I’ve been doing some recent work on housing to check back in with the health of the recovery. There are a number of different statistics we can look at to gauge housing’s health. I think the most important one I can highlight is the affordability index by the National Association of Realtors (NAR). This was an index we highlighted back in 2005 and 2006 that spoke to us concerning a bubble in housing. I have been tracking the recovery in housing sales on the weekly wrap up for FSN since December of 2011 and the recovery in price since the first quarter of 2012 and it is still pretty clear that the housing recovery has room to improve.

I’ve been doing some recent work on housing to check back in with the health of the recovery. There are a number of different statistics we can look at to gauge housing’s health. I think the most important one I can highlight is the affordability index by the National Association of Realtors (NAR). This was an index we highlighted back in 2005 and 2006 that spoke to us concerning a bubble in housing. I have been tracking the recovery in housing sales on the weekly wrap up for FSN since December of 2011 and the recovery in price since the first quarter of 2012 and it is still pretty clear that the housing recovery has room to improve.

Tailwinds:

Don’t Fight the Fed

The Federal Open Market Committee began a new quantitative easing policy in September of 2012 that includes the purchasing of agency mortgage-backed securities at a pace of billion per month in addition to the long-term Treasury securities it has been purchasing since late summer of 2011. The Fed has been purchasing billion Treasury notes per month while selling the same amount in short-term Treasuries to “twist” the yield curve. Starting in December of 2012, the Fed has removed its sterilization of its Treasury purchase program and now billion in long-term Treasury securities has joined the mortgage-backed securities purchases in outright QE. The committee has shown some debate over the policy in its minutes, but the recent policy statement yesterday showed no consideration to remove the policy in the near term.

In addition to outright QE in mortgage-backed securities and Treasuries, the Fed is continuing to maintain its zero interest rate policy (i.e. ZIRP) until unemployment drops below 6.5% or inflation rises above 2.5%, slightly above their long-run 2% goal. According to some of the forecasts of the voting members, this isn’t likely to change until 2014 to 2015.

With only one policy dissent, it is likely that Fed policy will remain very accommodative for some time. This is the ultimate tailwind to the housing recovery. The Fed is clearly inflating to combat the worst contraction in housing in many decades. As Martin Zweig understood the power of Fed printing, he would say of this situation, “Don’t fight the Fed”.

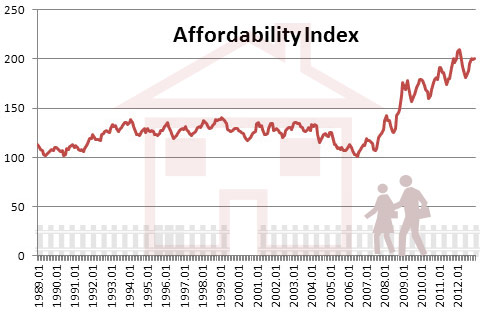

Affordability

As I said, another large tailwind behind the recovery is the affordability of homes. Despite the rise in the median price for a single-family home from January 2012 to now, roughly 16.6%, monthly mortgage interest rates and income levels have improved. The monthly mortgage rate has dropped from 6.69% in 2006 to 3.43% at the end of 2012. The median family income has risen 5 percent from ,497 to ,824). This has pushed the affordability index to record highs. In fact, the affordability index is now twice the value of the index at the housing peak in June of 2006.

Data Source: NAR

Economics of Housing:

NAHB Housing Market Index

We’ve recently seen a few housing data points this week and Lennar reported earnings on Wednesday. Starting off with the NAHB index on Monday, the index dropped for the second consecutive month in a row. Although the traffic of potential buyers recovered from 32 to 35, present single-family sales fell from 51 to 47, pulling the housing market index down from 46 to 44 in March. Despite the recent downticks, the index is well off its lows near 15 in 2011 and the trend is still clearly up for the index. The increased buyers traffic in March is a leading indicator of improvement in the near future.

New Construction

The U.S. Department of Housing and Urban Development released the new residential construction in February just this Tuesday. Within the report, the seasonally adjusted building permits for February were at an annual rate of 946,000, which was 4.6 percent above January’s number and 33.8 percent above February a year ago. Housing starts in February were at a seasonally adjusted annual rate of 917,000, which was 0.8 percent above January and 27.7 percent above the rate last year at this time. Housing completions were at a seasonally adjusted annual rate of 711,000, which was 0.6 percent below the January estimate, but 24.3 percent above the February 2012 rate. Overall, the new residential construction data indicates the upward trajectory for housing will continue.

Mortgage Applications

The weekly MBA mortgage applications survey is showing that activity has taken a dip recently but is up 9% from a year ago. The 30-year fixed rate has moved up from 3.69 at the end of January to 3.82 last week, about a 13 bip increase. Most of the dip recently has been related to refinance activity while mortgage interest rates rose modestly. One of the reasons for the rather large divergence between home sales and mortgage applications is likely due to institutional investors who primarily use cash to acquire real estate. According to CoreLogic, institutional investors in 2012 were 30% of all sales in Miami, 23% in Phoenix, and nearly 20% in Charlotte and Las Vegas.

Existing Home Sales

Today’s existing home sales advanced in February to a new 3-year high. Sales slowly advanced to a 4.98 million annualized units pace. Though it was below consensus estimates for a rate of 5.04 million, it was nevertheless a gain from the upwardly revised January annual sales rate of 4.94 million units. Demand continues to improve, but inventories are tightening and the share of distressed home sales continues to dwindle, therefore, driving housing prices higher.

Lennar Earnings

Lennar posted strong first quarter earnings yesterday. Earnings were .5 million versus million a year ago. Lennar’s CEO said that demand is strong as a result of low interest rates and attractive home prices, which have both led to affordable monthly payments compared to rising rental rates. Lennar has also been very aggressive in its land acquisitions, having spent 0 million in the first quarter. In the conference call, they said large public companies have access to capital and supply of land while smaller private builders did not. As such, public companies like Lennar are gaining market share.

Headwinds:

Underwater

Housing still has some remaining headwinds. According to CoreLogic, 27 percent of residential properties were underwater or close (under 5 percent equity) at the end of the third quarter last year. That’s in comparison to 29 percent at the end of 2009. This suggests that the price of homes would need to continue to increase by quite a bit for these homeowners to be able to refinance. This continues to be a major headwind in mortgage applications.

Interest rates

While the 10-year and 30-year Treasury bond remain at historically low levels, the writing is on the wall that interest rates are bound to head higher. I can remember many saying the same thing a couple years ago with QE and the 10-year at 3 percent, but look how far a trend can go. The 10-year Treasury was near 1.5 percent only a few months ago. Now that economic activity has improved in the U.S. and inflation expectations are creeping higher, we are finally seeing interest rates rise, even in mortgage rates with the recent MBA mortgage application release. So at what point do interest rates need to rise to curtail the housing recovery? Nobody knows yet. The housing economic indicators will eventually tell us and that hasn’t happened yet.

Conclusion

The housing recovery is robust and the tailwinds servicing the trend remain well in tact behind affordability and a monetary policy assuring it stays that way for some time. Some of the economic indicators regarding housing have taken a step back, while some of the leading components suggest stronger numbers ahead. Sales and construction continue their upward bias and company earnings from Lennar suggest that large public companies are in the sweet spot. Lennar’s conference call offered additional clarity from the seller’s point of view that also supports housing. Is it a bubble? Not yet according to the Affordability index, but low interest rates will not be here for much longer. Economic strength stemming from housing and manufacturing will eventually cause rates to go up. The combination of higher rates and higher home prices will eventually hinder the housing recovery, but that doesn’t seem to be the case right now.