VOL 2/2, JANUARY 2011

IN THIS EDITION

•MR MIZUNO RETIRES: We have read much in the financial press of late regarding Japan’s poor demographics, chronic government budget deficits and declining household savings rate. Several of these analyses conclude that these factors are negative for the yen. True, all is not well in Japan, but it is important to keep things in perspective. What options does Japan have to deal with an ageing population? Actually, they have several, and theirs are somewhat more palatable than those of the US, UK or even the euro-area. Yes, the Japanese may be gradually retiring, but at least they have saved prudently, and this legacy of savings is negative for US assets and positive for the yen.

MR MIZUNO RETIRES

Today is Mr Mizuno’s last day in the office. He has reached the mandatory retirement age of 60 years old. He is still healthy, sharp as a tack, highly productive and he enjoys his work. He would happily keep working for another five years, he thinks. Or perhaps even ten. But company policy is company policy. While clearing out his desk, a number of thoughts are going through his mind.

First, he notes that his firm’s retirement policy is not unusual. Nearly 90% of Japanese firms have mandatory retirement ages of 60 for most employees. Yet the Japanese are amongst the healthiest, longest-lived, economically productive people on earth and could in most cases remain at work through their 60s. Many of his friends are just like him: They would enjoy a few more years at work, if perhaps part-time in some cases, or with slightly more vacation time. He is also aware that the government has been encouraging firms to raise their mandatory retirement ages to 65, given an apparent desire by many older Japanese to continue working for longer. In this context, he finds it odd that 60 remains the standard retirement age in Japan.

Second, he thinks about his savings and pension and how these will finance his retirement needs. Like many Japanese workers, Mr Mizuno has worked his entire adult life for a single firm, although that firm has expanded and changed greatly during his time there. He has accumulated a substantial pension, which will provide him a steady if modest retirement income, enough to remain comfortable within his current lifestyle. The mortgage on his home was recently paid off, as he always planned to do prior to retirement. He has also saved some additional funds through the years, most of which has been conservatively invested in bank deposits and savings certificates and, as such, has more or less retained its value to the present day. To be sure, Mr Mizuno (and his wife) are most probably going to run through the bulk of this extra savings over the coming 20 years but, even in the event that they live somewhat longer, the pension will nevertheless cover their basic living costs indefinitely. (Incidentally, Mr Mizuno’s company pension is fully-funded in primarily low-risk investments so there is minimal risk that, for some unforeseen reason, his pension plan might become insolvent or be restructured in some way, reducing his income.)

Third, he thinks about his family. He and his wife have two children who are now middle-aged, employed and, with the exception of the 30-year mortgages on their homes, free of debt. They have one child each of their own, both of whom attend their local, traditional public school. Mr Mizuno loves watching his grandchildren growing up and is looking forward to spending more time with them following retirement, one of the positives of leaving work.

Reflecting on these things, Mr Mizuno knows he has much for which to be thankful. His parents had a rougher go in life, suffering as they did as young people during the war and aftermath. For years they worked six-day weeks for wages that, at times, barely put enough food on the table. Sure, things began to improve rapidly in the 1960s, when Mr Mizuno was old just enough to understand. They continued to improve through the 1980s and even in the 1990s, the decade in which both of his parents died. But Mr Mizuno was taught by his parents’ experience to be thankful for having missed a few rough decades.

As he places his last few belongings into a small box–including a picture of him being congratulated by the company’s former president at a team outing, in which he had scored the highest collective points total in the various competitions–a few concerns do enter his mind. For one, he read last week in the papers that the Finance Minister is pushing for another rise in sales tax to shore up government finances, which have been gradually deteriorating for years. Sure, Mr Mizuno and his fellow Japanese have long been accustomed to reading about government deficits, which have been chronic amidst efforts to stimulate the economy. But there seems a new sense of urgency for some reason, perhaps because the government’s total debt burden is now so high. Mr Mizuno has read some articles in the press suggesting that the debt is now too large to ever pay back. This thought sort of worries Mr Mizuno but he has difficultly understanding why the debt would ever need to be paid back. After all, it is he and his fellow citizens (and his pension fund) which owns the vast bulk of this debt, which pays a low rate of interest. Admittedly he is not in a position to buy up any more of the debt, given that he is now retiring. So perhaps this is why the government wants to raise sales taxes, to stabilise the public debt at the current level? Maybe that’s it.

