Spanish House Prices Plunge Again

It is well known that Spain's economy is in a depression, and we do not use this term lightly. With the official unemployment rate at about 23% and youth unemployment close to 50% it is not an exaggeration to speak of a depression. The probability of social upheaval erupting with greater frequency is extremely high. We already noted that the general strike recently called for by Spain's unions is only the fifth since the end of the Franco regime in 1975. It is a rare event in Spain and underscores the decline in the social mood and the growing desperation. Those who still have work want to protect their privileges and use the unemployed as their political weapon.

Meanwhile, Spain's banks are quietly sinking beneath the waves. They are the quintessential zombies, especially the insolvent cajas, which are drowning in real estate related assets that see the value of their collateral inexorably spiraling down the drain (as an aside here: the Fed's recent 'stress test' of US banks possibly has not taken sufficient account of this 'moving target problem'; as we have seen mentioned elsewhere, it also failed to consider the remote possibility that treasury bonds may decline more than it currently widely expected).

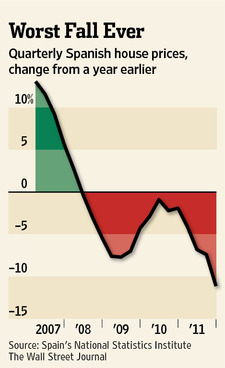

But let's return to Spain. The WSJ reports on the latest house price data, and keep in mind here that these are the 'official' and hence doctored in every imaginable way, data. The plunge in house prices is in fact accelerating.

“Spanish house prices tumbled at their fastest pace on record in the fourth quarter, a sign that a long-running property bust will continue to weigh on Spanish households and banks.

House prices fell on average by 11.2% in the fourth quarter from the same period a year earlier, well below the 7.4% decline in the third quarter, while prices of used homes was down 13.7% in the period, the country's statistics agency INE said Thursday.

Both readings are by far the worst since INE started recording countrywide prices in 2007, the peak year for Spain's decade-long property boom. Previously, annual price declines had bottomed out at 7.7% in 2009, and analysts say house prices have only rarely fallen year-to-year since at least the 1970s.

The drop indicates Spanish property prices are now correcting at a similar pace to that seen in the U.S. soon after the 2008 financial crisis, and may fall further at least this year. In previous quarters, price drops were somewhat contained, the result of support efforts by the government and banks, fearful of the effect of a housing collapse.

Spanish banks hold more than €400 billion ($521.32 billion) worth of loans to the construction and real-estate sector, backed by collateral that loses value as property prices slide further. The amount is equivalent to around 40% of Spain's gross domestic product.

(emphasis added)

Spain's house price decline according to official statistics: the worst fall ever.

Now, we can not stress enough here that the official data grievously understate the true state of affairs. They are however used by the banks as the basis for evaluating the collateral backing the real estate loans on their books.

It follows therefore that Spain's banking system continues to be even more rickety than is generally believed. The current 'Operation Spanish Ponzi', whereby the banks 'bail out' the government by buying Spanish government debt with funding from the ECB's LTRO's, while the two government-owned bank bail-out agencies are concurrently bailing out the banks, seems inevitably destined to fail. This scheme relies on the idea that the financial markets can be conned forever and ever. Now, it is certainly true that the markets can be conned for extended periods. Sadly, 'forever' is a mite too extended in this context.

Already the first cracks in this happy arrangement are beginning to show: a government bond auction on Thursday drew less demand than expected and the treasury sold less paper than it had planned (although yields remained fairly low by recent standards).

As to the future of house prices in Spain, the WSJ inter alia quotes a Spanish economist at Global Insight:

“Raj Badiani, an economist at IHS Global Insight, said government data indicates Spanish house prices are down more than 20% from the 2007-2008 peak, even though other evidence points to a possible drop of more than 30%. [actually, there is still other evidence indicating it's more like 40% to 50% by now, ed.]

