The Fed was cocked and primed to deliver a 25 basis point increase in the federal funds rate on June 15. But on June 3, the BLS announced that nonfarm payrolls increased a paltry 38,000 in May. This monthly random number prompted the Fed to stand down on its interest rate increase. Then on June 23, the UK voters surprised the smart money by voting to have the UK leave the EU. Globally, the prices of risk assets swooned for a couple of days. The FOMC was thanking its lucky stars that the May nonfarm payroll report caused it to hold off on its planned rate increase for June 15.

But my bet is that in the announcement immediately following the July 26-27 FOMC meeting, the Fed will put us on notice that an interest rate hike is on the agenda for the next FOMC meeting, September 20-21. One reason for my Fed policy expectation is that the pace of U.S. economic activity has picked up in recent months. June nonfarm payrolls rebounded by 287,000. Nominal retail sales surged at an annualized rate of 5.9% in the second quarter after having contracted 0.2% annualized in the first quarter. The manufacturing Purchasing Managers Index (PMI) increased in both May and June with the June level of 53.2 being the highest reading since February 2015. Corroborating the behavior of the manufacturing PMI was the 0.4% rebound in the Fed’s measure of manufacturing production for June. At 1.160 million units, average second quarter housing starts were the highest since Q4:2007. Too be sure, the U.S. economy is not hitting on all cylinders. “Compression” is low in business capital spending, in part due to the relatively low energy prices and previously weak consumer demand. Exports have weakened because of the slowdown in the pace of economic activity in developing economies. But about 80% of the economy is doing reasonably well.

See also A June Fed Funds Rate Hike Risks a September Economic Stall

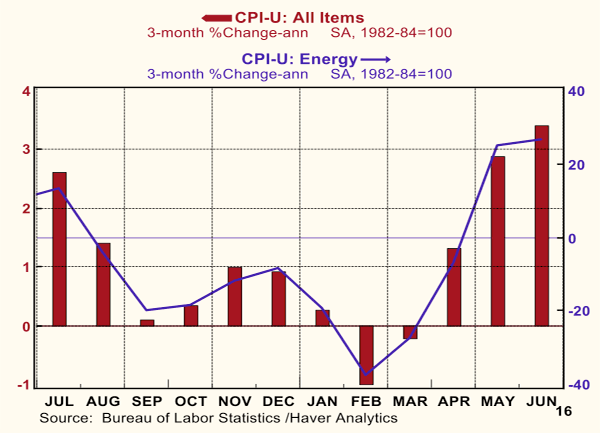

Does the current inflationary environment cry out for a Fed interest rate increase? After all, growth in the Consumer Price Index (with all components accounted for) has accelerated to an annualized rate of 3.4% in the three months ended June (see Chart 1). But data in Chart 1 also suggest that both the prior deceleration as well as the recent acceleration in CPI growth has been influenced by changes in energy prices.

Chart 1

Although energy prices account for only a little bit over 7% of the CPI, in the past 12 months, the median annualized month-to-month absolute-value percentage change in the energy component of the CPI has been almost 18%. Perhaps energy prices will continue to rise without other prices falling, thus resulting in a still higher rate of CPI inflation. Alternatively, perhaps energy prices will stabilize or even fall, which, depending on the behavior of other CPI components, could result in a decrease in CPI inflation. Perhaps some other CPI component will exhibit large month-to-month price volatility, which translates into extreme CPI inflation volatility. Whether it is a big movement in energy prices this month or some other component next month, there is a lot of “noise” or volatility in the short-term behavior of the CPI when all items are included. This makes the Fed’s policy decisions and our investment decisions more difficult.

One way to moderate some of the noise in the CPI is to exclude some components that historically have been volatile, such as energy and food prices. This is part of the logic for looking at the so-called “core” CPI – i.e., the CPI excluding its food and energy components. But food prices and/or energy prices are not volatile every month. So, to automatically exclude these components from the CPI each month is arbitrary. A better way would be to “smooth” the short-term behavior of the CPI would be to exclude items that actually are volatile in a given month rather than arbitrarily picking one or two items that have demonstrated price volatility in the past. This is what the Cleveland Fed does by calculating each month something it calls the 16% trimmed mean CPI. Essentially what the Cleveland Fed research team does each month is trim, or eliminate, 8% of the weighted CPI components with the largest monthly percentage increases and 8% of the weighted CPI components with the smallest monthly percentage increases from the remaining CPI components. Then, a weighted mean, or average, CPI is calculated using the 84% of the least volatile CPI components for that particular month. Energy prices are not automatically excluded from a particular month’s CPI calculation. But if the percentage change in energy prices in a given month is extreme compared to percentages changes in other CPI components, then they will be excluded.

Chart 2 shows the month-to-month annualized percentage change in the Cleveland Fed 16% trimmed-mean CPI and the All-Items CPI. Not surprisingly, the month-to-month behavior of the trimmed CPI has exhibited less volatility than that of the All-Items CPI.

Chart 2

The Fed has hinted that its target for annualized consumer inflation is around 2%. The median month-to-month annualized growth in the Cleveland Fed 16% Trimmed-Mean CPI in the past 12 months has been – you guessed it – 2%. Chauncey Gardiner predicted that the economy would grow in the spring, and it has. The Fed has “achieved” its target consumer inflation rate. Why not signal at the July 26-27 FOMC meeting that a federal funds rate increase is penciled in for the September 20-21 FOMC meeting barring extenuating circumstances?

Is it likely that the pace of U.S. economic activity will slump significantly between now and September 21? Not if the behavior of “thin-air” credit has anything to do with it. (Everyone may imbibe now.) Chart 3 shows that growth in the sum of commercial bank credit and the monetary base (currency in circulation and depository institution reserves at the Fed) has grown at an annualized rate of 4.8% in the three months ended June. Although 4.8% is not a blistering pace in an historical context, it does represent a rebound from its growth slump in December-to-February period. The winter growth slump in thin-air credit resulted from the Fed’s December federal funds rate increase. In order to bring about this rate increase, the Fed had to reduce bank reserves relative to their demand. This caused a corresponding slump in the monetary base component of thin-air credit. As also can be seen in Chart 3, growth in the commercial bank component of thin-air credit actually accelerated after the Fed raised the federal funds rate in December.

Chart 3

In sum, I believe that in the policy statement of the July 26-27 FOMC meeting, the Fed will alert us to the high probability of a 25 basis point increase in the federal funds rate occurring at the September 20-21 FOMC meeting. In the event, I believe that this will cause a significant upward revision in market expectations of the level of future short-term interest rates. Because yields on longer-maturity securities are a function of expected future yields on short-maturity securities, bond yields also will rise. Although history might not repeat itself, it does tend to rhyme. Go back and review what happened to the bond market in 1994.