Most people assume that the mismatch between US federal government revenue and expenses will go away, with enough time. All that is needed is a little “patch” now, and some more time, in order for the mismatch to disappear.

I don’t think the mismatch can be made to go away, partly because the mismatch between government revenue and expense is far worse than most realize. Furthermore, high oil prices seem to lead to recession, making it more difficult to fix the gap between government revenue and expenses.

There is good reason to believe that oil production will not increase materially in the next few years. With oil demand from China and India continuing to increase, the mismatch between oil supply and demand can be expected to get worse with time, leading to more recession, and a greater gap between US federal government revenue and expenses.

Because of these issues, about all recent debt limit agreement can be expected to do is push the problem down the road for a few more months. Eventually, we will be back into recession, and the revenue /disbursements mismatch will be worse than it was the last time around.

Mismatch between Government Revenue and Expenditures is Very Large

The way I look at federal spending is to look federal government revenue and expense on a combined basis (including budgeted programs, off-budget spending, and Social Security) using historical data <https://www.cbo.gov/ftpdocs/120xx/doc12039/HistoricalTables%5B1%5D.pdf> from the Congressional Budget Office (CBO). Instead of comparing amounts to GDP, I compare amounts to non-governmental wages (Private Industry Wages + Proprietors Income) from the Bureau of Economic Analysis, since I believe this gives a more stable base, and since, as a practical matter, most taxes are on wages.

When we look at Federal Government expenditures and revenue in that way, what we see is as follows:

Figure 1. Federal Government revenues and expenditures on a cash basis, compared to non-governmental wages, based on BEA and CBO data.

While revenue is down by about 5 percentage points recently, spending is up by close to 20 percentage points. My calculations include increases in internal debt but do not include increases in external debt, so really reflect what the Federal government has spent on a cash basis. If we categorize outgo based on categories given in the CBO report, and compare them to my non-governmental wage base, this is what we find:

Figure 2. Federal Government Expenditures as a percentage of Non-Government Wages, based on CBO and BEA data.

Based on Figure 2 information, there has been huge growth in the category called “Medicare, Medicaid, etc.” This category would also include unemployment insurance (to the extent it is funded by the federal government), plus many other mandatory federal programs, such as food stamps and Supplemental Security Income. The increase in the “Medicare, Medicaid, etc.” category is easy to understand with the recent recession, because there are many people who are unemployed or underemployed.

My non-budget spending category is determined by subtraction–comparing how much external debt actually increased to the expected increase based on the sum of the various programs. This approach will tend to understate non-budget spending (such as military spending and stimulus spending).

If we look at revenue (Figure 2), also using CBO amounts, we find that the decline in revenue reflects a combination of decreases in all categories, not just personal income taxes. Corporate income taxes are also recently lower, as is the “Other” category, which includes excise taxes (such as on gasoline) and estate taxes.

Figure 3. Federal government revenue breakdown, as percentage of US non-governmental wages, based on BEA and CBO data.

The thing we notice, both from Figure 3 and from Figure 1, is that Federal Government revenues have never exceeded 40% of non-governmental wages for very long. Government revenues are now at 34.6% of non-governmental wages. The drop in individual income taxes started back in 2001, at the same time the percentage of the US population with jobs started declining (Figure 4).

Figure 4. Ratio of number of people employed to US population, based on BLS and Census Department data.

In Figure 1, we saw that the size of the gap between revenue and expenditures was of the order of magnitude of 20% – 25% of non-government wages. If the mismatch between revenue and expense is a permanent one, we really need this much more revenue to fund the current system (not considering the big increase in Social Security payments in the next few years, as “Baby Boomers” retire). But looking at where revenue comes from in Figure 3, there is no possible way to get this much additional revenue. If individual income taxes were to be the sole source of this increase, we would need to triple individual income taxes, to provide enough revenue in total. More taxes on the rich would barely scratch the surface of this problem.

The Reason our Problem is a Permanent One

We are used to thinking of the use of debt as something to be expected, but this is something that is not really true, unless the economy is in long-term growth mode. If the economy is growing (Scenario 1 of Figure 5), it makes sense for the government and individuals to borrow, because the future appears to be better than today, and offers good prospects for debt repayment, with interest.

Figure 5. Two views of future growth

The problem comes when the economy can no longer grow, or actually begins to decline (Figure 5, Scenario 2). Most economists do not even consider this possibility, but in a finite world, at some point, this will have to happen because finite resources deplete. The only exception might be if we can figure out a way to somehow disassociate growth from the underlying resources used to manufacture and transport goods and services, but this seems extraordinarily unlikely <https://www.theoildrum.com/node/8185> .

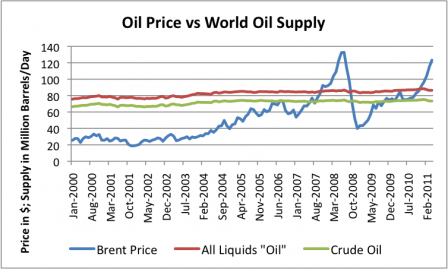

Oil supply has a been a problem since 2005. Regardless of how much price has increased (or decreased), there has been little change in world oil production.

Figure 6. World oil production, compared to Brent price, based on EIA data.

Economists tell us that if an item such as oil is in short supply, prices will rise, and either more of the item in short supply will be found, or a substitute will be found. It seems to me that there is a third alternative, which we are now encountering. In the agricultural world, if a required nutrient is not in available in adequate supply, the yield of the crop is reduced, based on the amount of the limiting nutrient. (This is called Liebig’s Law of the Minimum <https://en.wikipedia.org/wiki/Liebig's_law_of_the_minimum> .) It seems to me that we are encountering the corresponding problem with the economy now, if high oil prices are thought of as a limiting an essential part of the economy.

