The following is an edited, public version originally released to clients on August 19th, 2011

It is apparent from the incoming economic data that the economy is slowing rapidly in the US, Europe, and Asia. Unless countered with fiscal stimulus and more QE, it is looking more like there may be a double dip.

As the four charts below from last month's economic data illustrate, the strong second half of the year forecast is looking less likely.

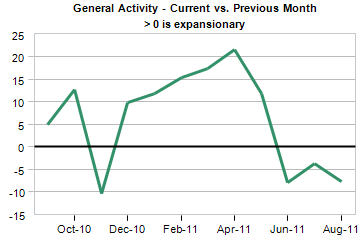

From the Empire State Manufacturing Survey, August 2011

From the Federal Reserve Bank of Philadelphia's Research Department's Business Outlook Survey, August 2011

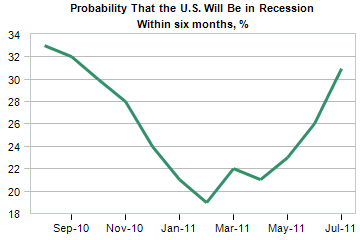

According to Moody's Analytics U.S. Macro Forecast

From the Economic Cycle Research Institute's Recession-Recovery Watch

In fact unless the Administration and Congress come up with a stimulus package soon we could move further into a recession.

Fears over an economic slowdown are causing equity markets to falter. Sovereign risk is not what is worrying the bond markets. Despite our downgrades, Treasury yields are lower today. There are not too many places to go, so fund managers are putting money into bonds. I believe with interest rates zero-bound, bond funds have become the new money market substitute.

There are also concerns over another financial crisis. The next crisis has a high probability of coming from Europe. I believe it is going to take a near-death experience to get the Europeans to act. As I have been saying, the two front tires of the car will be hanging over the cliff before the authorities in Europe react with a big bailout fund, which will be an expanded European Financial Stability Facility, Eurobonds, and lots of money printing. But first comes the crisis.

If a European crisis erupts odds are the Euro will get hit and Treasuries, gold and the US Dollar will rally, perhaps even going parabolic.

The Fed would like to act, and it will, as will Congress. They can't react right now because inflation expectations remain elevated. The core rate came in at 0.4%, and CPI came in at 0.5% last month, and is now tracking at an annual rate of 3.6%. So the Fed is on hold until the equity correction gets bigger, inflation expectations fall, and the talk turns from inflation to a double-dip and deflation.

Commodities remain vulnerable due to a slowdown in the developed economies as well as in China. They will remain vulnerable until the developed world reacts with coordinated stimulus and a monetary response.

Our preference in precious metals right now is for gold. Silver has been underperforming since its high in May due to a weakening economy. Gold does better when the economy is weak or when there is systemic risk in the financial system.

As for "cash," we are very leery of most money market funds right now because we don't know which funds have exposure to high risk European debt such as Portugal, Ireland, Italy, and Spain. As for certificates of deposit, U.S. banks also look vulnerable due to severe losses in their mortgage portfolios. Several of the larger banks such as Bank of America may have to be split apart or restructured. B of A took on too much risk when it bought Countrywide Financial and Merrill Lynch. Both entities held large portfolios of toxic mortgage debt.

Source: Stockcharts.com

We are in a defensive position right now until the crisis passes and the next major stimulus is enacted. Given the next election cycle I believe the next stimulus package will combine elements of both fiscal and monetary stimulus. The U.S. budget deficit is going to get a lot bigger next year. It could possibly approach trillion! It depends how bad the economy gets and how badly our politicians want to get (re)elected.

The Fed has already begun to implement its policy of financial repression by pledging to keep interest rates at close to zero until at least mid-2013. By November/December both parties will come together to enact a massive stimulus program to give the economy another jolt. The Fed will be back to printing more money in order to monetize the government's budget deficits. The Fed will have to do the heavy lifting as it now appears foreign money is starting to exit the U.S as shown in the graph below.

Appetite for U.S. Debt Diminishing

In summary, we are mainly on the sidelines until this storm passes.

All charts from Moody's DismalScientist.com unless otherwise noted.