When it comes to anticipating Federal Reserve policy, there’s no better place to turn than former Fed Chair Ben Bernanke. No longer bound by an office, Mr. Bernanke is now free to write about monetary policy as an outsider.

In a recent two-part post, the former Fed Chair took some time to explain what tools the Fed has left, and where they might turn in the case of another economic downturn. Why is this important? Because many believe the Fed’s hands are now tied as a result of short-term rates being near zero, and the Fed’s balance sheet sitting at over $4 trillion.

So if the economy continues to decelerate, what is the Fed’s next move?

According to Bernanke, there are some logical first steps, followed by uncertainty regarding the use of extraordinary measures such as negative interest rates and long-term rate targeting.

The conventional policy response would likely entail three parts:

First, the Federal Reserve would communicate to markets change in policy direction by eliminating the expectation for further rate hikes. This, by itself, would act as a form of stimulus as it would reduce upward pressure on the yield curve and reset investor expectations.

Read Gordon Long: If You Think QE Was an Experiment, You Haven't Seen Anything Yet!

The next logical step would be to reduce the target federal funds rate back to the zero to quarter point range it sat at for years until the most recent rate hike.

The third step would involve the reintroduction of forward guidance, using “open-mouth operations” to talk down longer-term interest rates.

The Fed used all three of these measures to combat the financial crisis, and they weren’t enough. As a result, the Fed had to resort to unconventional monetary policy in the form of quantitative easing.

It’s likely that in the event of another major downturn, these measures would not be enough stimulus to change course. Consider Bernanke’s comparison in which he notes that during the last two recessions, the Fed had to cut rates by 5.5 percentage points and 5.1 percentage points, respectively.

This makes a quarter point rate cut seem like child’s play.

So far, in his ongoing blog posts, Bernanke has addressed two other possible alternatives the central bank could turn to: negative interest rates and long-term rate targeting.

I found his comments on both rather intriguing, and will do my best to summarize them here.

Regarding negative interest rates, Bernanke points out that this concept is not necessarily novel. In reality, we’ve dealt with negative interest rates plenty of times throughout history in the form of negative real rates. He uses the chart below as evidence.

Interestingly, although the nominal federal funds rate has held at zero since 2008, the real federal funds rate has been negative for nearly that entire time. And it’s gone negative many times over the last few decades.

So if we’ve already had a negative real federal funds rate, what’s the big deal in taking the nominal rate below zero?

Bernanke argues that this is a feasible approach, with a few operational and legal constraints. I’m going to ignore the legal constraints for now, as it seems that dire economic situations tend to open the door for changes in the Fed’s legal authority (as they did during the financial crisis).

The primary operational constraint cited by Mr. Bernanke involves how negative the federal funds rate could go to the market as a whole begins to hoard cash.

Read also Russell Napier Forecasts Negative Rates in the US as Deflationary Pressures Spread

Recall that in a deflationary environment; cash becomes your best friend. It’s the one thing that tends to hold its value. In a strangely paradoxical way, negative interest rates can bring about that same behavior, which can ultimately cause a reduction in economic activity.

Bernanke notes a previous 2010 FOMC memo, in which Fed staff concluded that the limit to negative rates (due to this hoarding effect) was likely near -0.35 percent. Recently, several countries have blown past this mark with what appears to be a little adverse response, suggesting, as Bernanke puts it, that, “… the negative rates tool might be more powerful than thought.” To be fair, he goes on to state that he believes rates in the US could not go much beyond that mark without causing significant disruptions to some financial markets and institutions.

Regarding effectiveness, Bernanke paints much the same picture as another analysis has concluded, that rate cuts below zero have a similar effect to rate cuts above zero, making them a possibly relevant tool moving forward.

The other alternative that Bernanke suggests the central bank could employ during a sustained economic downturn is something that we’ve seen before long-term rate targeting.

As I’ve frequently discussed in the past, long-term rates are more influential to the macro economy than short rates. Historically, the Fed has targeted short rates as a means to influence longer-term rates, but recently (with the advent of QE) they’ve gone directly after long-term rates.

In reality, quantitative easing is a form of rate targeting, but it’s a more indirect approach. With quantitative easing, the Fed decides what quantity of assets they want to purchase to reduce supply in the market, driving bond prices up and yields down. In this case, the known variable is the quantity of assets they will purchase, and the unknown is what magnitude of suppression effect this will have on rates.

With rate-targeting, the Fed would set the desired price (and thus yield) at which they would purchase bonds, and allow the quantity of assets they would need to purchase to fluctuate, based on market conditions and expectations. In this scenario, the known variable is the final interest rate, but the unknown is what quantity of assets will be needed to achieve that rate.

Check out Global Liquidity Falls to 2008 Crisis Levels

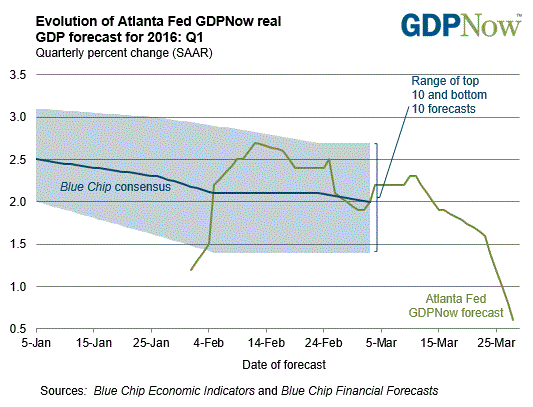

Then there’s this: The most recent Atlanta Fed GDP Now estimate showing the trajectory of Q1 GDP heading lower and lower.

Bernanke points out that the US already used this approach during WWII and in the following postwar years. During that time, the Fed pegged the interest rate of T-bills at 3/8 percent and created a 2.5% ceiling on long-term Treasury debt.

The main problem with this approach, as opposed to quantitative easing, is that it leaves a big question mark regarding the quantity of assets the Fed would have to purchase to maintain the peg. Bernanke notes that this concept, which he terms “losing control of the balance sheet,” was a factor in choosing QE over rate-targeting while he was Chairman.

Nonetheless, it’s possible that rate-targeting could have a pronounced effect without forcing significant expansion of the balance sheet, in which case it would be a strong alternative to QE.

No matter where the economy heads from here, it seems evident that we will not cross back into the realm of conventional monetary policy anytime soon. If that’s the case, we all need to become more educated about how various monetary policy scenarios may impact our economy and the value of our assets.

The preceding content was an excerpt from Dow Theory Letters. To receive their daily updates and research, click here to subscribe.