From worst to first in one year! The economic surprise index was already trending higher in the US and around the globe last Fall and Trump’s timing was impeccable as current and expected business activity surged since his election. The Citi Economic Surprise Index falls when real activity is worse than expected and conversely becomes more positive when actual economic data exceeds forecasts.

The negative surprises reached their nadir in February 2016 when the oil crash bottomed at $26/barrel. The positive surprises have been accelerating since last September to almost unsustainable levels today. It’s amazing how many forecasters throughout most of 2016 were calling for a recession by late 2016 to early 2017.

When business confidence and activity increase, passengers travel more. Flight activity has risen at the fastest pace in over 5 years.

Travel is accelerating around the world, other than Australia and Brazil. While Brazil is still rebounding from a 2-year depression, their manufacturing optimism has been surging since late 2016. The impressive growth in travel from China is another good sign for the renewed global recovery that has been so elusive for the past 8 years.

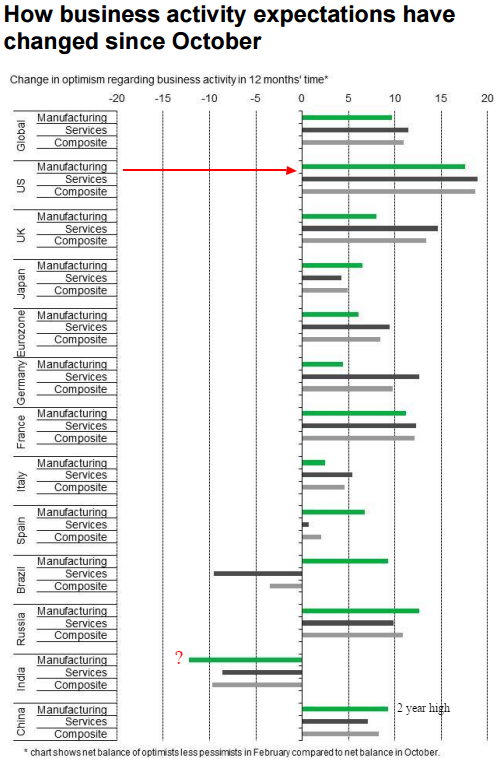

The service economy is far larger than the manufacturing economy, but industrial activity is a key barometer of growth trends in the whole economy. For years, the world has been plagued by overcapacity but with a decent service sector, the global economy has been merely treading water below long-term trendline growth. With manufacturing joining the secular service sector expansion we now have potential to move up an octave in GDP growth. Despite Brexit weighing on the UK and a major Brazilian recession, it’s interesting that the 2 most optimistic countries surveyed for economic expectations are the UK and Brazil.

Other than India, most areas of the world have steadily grown in optimism in recent months.

The US GDP is currently running a bit cold under 2% growth despite the very strong labor and manufacturing data in recent months. Legislative stagnation this spring may also sow some doubt that gives financial markets pause. However, there is no denying the robust “real” and expected growth that has accelerated here and around the world in what appears to be the new up-cycle we have been talking about for the past year. Growth may slow for a couple months but we expect continued gains over the next couple of years.

Become a subscriber and gain full access to our premium weekday interviews with leading guest experts by clicking here.