Helicopter money requires central banks to make choices they cannot make while undermining their independence and inflation-targeting mandate. Attempts at explicit fiscal coordination may not be feasible and may create unresolvable conflicts between central banks and political governments.

In the post-financial crisis world, unconventional monetary policy has become so mundane that the name is a contradiction in terms. Everybody does it, few know when they’ll stop it and it has probably been stretched beyond the scope of its abilities. The frustration brought about by the realization of the latter point is such as to make it now popular to consider a more direct version of quantitative easing.

What Is Helicopter Money?

“Helicopter Money” (HM) is an idea named after a parable of monetary policy described by Milton Friedman in 1969. At its core is the idea of bi-passing the intermediation of the financial system in order to give cash created by the central bank directly to consumers. After lying dormant for decades, the idea received attention in 2003 when it was discussed by Ben Bernanke in relation to Japan and again by then-EBRD Chief Economist Willem Buiter.

However, it is only as a result of the recent failures of the already unorthodox liquidity traps they find themselves in that the idea has been gaining traction in policy and financial research circles. Among others, Adair Turner, Willem Buiter, and strategists at Deutsche Bank, have recently advocated the policy. The fact that it was not outright.

QE, Disappointments and the Alternative Offered by HM

In principle, central bank asset purchases funded by the creation of new currency, known as quantitative easing (QE), can impact the real economy in three different ways. It can improve confidence and expectations, raise the value of assets used as collateral thus lowering borrowing costs, and increase the amount of cash being lent.

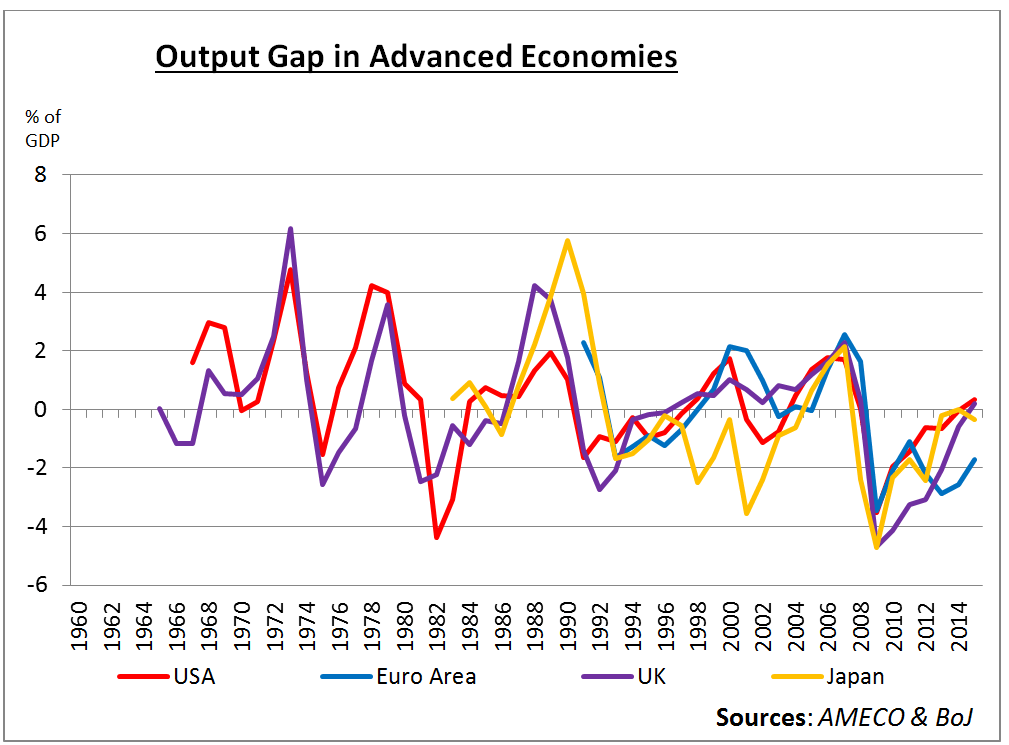

All of these mechanisms should conspire to increase GDP and inflation, but it seems the last mechanism did not quite work as expected. Contrarily to previous downturns, the recovery from the financial crisis has been disappointingly slow, as testified by the recovery of the output gap.