"The continued imbalance between the supply and demand of housing suggests that house prices will continue to fall throughout 2012," Mr. Badiani said. "The outlook remains bleak, with the demand for housing expected to shrink throughout 2012 with debt-laden households struggling to cope with a devastated labor market and limited access to credit."

Last month, Spain's Finance Minister Luis de Guindos presented a clean-up plan that will force banks to set aside an additional €50 billion this year to cover losses from souring loans, mostly property-related. The plan also seeks to allow a faster correction of the property market this year, so that lower prices trigger some demand in the moribund sector.

Earlier this week, INE data showed Spain's property sales continued their recent slide in January, with a 26% annual decline. Last year, just over 361,000 homes were sold in Spain, less than half the number sold in 2007.

The clean-up plan and other reforms may only have a delayed effect on the euro zone's fourth-largest economy, the Ernst & Young consultancy said in a report. A lack of demand amid an economic contraction that may stretch until 2014 should keep house prices falling for the next three years, Ernst & Young added.”

(emphasis added)

Remember that only a year ago, the Bank of Spain insisted that Spain's banking system would need only € 20 billion in the 'worst case'. Now this amount has grown to € 50 billion, so it seems that something worse than the 'worst case' has happened. It is highly likely that this amount will still not be enough. Of course we are predicating this opinion on the notion that all over Europe, banks are considered too precious to be allowed to actually fail, with perhaps only the very smallest ones excepted form this rule.

Spain – Even Worse than Greece?

A few days ago, Sony Kapoor, managing director of the 'Re-define' think tank appeared on CNBC and pronounced Spain to be a 'worse case than Greece'.

Now,we're not sure if one can really go that far. After all, Spain at least sports a vibrant and fairly competitive export industry, although it is probably too small to matter in the current crisis. Still, it is interesting that there are quite a few people out there who do not think the LTRO inflation exercise has solved all problems in Europe.

This is in contrast to the official eurocrat line, which is of course that everything is copacetic again.

“Spain has very large downside risks and it needs to tread very carefully – Spain is in a very fragile situation. Its problems are significantly worse than Greece’s,” Sony Kapoor, managing director at international think tank Re-Define said.”

[…]

Wolfgang Schaeuble, German finance minister, speaking at the meeting dismissed any comparisons with Greece describing it as a “completely unique case” adding that Spain “had made great progress but we’re all still on a tough path.”

Ben May, European economist at Capital Economics, told CNBC.com that underlying issues in Spain could derail any attempts to curb the budget deficit.

“There are some reports that suggest that public debt might be higher than the official statistics show and there’s a concern that it might end up worryingly high over the next couple of years. The banking system is also fragile and the fact that there’s a housing overhang means we could see a situation like that in Ireland,” May told CNBC.com.

He added that talk of bailouts and defaults would then be ramped up but with far worse consequences than Greece.

“Spain is so much larger than Greece, so even if there is a small risk of a default or a bailout then it has much bigger implications for the euro zone than Greece had,” May added.

(emphasis added)

And that is actually the crucial point here: it is not so much the question whether Spain's situation is really 'worse than Greece's', which seems to be a slightly dubious proposition. It is the fact that a crisis in Spain matters a lot more to the future of the euro area than the crisis in Greece. The current consensus has it that 'Greece has been walled off', but consider how much angst and money this procedure has so far cost – and that is not even considering the fact that Greece may need yet another bailout or debt restructuring down the road.

The problem is that Spain is so much bigger – it is the quintessential 'too big to bail' case.

5 year CDS on Portugal, Italy, and Spain. It is noteworthy that both Portugal's and Spain's have begun to trend higher once again. Spain is now once again considered a worse credit risk than Italy, which is as it should be.

Spain's IBEX has been sitting out the recent rally in 'risk assets' across the world. It continues to be mired in a secular down trend - click for better resolution.

Charts by: StockCharts, Bloomberg, WSJ

Source: Acting Man