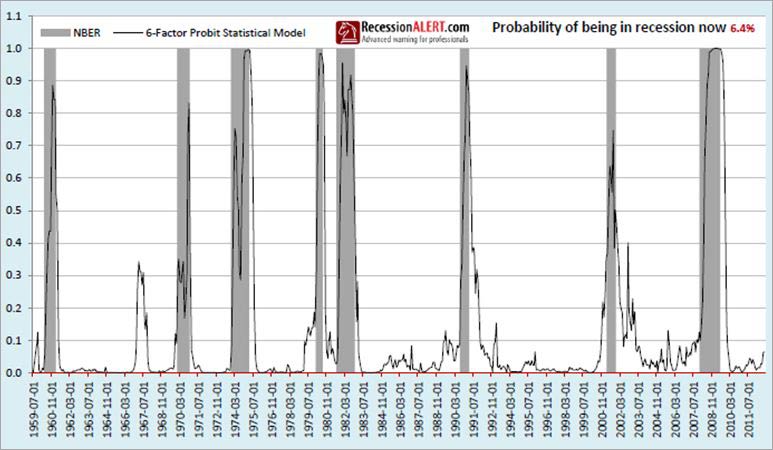

With the nosedives for the August prints for Industrial Production and Personal Incomes, this model is now showing triple the recession probability in August over the prior month, namely 6.8%.

The low prints for Industrial Production and Personal Incomes brought the NBER composite coincident index down to a new 32-month low watermark:

Let’s examine the main culprits for this month’s decline starting with Personal Incomes. You will note we deploy a rather fast-moving short-term 3-month smoothed growth rate (which examines the behaviour of the last 7-month data in the formula) so this model captures trend changes very quickly (and is less susceptible to seasonal anomalies) as opposed to traditional 6-month smoothed and 12 month growth rates.

![]()

The other culprit in August was Industrial Production. Again we deploy a 6-month smoothed growth rate as opposed to the traditional 12-month straight growth to allow for faster response to directional changes and less exposure to structural seasonal changes:

To see just how sub-par this expansion has been, have a look at how it compares to the 7 expansions before it as displayed in the chart below:

Does this mean a recession is likely? It certainly would seem so if the co-incident data continue to decline for the next 2-3 months. However we are inclined to give the economy the benefit of the doubt since none of the mainstream leading indicators are confirming a slide into recession – in fact some of them are putting in a bottom. It is highly likely that the weakness we are seeing in the co-incident data now is just the manifestation (or playing out) of the many leading indicators that started rolling over 5-6 months ago, as shown by our Weekly Leading SuperIndex that rolled over in April 2012

Given the NBER co-incident composite has been declining for 7 months and the leading data seems to have made an attempt to find some support since 2 months ago, we may find the co-incident data decline further for 1 or even 2 months before bottoming out, probably flirting very closely with the recession trigger in the process. Some co-incident data has already showed signs of bottoming, as shown by our “50-State Co-incident Indicator” update note.

Despite the torrid growth of the economy, and the risks this exposes us to for external shocks, we are still of the view that the lack of corroboration of the leading indicators in signalling recession mean it more likely we will skirt it again as with the prior two summer swoons. Even if we are incorrect and the Fed easing continues to prop up the leading indicators whilst we fall into a balance sheet recession due to a fall in final-demand - it is likely that the average 30% correction of the stock market in the wake of recession may not materialize (or be far less severe) and that the recession is a “muddle through recession” just as the “muddle through” expansion that went before it.

Source: RecessionAlert