One to the biggest issues that face millions of retiring individuals in the coming years is the grossly underfunded pensions for state workers nationwide. Just recently the PEW Center For The States released their annual update on the status of state pension plans - the bottom line is not good. "States continue to lose ground in their efforts to cover the long-term costs of their employees' pensions and retiree health care, according to a new analysis by the Pew Center on the States, due to continued investment losses from the financial crisis of 2008 and states' inability to set aside enough each year to adequately fund their retirement promises. States have responded with an unprecedented number of reforms that, with strong investment gains, may improve the funding situation they face going forward, but continued fiscal discipline and additional reforms will be needed to put states back on a firm footing."The report, which is based on fiscal year 2010 data which is that latest complete data set available, the gap between states’ assets and their obligations for public sector retirement benefits was $1.38 trillion, up nearly 9 percent from the fiscal year 2009. Of that figure, $757 billion was for pension promises, and $627 billion was for retiree health care.

The problem, however, is not a current development the recent financial crisis but goes back over a decade when pension managers began making aggressive return assumptions of 8% - the same as it is today. With higher return estimations the states were required to fund less into pension plans leaving money available for all sorts of other spending. What they did not account for, however, was over a decade of near zero return growth, two nasty bear markets which decimated investment accounts, two recessions which lowered tax revenue and a weaker growth economy. PEW stated: "Investment losses suffered by pension funds during the Great Recession have been a key driver of growth in states’ unfunded liabilities. About $6 of every $10 in the funds comes from earnings on investments; employee and employer contributions make up the rest."

While the majority of pension plans were projecting gains of 8% in 2008 the median loss turned out to be 25% with many performing far worse. While the market has rebounded in the past three fiscal years - the hole left by the massive draw down in 2008, combined with the continued expected return of 8% and underfunding, have increased the gap to the $757 billion where it sits today. Considering the S&P 500 returned just shy of zero in 2012 the gap will be worse in the next report.

As states struggle with budgetary problems, lower revenue and low market returns - the level of funding obligations continue to impact the health of pension plans nationwide. According to PEW: "Many experts say that a healthy pension system should be at least 80 percent funded. In 2000, more than half of the states were 100 percent funded, but by 2010 only Wisconsin was fully funded, and 34 were below the 80 percent threshold—up from 31 in 2009 and just 22 in 2008. Connecticut, Illinois, Kentucky, and Rhode Island ranked the worst; all were under 55 percent funded in 2010. At the other end of the spectrum, four states were funded at 95 percent or better: North Carolina, South Dakota, Washington, and Wisconsin."

However, even 10-20% underfunding could create problems depending on many variables such as another recession, stock market swoon or how many individuals step into retirement. In order to shore up funding shortfalls in recent years many pension plans have turned to alternative investments such as hedge funds and private equity. Unfortunately, those investments, in many cases, have lagged well behind the markets over the last couple of years which has further compounded the problem. Pension funds are finally beginning to slowly lower the 8% return assumptions but therein lays another problem. As pension plans reduce their estimated returns the level of required funding goes up. That funding must come from the State's budgets which are sorely short of funds to begin with.

Many states have begun to take action by either reducing pension benefits or increasing employee contributions over the last three years. These have been very minor changes and many states have already acknowledged that any reforms already made will not be sufficient to control rising long-term retirement costs or reduce the risk of future underfunding. PEW stated: "Though states have enough cash to cover retiree benefits in the short term, many of them—even with strong market returns—will not be able to keep up in the long term without some combination of higher contributions from taxpayers and employees, deep benefit cuts, and, in some cases, changes in how retirement plans are structured and benefits are distributed"

This does not bode well for many of those workers today that have already under saved for retirement and are counting on those benefits to fund both retirement and healthcare needs in the future. For many pension plans it has been the equivalent of being in the ring Mike Tyson - they keep getting knocked down no matter which way they turn. It is a frustrating problem with severe consequences to retiree's as millions of Americans are at risk in future years.

Of course, all this coincides with a massive number of individuals beginning to move closer to retirement. The timing could not be worse and the problems do not stop there.

