The world’s major economies are struggling and their private-sector is deleveraging (paying off debt). If history is any guide, this deflationary process is likely to continue for several years.

You will recall that heading into the global financial crisis, corporations and households in the developed world were leveraged to the hilt. During the pre-crisis era, debt was considered a birth right and for decades, the private-sector leveraged its balance-sheet. Unfortunately, when the US housing market peaked and Lehman went bust, asset values plummeted but the liabilities remain unchanged. Thus, for the first time in their lives, people in the developed world experienced the wrath of excessive leverage.

Today, the private-sector in the West is struggling and for the vast majority of households, their liabilities now exceed their assets. Furthermore, incomes have also declined (or vanished), thereby making the debt servicing even more difficult. Consequently, in order to avoid bankruptcy, the private-sector in the developed world is now trying its best to reduce its debt overhang. Instead of getting excited by near-zero interest rates and taking on even more debt, it is now doing the unthinkable and paying off its liabilities.

Figure 1 shows that despite the Federal Reserve’s carrot of almost free credit, the private-sector in the US is deleveraging. As you can see, since the bursting of the housing bubble, America’s companies and households have been accumulating large surpluses. Make no mistake, it is this deleveraging which is responsible for the sluggish economic activity in much of the developed world. Furthermore, this urge to repay debt is the real reason why monetary policy in the West has become ineffective.

Figure 1: America’s private-sector is not playing Mr. Bernanke’s game

Source: Nomura

If you review data, you will note that in addition to the US, most nations in Western Europe are also deleveraging and this explains why the continent’s economy is on its knees.

The truth is that such periods of deleveraging continue for several years and when the private-sector decides to repay debt, interest rates remain subdued and monetary policy becomes ineffective. Remember, during a normal business cycle, monetary easing succeeds in igniting another wave of leverage. However, when the private-sector is already leveraged to the hilt and it is dealing with negative equity, low interest rates fail to kick start another credit binge.

As much as Mr. Bernanke would like to ignore this reality, it is clear to us that this is where the developed world stands today. Furthermore, this ongoing deleveraging is the primary reason why the Federal Reserve’s stimulus has failed to increase America’s money supply or unleash high inflation. Figure 2 shows that over the past 4 years, the US monetary base has grown exponentially, yet this has not translated into money supply or loan growth.

Figure 2: Liquidity injections have failed to increase US money supply

Source: Nomura

At this stage, it is difficult to forecast when the ongoing deleveraging will end. However, we suspect that the private-sector may continue to pay off debt for at least another 4-5 years. In our view, unless the US housing market improves and real-estate prices rise significantly, American households will not be lured by record-low borrowing costs. Furthermore, given the fact that tens of millions of baby boomers are approaching retirement age, we believe that the ongoing deleveraging will not end anytime soon. Due to this rare aversion to debt, interest rates in the West will probably remain low for several years.

It is noteworthy that interest rates are established by the supply and demand for credit. When business activity is booming and demand for credit is strong, interest rates tend to rise. Conversely, when business activity is muted and demand for new loans is weak, interest rates tend to decline.

In this respect, Japan’s post-bubble experience shows that despite a massive explosion in its government debt, the island nation’s interest rates have continued to fall for over 20 years! Interestingly, Japan’s ongoing experience is consistent with America’s own prior episode of deleveraging which took place after the Great Depression.

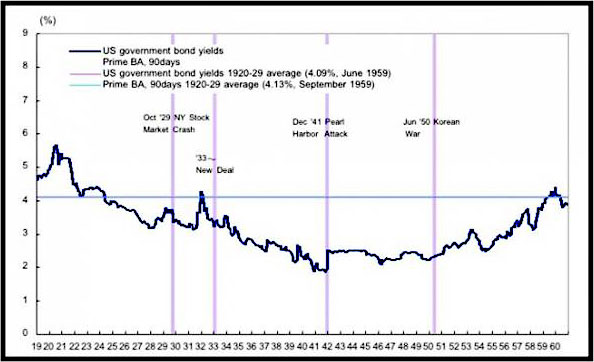

Figure 3 confirms that in the aftermath of the 1929 crash, US bond yields remained suppressed for nearly two decades and only normalised after 30 years! Turning to the present situation, short term interest rates in the US are near zero and long term interest rates are at historic lows. For sure, the Federal Reserve is partly responsible for this suppression, but we are of the opinion that the ongoing deleveraging is the chief culprit.