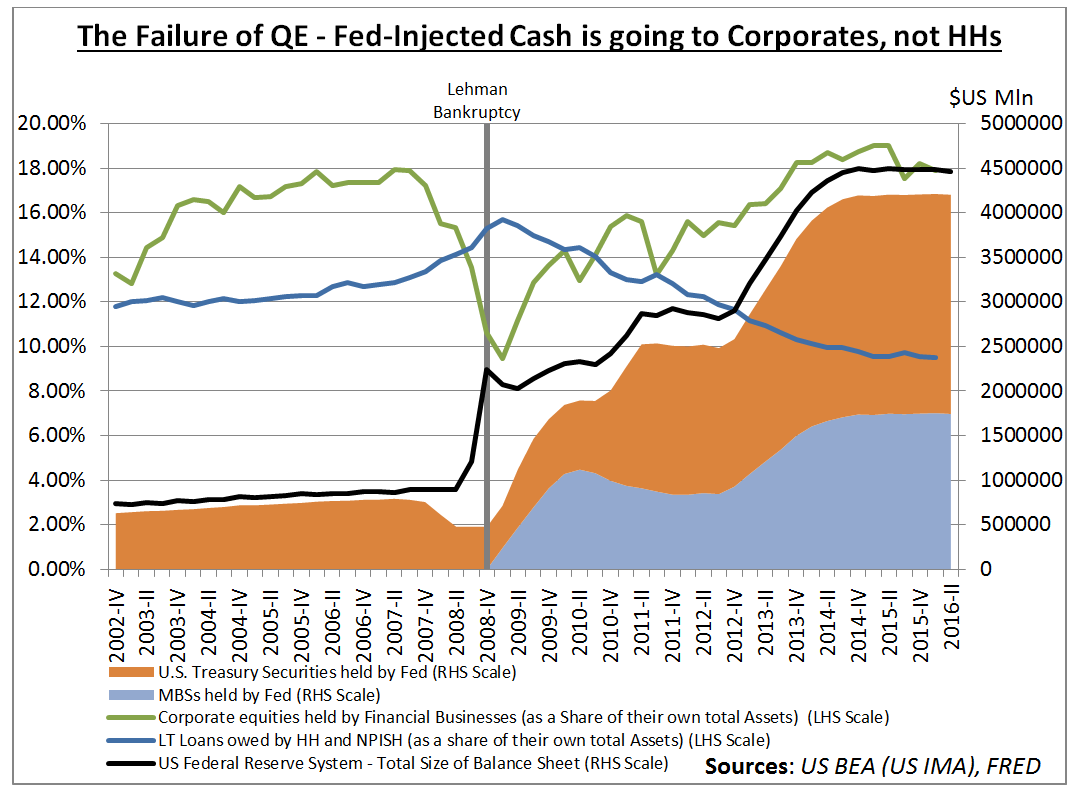

Even in the USA, where QE has admittedly been most successful, its shortcomings are evident. Instead of increasing loans to consumers, the money injected by the Fed through Treasury and MBS purchases was reinvested by banks into corporate equity positions.

With historically high dividends paid by US corporates still trending upwards, the choice makes sense. Unfortunately, QE did nothing to stop the rebalancing of corporate priorities away from relatively higher shareholders payments and lower wages.

HM would bi-pass the intermediation of financial markets that is holding up that end of the recovery. Instead of giving money to banks in the hope that they will then lend the money to households, central banks could give it to households directly.

The Problem With Helicopter Money

Unfortunately, there are several problems with HM. In its purest form, it would require the central bank to answer the very simple question of “Who gets the cash?” HM will inevitably result in a reorganization of the distribution of income which no central bank is legitimately mandated or equipped to pursue. While nominally the adjustment is only relative rather than redistributive, the effect is not uncontroversial. A uniform distribution might be seen as regressive while a focus on the poor might be resented by the rest of the economy.

To resolve this issue, Adair Turner and Michael Woodford have proposed alternative cooperative arrangements between the central bank and the government whereby the first would transfer the cash through the latter. The distinctive feature of this “HM”-flavor of QE is that it would be explicitly conducted to fund fiscal stimulus. This is supported by evidence that when a monetary policymaker supports fiscal policy, fiscal multipliers are large and economic growth is likely to ensue. Woodford and Turner only disagree on whether a GDP growth target or an explicit deficit funding target would be the best tool to ensure that this coordination does not undermine central banks’ independence and their inflation-targeting mandate. However, none of them has addressed the fact that this cooperative solution simply replaces financial by political fiscal intermediation, which would introduce a range of new bottlenecks. This is not a problem if the government is a theoretical welfare maximize, but it real life that seldom is the case.

You may also like Forward-Looking Data Show Growing Risks of Recession

The sudden abundance would certainly remove some of the inhibitions and restraint regarding feeding interest groups. The “flypaper effect” suggests that the government would probably be more careless with its balances once they include explicitly free cash. So inefficiency and corruption may increase. For these reasons, one would expect the government and the central banks to disagree about how to use HM. In that case, one of three things could happen. The government dominates the central bank, much like UK treasury did until the 1990s; the central bank dominates the fiscal authorities like the ECB does in the Euro-Zone; or the central bank cancels HM to avoid the clash. The undesirability of any of these outcomes should undermine the validity of this fiscally intermediated form of HM.

Conclusion

Theoretically, HM should work. Unfortunately, political frictions would most likely undermine its implementation. Its desirability as a process of wealth creation is also debatable. The fact that the policy is only seriously being considered in the UK echoes the dangers and fear created by Brexit and the lengths to which UK policymakers are willing to go to avoid its costs. But perhaps that is the problem itself. Fear of stagnation and of the ensuing political backlash has left politicians unwilling to accept the natural cycle of economic activity and the tough choices that they signed up to make when they began their career. If the solution to the ongoing stagnation is to put more money in people’s pockets, politicians should campaign for it, get elected and do it through targeted fiscal stimulus, rather than expect their central bank to deliver a basic income free lunch.