Finally, Mr Mizuno, even though he has only rarely travelled abroad–including a bargain family vacation to Hawaii and California when the yen/dollar exchange rate was below 90 in 1995–has some concerns about the world at large. As with essentially all his classmates, he grew up with tremendous awe of and respect for the United States. In history classes he learned of how the British and other Europeans had established trading routes and colonies all over the world, including Japan, before the US even came into formal existence. Japan was late to the industrial game, although it had mostly played it rather well. But now with the US, UK and much of the euro-area economy suffering in the wake of a massive credit crisis, how might this affect modern, prosperous Japan? His lifelong employer produces precision tools largely for export all over the world. In recent years, somewhat more of these exports have started going to China and elsewhere in Asia, but many still go to the US and Europe. If those regions are now going to be growing more slowly in future, how might this impact the business going forward? The colleagues he is about to leave behind might need to deal with that.

After Mr Mizuno finished packing his final box he walked out of his office and down the corridor to that of his successor, who bowed when he saw him and then smiled. It was now his turn to have the office with the fine view out over the factory floor, where he had worked for much of his previous 20 years at the company. As Mr Mizuno was leaving the building for the last time as an employee, his successor walked into his new office and went straight up to the window, surveying the activity below. He had a few ideas about things he might change but, for the most part, he was content to oversee such a fine, well-oiled machine in action.

***

Regular readers of the Amphora Report will not be surprised by the narrative style employed above. We sometimes find it easier to communicate important ideas in this way as it avoids the need to rely entirely on economic equations and jargon. But the topic of what is happening in Japan, and what it implies for the rest of the world, nevertheless deserves some direct analysis.

Japan in an immensely wealthy country with an equally immense demographic problem. Think of Mr Mizuno. He’s a member of the vast Japanese middle-class. He is retiring and expects a modestly lower income in future as a result. But like his fellow middle-class retirees, growing rapidly in number, at least he has saved for retirement. Retiring is only a potential problem if you haven’t saved for it.

Wait a minute, some might interject, doesn’t Japan have a massive government debt? Well yes, as a matter of fact it does. Beginning in the early 1990s, following the collapse of a colossal housing and stock market bubble, Japan began to run large government deficits. It has remained in deficit ever since. The gross government debt/GDP ratio has thus risen relentlessly and is around 200% today. Ouch! (Net debt/GDP, incidentally, is much lower, at about 100%. More on that below.)

How rapidly is this debt growing? Well, according to the IMF, Japan ran a deficit of about 9.6% in 2010, slightly below the 10.2% and 11.1% deficits in the US and UK last year, although this is at a slightly higher rate than in the euro-area. Perhaps a better way to think about Japan’s government deficit and debt servicing costs is to look at what economists and sovereign debt analysts call the cyclically-adjusted primary balance (CAPB), which is the deficit adjusted for the business cycle, minus interest payments. As such it can be thought of as a longer-term “core” measure of the deficit. If the CAPB is positive, then this implies that your debt servicing costs are trending down rather than rising. Also according to the IMF, Japan is currently running a CAPB of 6.2%, slightly lower than that of the US, at 6.5%, although slightly higher than the UK, at 5.4%. (The euro-area looks somewhat better on this measure.) So while Japan’s public debt situation is serious and growing, it is at least not growing more rapidly than either the US or UK. And in the former case, a great deal of new stimulus has just been thrown at the economy in the form of tax cut and unemployment deficit extensions, which practically ensure an elevated US deficit over the coming year or two.

Yes, as it stands now, Japan’s government debt/GDP ratio is more than double those of the US, UK and most of the euro-area, for example. But let’s put this in perspective: First of all, who owns this debt? Well guess what, the Japanese do. That’s right, their government debt is held almost entirely domestically. They basically owe their public debt to themselves. Now that doesn’t mean that this debt isn’t an issue, but it’s not the same sort of issue as if your government debt is held largely by foreigners, who might decide to sell that debt someday to buy some other country’s debt or to finance domestic investment or consumption. This is a potential risk with the US, which relies on foreigners to finance a substantial portion of its government debt.

Having discussed government finances, this brings us to the most important point of all, which is to compare the entire Japanese economy, public and private, to those of the West. As a legacy of decades of large trade and current-account surpluses with the rest of the world, Japan has a cumulative net foreign credit position of some 57% of GDP, whereas the US and UK have net foreign debt positions of around 19% and 22%, respectively, with the euro-area roughly in balance. (1) This is reflected in part in Japan’s large official foreign exchange reserves of just over $1tn, the bulk of which are held in the form of US Treasury securities. (The US and UK have essentially no foreign exchange reserves. The euro-area has some $200bn.) Now, why are these figures so important? Think about it: If you are approaching retirement, do you want to owe other people money, or do you want them to owe you? Japan may be an ageing society but it is an ageing society with a private sector that has saved prudently for retirement! Japan may have a huge government debt but it can service that debt for an extended period by gradually winding down its massive net foreign credit position.

