"By the time a queen bee is five she is old and no longer reproduces, leaving her army of honeybees torn between loyalty and survival. Since the hive cannot survive without a productive queen, the beekeeper reaches into the hive with a long-gloved hand and squashes the enfeebled queen. With the entire hive as a witness, all know the queen is dead. Absent the scent of their leader, the honeybees panic. But, the beekeeper is prepared, having ordered a new queen from a bee breeder. Arriving in a two-inch-long wooden box with a screen at the top and bottom, the queen is accompanied by a court of six to eight escort bees who care for her every whim, cleaning her, feeding her, removing her waste. At one end of the box, a tiny piece of hard candy blocks access to the queen. When the box is inserted into the hive, the first instinct of the worker bees, who immediately know she has the wrong scent, is to kill the new queen. The workers struggle to reach her but are blocked by the candy. Soon they become diverted by the sweet [candy], and over the two or three days it takes to eat through it to succumb to the enticement. Their fealty is won. All hail the new queen."

— “Three Blind Mice” by Ken Auletta (American writer, journalist, and media critic)

Something similar to this “new queen bee” story is happening now. The “old queen” has been the Federal Reserve and monetary policy. The “new queen” appears to be the White House and fiscal policy. The White House seems nervous that monetary policy, the Fed, and up until recently the continuing policy of lowering interest rates, has not produced the typical strong economic rebound following a “soft patch.” So, the “new queen” looks to be fiscal policy and the White House. As repeatedly stated, “The White House is ‘driving’ the equity markets and not the Fed, which is a huge change from the past two decades.” Now Wall Street loved the old queen. The Street loved lower interest rates, figuring that stimulation would revive the banks, business, and the economy in general. Yet many investors are leery about the new queen. The Street worries that tax cuts could be a catalyst for bigger budget deficits and higher inflation. Moreover, the media, the Democrats, and even many Republicans appear to be taking every opportunity to undermine our new President. However, the White House figures that Wall Street will eventually succumb to the sweet lure of tax cuts, reduced regulation, repatriation of foreign corporate profits, a fix for Obamacare, etc. But, beekeepers sometimes get stung! The head beekeeper in Washington D.C., the President, knows that the economy remains in a fragile state. He knows the worker bees are worried about their jobs, their hive, and their honey. He knows they will sting Republicans in the next election if he does not get the economy moving again, but we think he will.

Wall Street is also worried about getting stung. The Street has bid the S&P 500 (SPX/2351.16) up ~30% from last year’s February lows, and up nearly 10% from the Presidential election lows, with many indices doing better than that. So what’s driving the Trump rally? Well, as the always insightful Craig White, portfolio manager of the Canada-based HugganWhite Wealth Management organization, writes:

- Stimulus measures proposed by the new administration including tax reform, increased infrastructure spending, a reduction in regulation and the potential repatriation of offshore dollars.

- A strong fourth quarter earnings season, highlighted by more than 65% of reporting companies beating expectations.

- Multiples that are fairly valued based on forward earnings expectations.

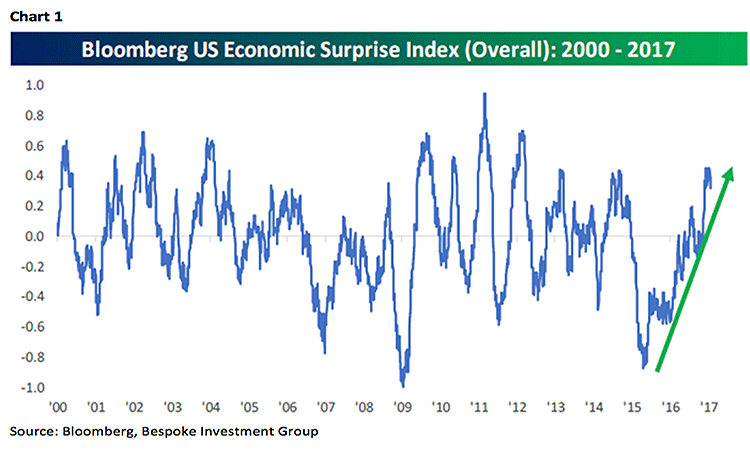

- An economic backdrop that continues to show resilience with employment, manufacturing, wage growth etc. all trending positive.

- Business optimism that has picked up materially over the past year.

- Fund flows benefiting equities for the first time since mid-2104.

- An improvement in overall sentiment compared to early 2016.

We agree with point 1, except we do not think infrastructure spending will occur quickly. The majority of infrastructure spending happens at the state and local level, so it is hard to envision how the government can wave a magic wand and immediately foster such spending. Recall that when the American Recovery and Reinvestment Act (ARRA) was passed it took a long time before the first dollars “showed up.” Point 2 we clearly agree with since we remain of the view the “profits trough” occurred in the 2Q16 and the equity markets are/have transitioned from an interest rate driven to an earnings-driven, secular bull market. Indeed, as of last Friday, of the S&P 500 companies that had reported 4Q16 earnings, aggregate earnings improved by 7.5% with 69% of those companies reporting better than expected numbers. Three, if you believe S&P’s 2017 earnings estimate for the S&P 500, and that for every one point drop in the corporate tax rate hypothetically adds .31 to those earnings, stocks are not all that expensive. Four, there is little doubt the economy is getting better. Five, hereto there is little doubt small business optimism has soared. Six, investors poured nearly billion into equity mutual funds and exchange-traded funds in the week of February 15. And seven, the sentiment is profoundly ebullient, which is actually a cause for some near-term concern.