Health Care Looks Even Worse

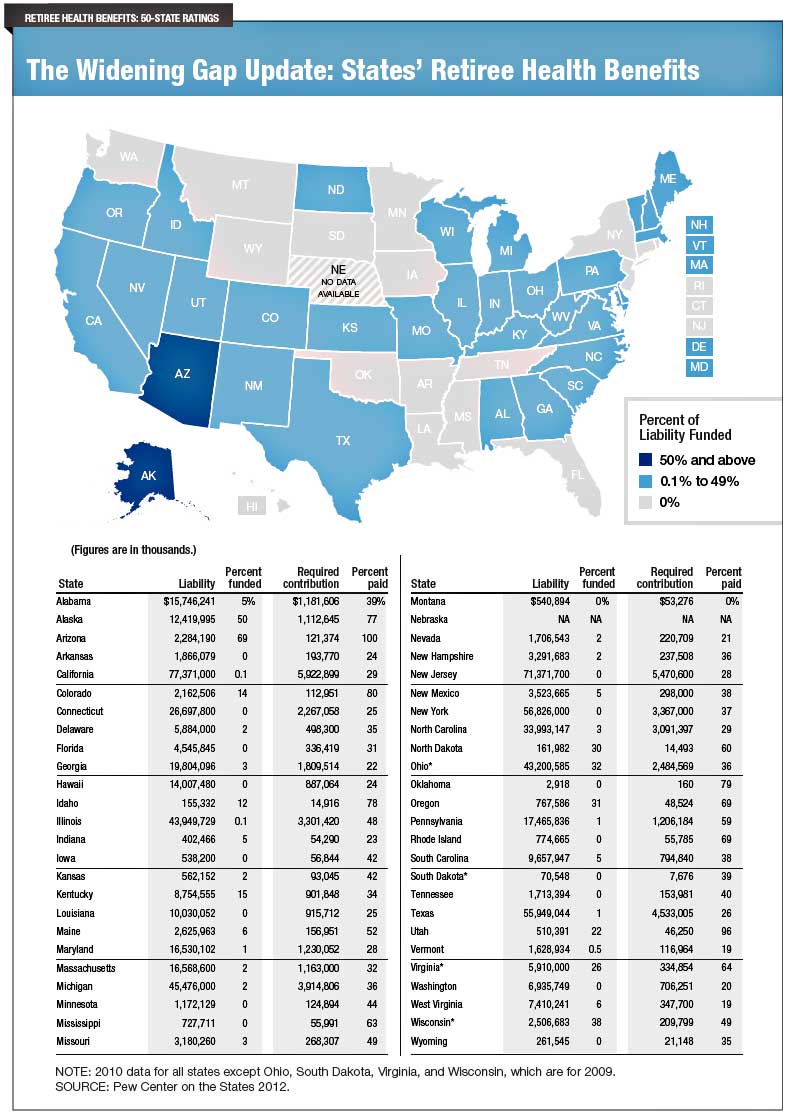

On top of the problem with the state's retirement plans - retirees’ health care and other non-pension benefits such as life insurance are even in worse shape. As of fiscal year 2010 - States had put away only 5 percent of their total bill coming due for those benefits. According to PEW: "Seventeen states set aside no money, and only seven states had funded at least 25 percent of this long-term liability. In contrast, Alaska and Arizona had nearly 50 percent of their health care liabilities covered by assets on hand. No other states came close to that percentage.

Many states have not held up their end of the bargain when they should have been paying for the promises they made. All told, state and local governments participating in state-run retirement systems should have set aside 4 billion in fiscal year 2010 to pay the recommended contribution for their pension and retiree health care obligations. Policy makers were able to make 78 percent of the recommended contribution toward their states’ pension plans but set aside just 34 percent of what actuaries recommend should be set aside to pay for retiree health benefits.

While it is currently difficult for states to make contributions toward their retirement systems, given the drop in revenues and fiscal stress from the recession, many of these states also failed to make the recommended contributions when times were good."

The liability in 2010 was $660 billion but states only had assets to cover $33.1 billion leaving a $627 billion deficit. Again it comes down to the problems with the state's budgets and priorities. For years now the state's have lived well beyond their means spending money on everything but their promised obligations in many cases. In 2010, as unfunded health care liabilities rose by $22 billion - only seven states fund 25% or more of their retiree health care obligations: Alaska, Arizona, North Dakota, Ohio, Oregon, Virginia, and Wisconsin.

According to PEW states overall should have set aside nearly $51 billion to pay for health care obligations in fiscal year 2010 but only contributed slightly more than $17 billion or about 34 percent of what was required for the year. While pension obligations are generally funded in advance these healthcare obligations are generally paid as the expense is incurred. This is a giant, and unrealized, vacuum waiting to occur in future years as masses of retirees begin to incur enormous healthcare costs simultaneously. With the massive shortfall of funding in health care plans today - there is no cushion for a surge in incurred costs in the future.

State's nationwide have now come to the realization of the problems that lay ahead and are beginning to slowly take action in reforming their structures. However, the assumptions continue to be flawed as there is no accounting for further recessions, market draw downs, or other events that cause deterioration in the underlying assets or revenue streams. In fact, projections for economic and market growth in a sustained low interest rate environment may turn out to be very shortsighted.

At some point in the future state retiree's will begin to be impacted as pensions reach the limits of their solvency and more radical measures are taken to shore up liabilities with reality. With the majority of American's under saved for retirement, incomes stagnant and savings on the decline - the dependency on retirement plans is higher than ever. That dependency will likely prove to be a mistake.

Source: Street Talk Live