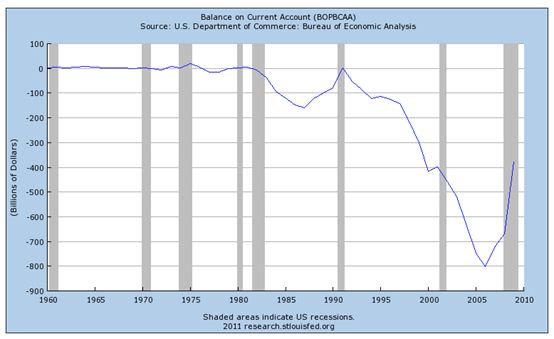

The US has been borrowing money from abroad for a generation

But wait, what does this imply? If Japan is now beginning to gradually “dis-save” in this manner, gradually selling off its large accumulated holdings of foreign assets to service its domestic debts, what is going to happen to interest rates and currencies? Well, if Japan is winding down its holdings of US Treasuries and exchanging the proceeds for yen cash to service Japanese government debt then, other factors equal, US Treasury yields are going to rise and the dollar fall versus the yen. Rising yields will crimp US growth and a weaker dollar will reduce US purchasing power, such that demand for Japanese exports will likely decline. But then, if Japan is indeed dis-saving, it will be less reliant on exports, especially to the US, which in any case is declining in importance for Japan as its Asian neighbours are growing much faster.

Viewed in this way, Japan’s demographic issues, far from being automatically yen negative, could in fact be yen positive, at least for a period of some time. Yes, Japan’s potential growth rate may be in gradual decline for demographic reasons, but at least they have a huge stock of private savings. And as they wind down their holdings of foreign assets, stocks and bonds, and exchange the proceeds for yen, the value of those assets will come under downward pressure, as will their currencies of issue versus the yen.

One objection that might be raised at this point is that perhaps, notwithstanding a large net foreign credit position, Japan’s private sector has nevertheless not saved enough to fully fund its demographic-driven future liabilities. Fair enough, in fact we would agree that it hasn’t. But please answer this: Who has? Please name one large developed country that has fully-funded future liabilities, public and private. Can’t do it? Well that’s because there isn’t one! (There are some smaller ones, including Norway for example.) The US, with estimated future public liabilities of some five times GDP may be the most egregious example of massive, largely unreported off-balance sheet obligations such as medicare, social security, etc, but it is nevertheless in good company with the UK and several euro-area countries.

Moreover, whereas Japanese corporations and also the public sector tend to have essentially fully-funded pension plans–the primary explanation for why Japan’s net public debt is so much lower than gross public debt–the same cannot be said for most US, UK or European corporations and public sector entities, many of which are already facing pension funding problems, requiring additional debt issuance just to make interest payments! Now how on earth is that new debt going to be serviced? We’d much rather be in line to receive a fully-funded Japanese pension–despite the demographics–than a ponzi-style pay-as-you-go and hope-the-stock-market-always-rises western-style one!

Another point that is worth mentioning here is that, as mentioned in our narrative above, the normal Japanese retirement age is only 60, yet the Japanese are generally much healthier and longer-lived than their western counterparts, and also tend to have a stronger work ethic, implying that it could be quite possible to extend the retirement age substantially, thereby generating additional income and holding down retirement costs. That could have a huge impact on their ability to deal with their demographic problem, at least for a number of years. Certain western countries have large and growing health issues which suggest that, even if retirement ages are extended somewhat, they may not be able to reap the same degree of productivity benefits as Japan.