Figure 3: US interest rates in the aftermath of the Great Depression

Source: FRB, Banking and Monetary Statistics

It is our contention that as long as demand for credit remains weak, business activity will not pick up. Furthermore, unless the central banks start sending out cheques to every household, inflationary expectations in the West will probably remain in check.

Today, some of the world’s most prominent central banks are engaged in quantitative easing and Mr. Bernanke has now embarked on an open-ended monthly ‘stimulus’. However, despite such blatant monetary debasement, it is interesting to note that US Treasury yields are staying near historic lows and the prices of precious metals are not going through the roof.

These developments clearly show that investors are not particularly worried about future inflation and they are still allocating capital to ‘safe haven’ assets such as German Bunds and US Treasury securities.

Figure 4 shows that despite various ‘stimulus’ programs, interest rates in many prominent economies are near historic lows. Moreover, it is interesting to note that contrary to the consensus view, interest rates have in fact fallen over the past 4 years!

Figure 4: Global bond yields turning Japanese?

Source: Nomura

When it comes to investing, nothing is set in stone. Nonetheless, we expect long term interest rates to remain exceptionally low for several years. For instance, if Japan’s post-bubble experience is any guide, then it is conceivable that interest rates may remain around current levels for another decade or longer.

Bearing in mind the fact that the private-sector in the West is refusing to take on more debt, the world’s economy is likely to remain sluggish for several years. Under this scenario, interest rates may remain low for an extended period of time and investment returns are likely to remain muted. Furthermore, in this age of deleveraging, we believe that the former high-flying (export dependent) economies could really undergo extreme volatility. Last but not least, in this type of low growth environment, cyclical industries and industrial commodities are likely to disappoint investors.

Turning to the world’s largest economy, it is encouraging to note that its housing market seems to be bottoming out. Amidst all the doom and gloom, at least this is one bright spot and a sustainable recovery in this sector will surely improve consumer sentiment. At this stage, there is no way to know whether America’s housing has already hit rock bottom, but the recent uptick in housing starts and permits are positive signs.

Over the long run, income and household formation determine the state of every real estate market. Generally, property prices rise in line with household incomes.

During a real estate boom, both valuations (price to income ratio) and new construction rise above their historic trend. Furthermore, the availability of cheap credit and relaxed lending standards fuel the euphoria and rising prices generate a herd mentality. During the final phase of a real estate boom, property becomes a national obsession and people delude themselves into believing that ‘this time is different’. After several years of rising home prices, the participants become convinced that their market is somehow special, therefore not subject to the laws of economics. Interestingly, such misplaced optimism is almost always accompanied by the usual misconceptions (land is scarce, home supply is limited, central banks cannot print houses, affordability does not matter etc.)

Unfortunately, no real estate boom lasts forever and the quality of the hangover is alwaysproportionate to the extent of the indulgence i.e. the bigger the boom, the bigger the bust.

After the boom has turned into a bust, the opposite occurs during the downturn. Both, valuations and new construction fall below their historic trend. Furthermore, credit becomes scarce, property transactions evaporate and there is a buildup of unsold inventory. Last but not least, optimism and euphoria are replaced by outright despair.

Whether you agree with it or not, mean reversion is the most reliable feature for any real estate market. Although real estate is one of the most cyclical assets (prone to extreme booms and busts), the property cycle is lengthy in duration and quite difficult to read. For instance, most market participants are unable to tell where they are in any given cycle.

In terms of the US real estate market, history has shown that its gyrations follow a somewhat regular pattern. In fact, between 1960 and 1990, real US home prices peaked every 10 years (in 1969, 1979 and 1989). Thereafter, a long 17-year interval occurred before the next top in 2006 and it appears as though Mr. Greenspan’s easy money policy extended the most recent real estate cycle.

Today, inflation adjusted real estate prices in the US are well below trend and mass euphoria has been replaced by abject despair. Thus, it is conceivable that America’s housing market is now bottoming out and getting ready for the next upswing which may last for at least 10 years.

It is notable that after topping out in 2006, America’s real estate prices declined by approximately 34% over the following 6 years. However, over the past couple of months, prices have rebounded sharply in some of the hardest hit regions and now it will be most interesting to see whether this nascent recovery can be sustained.