Opinion is currently divided on the world's second largest economy.

On one hand of the spectrum, the bears believe that China is a train-wreck and that its economic growth is unsustainable. These sceptics love to highlight the property bubble in China and they never miss the opportunity to mention the fact that fixed asset investment accounts for a disproportionately large chunk of the Chinese economy. According to the bearish camp, China's economy is not real; rather, its breakneck economic growth is centrally planned by Beijing. Furthermore, the bears argue that China's vast foreign exchange reserves are meaningless and that they will be used up in dealing with the aftermath of the Chinese real estate bust.

On the other side of the equation, the optimists believe that China is the next great nation in the world and its super power status is all but assured. These bulls point to China's foreign exchange reserves, low debt levels, high savings rate, strong work ethic and growing domestic consumption. According to these folk, China's economy is amongst the strongest in the world and Beijing is in total control.

So, given such conflicting views, it is hardly surprising that investors are confused about China. Furthermore, it goes without saying that over the past few months, we have spent a lot of time thinking about China's prospects. Therefore, we will now outline our views about the Chinese economy and its financial markets.

First and foremost, we want to make it clear that we are not bearish about the long-term prospects of the Chinese economy. After all, the country has amassed the largest foreign exchange reserves in the world (US$2.85 trillion), it boasts a very high savings rate (37%), its household debt to GDP ratio is very low and its per-capita income is rising rapidly. Therefore, at first glance, the Chinese economy appears to be in good health.

Unfortunately, China's economy also has a soft underbelly; it's out of control property market. After reviewing heaps of data, it is clear to us that real-estate prices along the coastal cities in China are grossly over inflated and due for an abrupt adjustment. When measured in terms of affordability (median home price to median household income), it is blatantly obvious that Chinese property is in a gigantic asset bubble. Moreover, various other data points also confirm overvaluation and excesses in China's property market.

According to some reports, billions of square feet of commercial real-estate is unoccupied in China. Furthermore, we have also heard accounts from reliable sources that there is rampant speculation in China's residential real-estate. For example, the Chinese have been snapping up bare-shell apartments (no internal walls or fittings), for the sole purpose of flipping these properties for a quick profit. It is interesting to note that these buyers are not the least bit interested in a rental yield, their only intention is to sell these properties to a 'greater fool'.

Needless to say, China's banks have been doing their part to fuel this speculative orgy. For instance, the South China Morning Post recently reported that in 2010, China's banks originated CNY8 trillion in new 'official' loans and this amount exceeded Beijing's loan target. However, the buck did not stop here and allegedly the Chinese banks loaned out an additional CNY3 trillion via 'off the balance-sheet' arrangements orchestrated through various Trust entities.

Figure 1 captures the sharp increase in China's Yuan-denominated loans. According to China Daily, outstanding Yuan-denominated loans stood at CNY47 trillion at the end of October, which is an astronomical sum when you consider that China's economy is worth only CNY37 trillion. Unfortunately, this rampant credit growth is not slowing down and apparently, Chinese banks have already created new loans worth CNY1.5 trillion in 2011!

Figure 1:

China's new Yuan-denominated loans (October 2009-October 2010)

Source: China Daily

So, there you have it. All the conditions are now in place for a property bust – extreme overvaluation, abundant credit and massive oversupply. The trillion dollar question though is whether the unavoidable bust in housing will impact China's broader economy or will the damage be confined amongst the property speculators and developers?

Unfortunately, this is a very difficult question to answer but given the relatively low household debt in China, we are inclined to believe that the pain will be limited to the property developers, leveraged speculators and banks. We have no doubt in our mind that China's non-performing loans will escalate in the future, therefore we believe that an investment in Chinese banks is risky.

Furthermore, when the Chinese property boom turns sour, various asset markets and economies will be impacted. First and foremost, the prices of base metals may fall from their lofty levels and this will affect the earnings of the major mining companies. Remember, China is the major importer of base metals and any slowdown in its real-estate construction will diminish demand for industrial raw materials. Accordingly, we have recently liquidated our investment positions in the base metals mining companies.

Moreover, any fallout from the Chinese real-estate bust will surely impact the economies of the commodity-producing nations such as Australia and Brazil. Thus, investors should remain vigilant and perhaps reassess the risk/reward of their cyclical investments in these resource-rich nations.

Now, this may sound strange but despite our near-term concern about China's housing bubble and our bearish stance towards certain sectors, we remain optimistic about the nation's long-term economic prospects.

In terms of the broader Chinese economy, we believe that a housing bust in China will cause some hiccups in its breakneck growth. However, we suspect that this slowdown will be temporary because most Chinese households are not leveraged to their eyeballs (China's household debt to GDP ratio is below 20%).

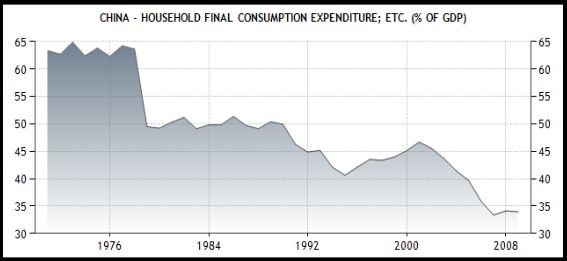

Furthermore, it is notable that currently, China's private domestic consumption accounts for only 34% of GDP (Figure 2) and in our view, this percentage will increase in the future. Remember, in its latest five year plan, Beijing has made it clear that it wants to increase private consumption and reduce China's dependence on low-margin manufacturing and exports.

Figure 2:

China's domestic consumption set to increase?

Source: Trading Economics

It is our contention that China's policymakers are serious about this issue and they have the necessary tools to encourage domestic consumption. For instance, if Beijing allowed its currency to appreciate, such a move will undoubtedly increase the purchasing power of the Chinese, thereby increasing private consumption.

Despite the looming property bust, it is our contention that China's stock market has already discounted the housing problem and this is why the Shanghai Composite Index is trading approximately 55% below its all-time high. As far as valuations are concerned, it is notable that the index is trading at 17 times reported earnings, which is remarkably cheap when you consider the 12-year average price earnings ratio of 34. Last but not least, if you factor in this year's corporate earnings growth, the index is valued at just 13.1 times projected after-tax earnings.

In summary, given our long-term optimism towards the Chinese economy and the historically low valuations, we are maintaining our investment exposure to our preferred companies in China. While we continue to avoid the property developers and banks, we have allocated capital to terrific Chinese companies which should benefit from an increase in China's domestic demand.

If our assessment is correct, the ongoing weakness in Chinese stock prices is a good buying opportunity for the patient investor.