Respected media icons, economists, hedge fund managers and self-aggrandized pundits have long predicted an immediate stock market crash and recession upon the astronomically remote odds of a Trump Presidency. Shark Tank’s Mark Cuban and the vociferous majority were correct — for a couple hours! However, the silent smart money and bulge investors quickly stepped in to create a new Bull market stampede on the speculation that Trump would be the most aggressive pro-business executive to be CEO of the most powerful nation on the planet. “Yuge” unknown policy risks remain from such a mercurial leader, but the high confidence bet is evolving that the economy will be unshackled from current regulatory brakes and impelled to invest by an unprecedented blitzkrieg of incentives. The unrelenting appreciation of financial assets since November 8th has increasingly created pent up dry powder awaiting a better entry point to board the Trump Train, ‘hoping for change’.

Check out Marc Chandler: Dollar’s Bull Run Not Over; Euro Likely Heading Lower

A characteristic of a new Bull market is its tendency to minimize opportunities to invest at desired prices. This post-election surge looks unlikely to allow an easy buy zone until a strong short to medium peak has arrived. This Trump rally has appreciated almost 15% or 2,500 Dow points from the November 9th intraday low without a 2% pullback. Most investors are hoping for at least a 4 to 6% correction down toward Dow 19,000 before purchasing stocks. Don’t hold your breath.

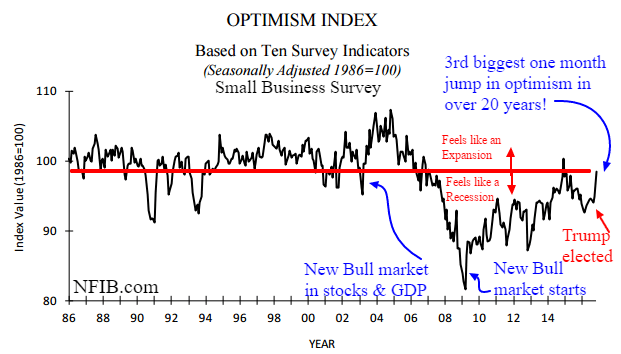

In addition to stock investor euphoria, economic optimism has quickly soared to nearly 10-year highs upon the news of Trump’s victory. Hope and Change have been Trumped as investors sense an aggressive focus on growing the economy.

Small Business surveys have shown a persistent dour assessment about the past 9 years. The former job engines of past recoveries have been left in subsistence mode during the Obama era waiting for the recession to transform to prosperity. Suddenly the election has boosted sales expectations for 2017 based upon lower operating costs and improved spending promised by Trump.

Not only are CEO’s excited, but consumer pre-election fatigue has now morphed into post-election relief and more ebullient shoppers as well. If Trump lives up to half of his hype, then sheer excitement may compel faster rates of consumption in 2017.

The New York Empire and Philadelphia Fed surveys this week also reflect robust business expectations that bode well for increased manufacturing. Quick surges of the Empire State index to the 50 level is more typical of the first inning of a new or mid-cycle upturn (2002/2009/2012). The slow growth recovery from 2009 has “technically” been the 4th longest economic expansion in US history, but the slack capacity and surge in sentiment are more indicative of a nascent expansion cycle with room to run.

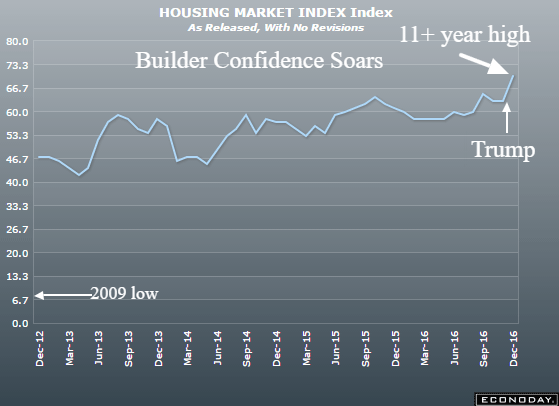

Hammering down to the elusive home building and services industry that account for 15 to 18% of our economy, we also see surging optimism upon Trump’s victory. Since the multi-decade mortgage bubble burst in 2008, housing has been a major impediment to the US recovery during Obama’s first term to be followed by the energy sector collapse in his 2nd term. Today we not only have the headwind of energy turning into a tailwind, but home builders feel the most positive since 2005 and stronger than at any point in the 1980’s and most of the ’90’s.

Hedge funds, investment banks, business owners of all ranks and consumers have literally and figuratively marched into the Golden Trump Towers to say they want to be on board Trump Force One. Exogenous events and inevitable obstacles such as Democrat filibusters and orthodox Republican resistance are unpredictable expected, but at this point “resistance is futile” during this momentous phase of our new populist President and CEO. Investors can’t be too patient looking for corrections to buy as there are still a few Trump cards to play before this stock market advance is ready to disappoint.