Hard data is soft! Retail sales have contracted 2 months in a row, construction spending and industrial production data are soft and other hard data inputs have pressured economic models sharply lower in their 1st quarter GDP estimates. When the economic outlook is soft, interest rates along with stocks earning forecasts decline.

Check out The Behavior of the Market Actually Has Very Little to do with Trump

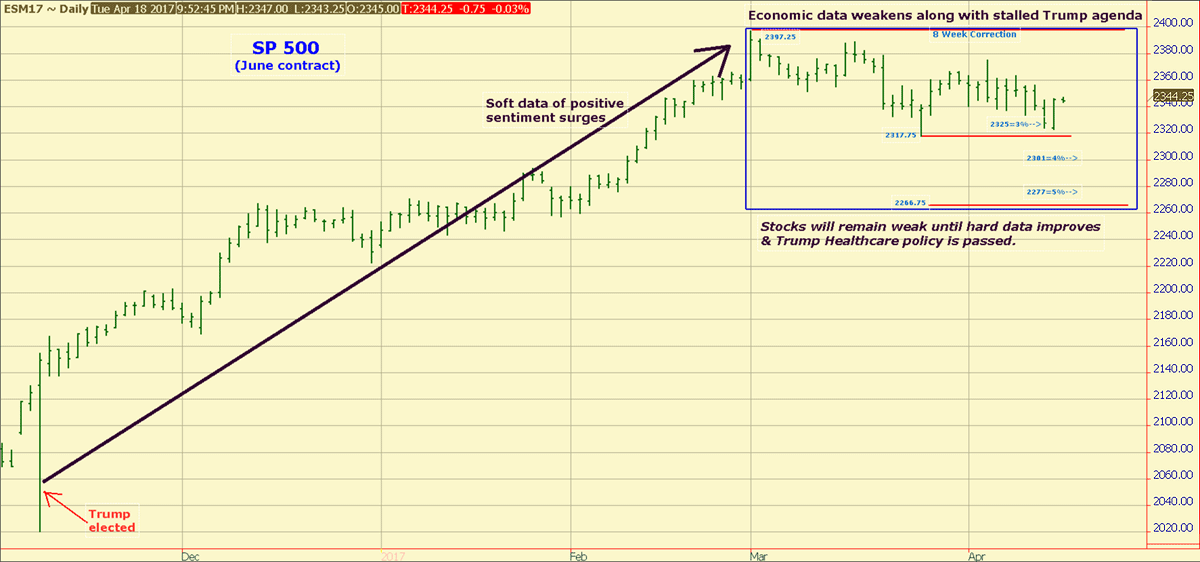

Until March the vast majority of economists had expected 1st quarter GDP growth in the range of 2 to 3%. Now the estimates are likely to coalesce under 1% when the 1st estimate arrives April 28th. Each time the estimates spiral lower, interest rates and stock prices fall in sympathy.

When Trump was elected, Small Business and various regional Fed Districts optimism soared at record rates. Most of this was based on soft data – sentiment. This expectations data has been further supported by European and Global Purchasing Manager surveys of expected orders, production, and employment that have been hitting 6 and 7-year highs. In March it became apparent that the hard data of actual consumption and production metrics had been softening, revealing one of the largest divergences of soft and hard data. Such divergence of expectations over current reality has primed stocks for disappointment. With the Trump agenda in limbo following the March Healthcare quagmire, stocks could no longer rally to new highs. We have said since November that the downside risk was no more than 2 or 3% as sidelined investor sentiment was too anxious to buy every dip. That sideline euphoria evaporated in March and April allowing a larger correction potential.

AAII investor and Option trader sentiment are moving toward oversold, but there is still room for new 2 to 3 month lows in stock indices before pessimism signals an oversold condition for investors to step in and buy. Once we move past the April 28th GDP release, investors will shift their focus to more optimistic 2%+ 2nd quarter GDP forecasts. Trump needs Healthcare or much better economic data before the stock market will consider another run to new highs. Bonds are the “tell”. Interest rates are hitting 5-month lows this week, hinting that the softer economy consensus is still growing.

Become a subscriber and gain full access to our premium weekday interviews with leading guest experts by clicking here.