Oil is used in very specific ways in the economy–for example, in transportation, in growing food, in operating heavy construction equipment, and in making many products including synthetic fabrics, asphalt pavement, and pharmaceutical drugs. There are no good substitutes within any short-term time horizon.

When oil prices increase, consumers tend to cut back on discretionary purchases, because oil price increases tend to cause food and commuting expenses to rise, and these are necessities. Earlier this year, economist James Hamilton showed <https://reason.com/archives/2011/03/08/oil-price-shocks-and-the-reces> that oil price spikes were associated with 10 out of the last 11 US recessions. Now, oil prices are again high, and economic growth during the first half of 2011 was less than 1%. We are again seeing signs of recession. If oil is really a limiting input for the economy, this is exactly the type of response we would expect from high oil prices.

While world oil production is flat as shown in Figure 6, consumption of the United States and many other “developed” nations is down recently, especially during the 2008-2009 recession.

Figure 7. Oil consumption based on EIA data.

The reason for the decline in oil consumption of Europe, Japan, US, and Australia is competition for limited supply. Oil consumption in my “Remainder” category (including China, India, most oil exporting nations, and many small “lesser-developed” countries) is rising rapidly.

I believe the reason for the shift in oil consumption to less-developed countries is because oil consumption tends to go to the countries where the jobs are–in part because the jobs, themselves often use oil, and in part, because those with jobs have the financial resources to buy goods and services made with oil. So as we import more goods from abroad, the countries we buy from prosper, and our own economy meets more recessionary headwinds.

Going forward, it is not at all clear that world oil production (Figure 6) will increase above its current level. In fact, it may very well decrease, as old fields become more depleted. Given the likelihood of continued growth in the “Remainder” category (Figure 7), this means that the United States and other “developed” countries may continue to experience declining oil consumption. Not surprisingly, given this background (high oil prices reflecting limited oil supply tending to cause recession, and oil consumption tending to go where jobs are), low oil consumption seems to be associated with a low number of available jobs (Figure 8).

Figure 8. Relationship between US jobs (from BLS) and US oil consumption (EIA "product supplied")

This relationship becomes even closer when we adjust for the long-term downward trend in oil consumption (Figure 9).

Figure 9 - US oil consumed per person employed, based on EIA and BLS data, with fitted exponential trend line.

An Unwind in Private Debt Makes our Current Problems Worse

When the economy is growing, as in Scenario 1 of Figure 5, it is possible for private debt to continue expanding. But once the economy stops growing and starts shifting toward decline, growing private debt become much less possible. Part of this decline in debt occurs simply because it doesn’t make sense to borrow from the future, and pay back the loan with interest, when the future provides fewer goods and services than today. Also, in a declining economy, businesses see no need to borrow to expand their businesses. Instead, they repay existing loans, and don’t take out new ones. In addition, there tend to be many more defaults in a declining economy. (See my posts The Link Between Peak Oil and Peak Debt – Part 1 <https://ourfiniteworld.com/2011/07/11/the-link-between-peak-oil-and-peak-debt-part-1/> and The Link Between Peak Oil and Peak Debt – Part 2 <https://ourfiniteworld.com/2011/07/13/the-link-between-peak-oil-and-peak-debt-part-2/> .)

When we look at the recent trend in United States non-governmental debt together with the increase in governmental debt, the graph is quite disconcerting:

Figure 9. US Domestic Debt, split between government debt (external only) and non-governmental debt. Based on Federal Reserve Z.1 data. Excludes Foreign Debt.

Our economy is used to the stimulus it gets from increasing debt. The government can try to increase debt to make up for the lack of increase in private sector debt. But if growing debt really no longer makes sense, because of the difficulty the economy has growing when oil prices are high, then attempts to make up for the shortfall in private debt will never work. Private debt will keep shrinking, and government will be too small to make up the shortfall. Furthermore, in a declining economy, repaying governmental debt is likely to prove impossible.

Is There a Solution?

It is hard to see a solution to the mismatch between revenue and expenses. Laying off government workers and cutting back government safety-net programs will tend to be recessionary. Raising taxes will also tend to be recessionary. Low-cost oil has enabled our current standard of living. As low-cost oil is replaced by high-cost oil, we need to expect our standard of living to fall, because we will find the cost of many essential items increasing, without our salaries increasing. Even adding more high cost oil (say, from deep-sea locations) won’t fix this problem.

Government programs have tried to hide the trend toward more job layoffs and a lower standard of living that comes with lower oil consumption through stimulus programs and bailouts, but this cannot continue indefinitely, because the underlying problem has not been fixed. Eventually, the mismatch between government revenue and expense will become more evident, and the government will find it needs to cut back on many popular safety-net programs, or find the interest rates it needs to pay for sovereign debt significantly raised.

The level of changes agreed to today in today’s debt cap legislation is far too low to significantly change the current situation. We will still be left with a wide gap between federal government revenue and expenses, and the likely prospect of recession in the future.

It is hard to fix the mismatch between government revenue and expenditures. One thought is that we need new types of taxes that will discourage “exporting” of jobs, and encourage “importing” of jobs. We need a clear focus on keeping jobs in this country, even if the goods produced here cost more.

We probably also need to work on finding jobs for people, outside of our current oil-based economy. At one point, it was usual for one family member to remain outside the paid work force, and instead work on raising a garden, preserving food, and taking care of children and the elderly. We may need to go back to this model again, as more of the norm.

I am afraid I do not have all of the solutions. If solutions were easy, we would not be in our current dilemma.

Source: Our Finite World