Finally, much ridicule has been directed at Japan’s relentless and ultimately futile attempts at fiscal stimulus over the past two decades. But consider: Rather than transfer cash to households to spend on food, or vacations, or whatever, stimulus in Japan has generally taken the form of investment in infrastructure, such as “bridges to nowhere”, for example. Now we are no fans of misguided Keynesian stimulus, which at the extreme is as counterproductive as paying people to dig holes and then fill them up again, but if we had to, we would probably choose to own a bridge to nowhere or other such infrastructure rather than an empty hole in the ground. The former might at least be of some value, if less than what a profit-seeking corporation would have built with the capital instead. If Japan does get into budget difficulties down the road that cannot be fully addressed by increasing the retirement age; raising taxes; restructuring pension liabilities; drawing down net foreign savings, etc, then Japan has much public infrastructure which could be privatised to raise funds. After all, this has been going on in western economies for years. So much public infrastructure has already been sold off in some places that there is not much left. In the US, even state capitol buildings have been sold (and leased back) to raise revenue for cash-strapped governments! Japan has not even begun to go down this road, which given the huge numbers of “bridges to nowhere”, might be long indeed. The West, however, has mostly reached the end, leaving it with fewer options.

***

We all know what happens to countries that have borrowed too much and can’t pay it back. They devalue their currencies, default on their obligations, or both. However, if you owe the debt largely to foreign, rather than domestic investors, isn’t it politically somewhat more expedient to devalue, than to default? As a result, might the political temptation to devalue unfunded liabilities away be much greater in the US than in Japan? We believe so. Perhaps someday there is going to be some sort of restructuring of Japanese government debt, but as they owe it primarily to themselves and are only now just beginning the long process of dis-saving, which implies less reliance on exports, we don’t see nearly as much potential risk of a pro-active devaluation of the yen as we do for, say, the dollar or sterling, where savings rates and exports, in fact, need to rise dramatically to rebalance those economies. It is not just the economics of foreign asset sales that favour the yen over the dollar but, at the margin, also the politics.

We do sympathise with the Mr Mizuno of our narrative above. He is perfectly justified in having some serious concerns about the future of his country. But it is the now-retiring baby boomers of the West who, in our minds, have reason to be outright terrified.

The Amphora Liquid Value Index (through 11 January 2011)

Source: Bloomberg LP

Resources:

(1) It is an economic identity that, as you export more than you import, you run a trade surplus which, when broadened to include all cross-border transactions, including interest payments for example, is called a current-account surplus. Over long periods of time, cumulative current-account surpluses, or deficits, can become large and, in the past, have occasionally been associated with major international financial crises. This is one reason why many observers have been concerned in recent years with the growth of global imbalances, in particular that of the US, which has been running large deficits, and China, which has been running large surpluses. In key respects, the current set of global imbalances is eerily reminiscent of the 1920s, when the US was running large surpluses and the UK large deficits, a legacy of massive WWI spending and economic upheaval. While economic historians disagree on the specifics, there is general agreement that the large and growing global imbalances in the 1920s contributed to the severity of the Great Depression that began during the global financial crisis of 1929-33.

THE AMPHORA LIQUID VALUE INDEX represents the return on a dynamically-rebalanced portfolio of broadly and efficiently diversified commodities and currencies, intended to retain its real value in a wide variety of circumstances, including both inflation and deflation.

AMPHORA: A tall, lateral-handled, ceramic vase used for the storage and intermodal transport of various liquid and dry commodities in the ancient Mediterranean.

AMPHORA CAPITAL is dedicated to helping clients preserve wealth in a highly uncertain global environment by developing investment strategies protecting against both inflation and deflation.

John Butlerjbutler @ jb-cap.com

John Butler has 17 years experience in the global financial industry, having worked for European and US investment banks in London, New York and Germany. Prior to founding Amphora Capital he was Managing Director and Head of the Index Strategies Group at Deutsche Bank in London, where he was responsible for the development and marketing of proprietary, quantitative strategies. Prior to joining DB in 2007, John was Managing Director and Head of Interest Rate Strategy at Lehman Brothers in London, where he and his team were voted #1 in the Institutional Investor research survey. He is an occasional contributor to various financial publications and websites.

DISCLAIMER: The information, tools and material presented herein are provided for informational purposes only and are not to be used or considered as an offer or a solicitation to sell or an offer or solicitation to buy or subscribe for securities, investment products or other financial instruments. All express or implied warranties or representations are excluded to the fullest extent permissible by law. Nothing in this report shall be deemed to constitute financial or other professional advice in any way, and under no circumstances shall we be liable for any direct or indirect losses, costs or expenses nor for any loss of profit that results from the content of this report or any material in it or website links or references embedded within it. This report is produced by us in the United Kingdom and we make no representation that any material contained in this report is appropriate for any other jurisdiction. These terms are governed by the laws of England and Wales and you agree that the English courts shall have exclusive jurisdiction in any dispute.

© Amphora Capital LLP. All rights reserved. Amphora Capital is registered in England and Wales under the number OC345497.