With the end of asset purchases in sight (and assuming activity does not lurch downward) Fed officials will increasingly turn the discussion toward raising interest rates. It is not as if the anticipated time line has been any secret. The Fed's forecasts clearly show an expectation of higher rates in 2015 with the exact timing and pace of that tightening dependent upon each participant's growth and inflation forecast. Fed officials would want to clearly telegraph such a move well in advance. Hence they will pivot from talk of sustained low rates to raising rates. Of course, we would expect hawks to be first in line, as they have been. For instance, Philadelphia Federal Reserve President said last week (via the Wall Street Journal):

“Most formulations of standard, simple policy rules suggest that the federal funds rate should rise very soon–if not already,” Mr. Plosser told a conference sponsored by the University of Chicago‘s Booth School of Business.

Such warnings from Plosser are not new. More notable is San Franscisco Federal Reserve President John Williams' interview with Robin Harding at the Financial Times. Williams is generally seen as a dove, but he was also was one of the first to telegraph the end of asset purchases. Williams on the forecast:

In his own economic forecast, Mr Williams said, the Fed will raise interest rates in the middle of next year with the unemployment rate at about 6 per cent, inflation at 1.5 per cent and “everything moving in the right direction”.

“At that point if we don’t start to adjust monetary policy there’d be a risk of overshooting,” he said. “You don’t wait until you’re at full employment before you start to raise interest rates from zero.”

There is a lot to think about in those two paragraphs. First is a forecast of 6% unemployment 15 months or so from now. Given the rapid drop in the unemployment rate, it is completely believable that we reach 6% before asset purchases are predicted to end later this year. Given Williams' forecast, this suggests to me that the risk here is a more rapid tapering or earlier rate hike. The second is the idea of raising rates when inflation is only 1.5%. This to me suggests that Williams is expecting to reach the 2% target from below, not above. This seems clear from the next point: WIlliams wants to take the possibility of overshooting off the table.

[Hear More: Brian Pretti: Rising Interest Rates the Biggest Risk in 2014]

Note that Williams' position differs greatly from that of Chicago Federal Reserve President Charles Evans. From a speech last week:

A slow glide toward our goals from large imbalances risks being stymied along the way and is more likely to fail if adverse shocks hit beforehand. The surest and quickest way to get to the objective is to be willing to overshoot in a manageable fashion. With regard to our inflation objective, we need to repeatedly state clearly that our 2 percent objective is not a ceiling for inflation. Our “balanced approach” to reducing imbalances clearly indicates our symmetric attitudes toward our 2 percent inflation objective.

Evans is obviously willing to overshoot, where Williams is not. Whether the consensus sides with Williams or Evans is critical to the timing of the first rate hike. If the consensus is set on hitting the inflation target from below, then we have have to consider the Fed's own forecasts as suspect. They will find themselves moving sooner than they expect.

I would say, however, it is widely believed, on the basis of her "optimal control" analysis, that Federal Reserve Chair Janet Yellen leans toward Evans. Any suggestion that Yellen leans toward Williams on the overshooting question would be notable.

Regarding asset purchases, Williams joins the chorus indicating the bar to change is high:

Mr Williams said it would take a “substantial change in the outlook” before he was willing to revisit the Fed’s plan to slow purchases by $10bn at each meeting, and despite some weak data, that has not yet happened. “We haven’t really changed our basic outlook for the economy.”...

...Mr Williams said that as long as average monthly jobs growth stays well above 100,000 then unemployment will continue to come down. “What would worry you is if you don’t have an explanation for why it’s weaker and you get multiple months below that,” he said.

I don't think this should come as a surprise. The Fed has been looking to get out of the asset purchase business since the beginning of 2013. The end is now in sight, and only the most disconcerting of data will change that. They may say they are data dependent (Williams of course adds that he could envision circumstances in which the Fed slow or even reverse tapering), but the reality is they have a bias against asset purchases.

The desire to exit asset purchases only increases as the unemployment rate falls. I think that Joe Weisenthal is on the money here when he points out that economists are gravitating toward the idea the the changes in the labor market are largely structural. In other words, as St. Louis Federal Reserve puts it (via the Wall Street Journal):

“I think that unemployment is really sending the right signal about the labor market” and the decline in the labor force participation rate is largely a demographic issue that will play out over a long time horizon, he said.

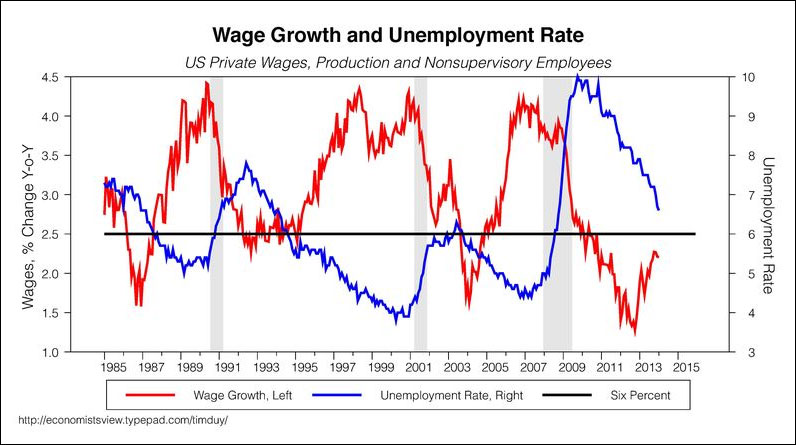

I think that Fed officials have long seen the risk that this might be true, which is one factor that biases them against asset purchases. Increasing, though, I suspect they do not see is as a risk, but as reality. Again, the consequence is that rates might be rising sooner than Fed officials currently anticipate. It is worth repeating this chart:

In the past, wage growth accelerates as unemployment hits 6%. With unemployment well above 6%, it was difficult to conclusively say much one way or another about the exact amount of slack in the labor market as there was certainly enough slack to keep wage growth in check. If the unemployment rate is no longer the appropriate indicator of labor market slack, then we should not expect to see upward wage pressure as 6% looms. If that pressure does emerge, then I think we learn something about the amount of slack. From the Fed's point of view, if they see wage growth, they will suspect their isn't much. Wage growth will raise concerns about unit labor costs, which will in turn raise concerns about inflation.

Weisenthal, however, adds:

The view from the left is basically: Even if the labor market is getting tight (which they deny), the Fed should press hard on the gas pedal, so that employers start to employ the long-term unemployed.

And that might be the proper path, and if there's anyone who has the stomach to engage in the strategy, it's probably Janet Yellen.

Once again, this implies that Yellen is willing to risk overshooting. Her views on overshooting are critical to the evolution of policy at this point.

Bottom Line: Put aside the possibility of an international crisis-fueled collapse in activity. The Fed's baseline view is that economic growth continues this year at a pace sufficient to end the asset purchase program. The Fed will resist changing that plan for any minor stumble in activity. The pace of job creation itself might not be that critical; it simply needs to be fast enough to lower unemployment to justify continuing the taper. Moreover, we are reaching a point where the Fed will need to decide to what extent it will risk overshooting. That was never really a risk of overshooting above 6% unemployment. Soon it will be an interesting question. The timing of the first rate hike and the subsequent tightening is dependent upon the consensus on overshooting. If wage growth starts to accelerate, the Fed's focus will shift from fears of too much to too little slack. If they are concerned about overshooting, they will need to accelerate the tightening time line. Where Yellen ultimately falls on the issue is critical.