When it's obvious, it’s obviously wrong! Is there any forecaster, economist, or investment house that doesn’t think interest rates are going higher? Trump’s victory and hyper business cheerleading have accelerated a rush to sell bonds due to the certainty over rising economic growth and inflation. The Federal Reserve finally hiked rates on December 14th, 2016 and promised several more bumps in 2017. As it turns out, the day after the Fed funds rate was raised to 0.75% in December, that marked the high in interest rates to date. Yields on the 10-year have fallen from 2.62% to 2.3% (2.47% last) and may fall further before the next leg of rising rates manifest.

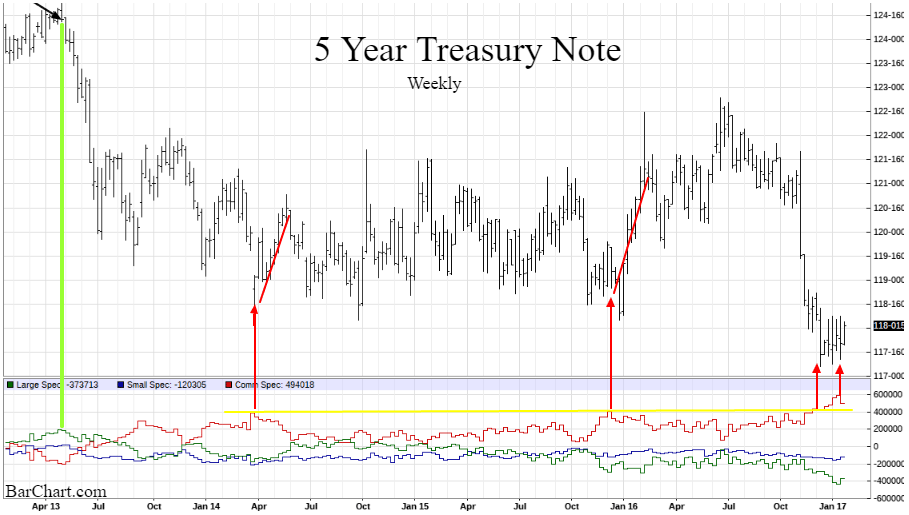

While timing is never precise, the extreme 7-year net short positions by Large Spec Funds (inverse of Commercials) investing for lower bond prices indicate an oversold condition supporting prices (lower yields) over the next couple of months (see the BarChart.com charts below).

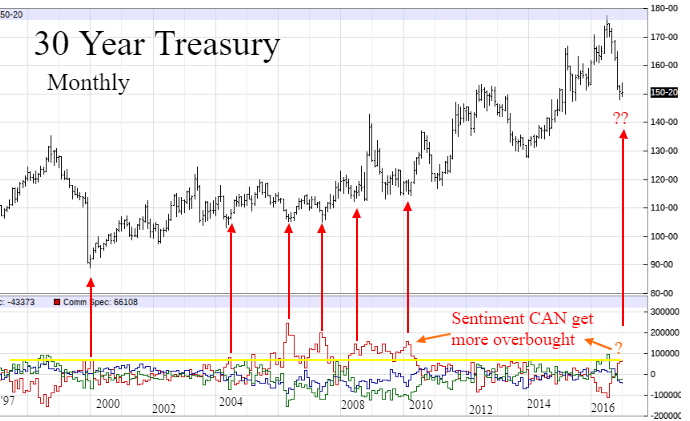

A longer term picture reveals that 30-year bond sentiment does have room to rise further (lower prices) as the focus has been on shorting the near term vs long term bonds.

When we look at the shorter maturities, it’s quite evident that there has been a rush to sell short the 5- and 10-year notes more than the long-term 30-year bond duration as record bearish sentiment has far exceeded past records. It’s a positive sign of growth expectations to see fund flows betting on short rates rising faster than long rates as it indicates expectations of economic acceleration.

History indicates that bond prices should move higher before new lows are reached to relieve the extremely oversold pricing pressure of short hedges by Large Spec Funds.

We feel strongly, like most investment houses, that the economy and interest rates will move higher over the next 2 years. This is congruous with our call for lower interest rates in the 1st quarter 2017 as bond bears have moved ahead of their skis with such large pessimistic bets of net short investment hedges targeting higher yields. Once yields drift lower and Spec funds cover part of their net short positions, then another leg up in yields can begin. Ours is a contrary opinion perspective. When sentiment reaches an extreme, vulnerability to reversals become more likely. Until GDP quarterly forecasts start pushing well north of 3% growth rates in 2017 or new highs in oil prices are reached, mildly lower rates should prevail. One caveat would be an exogenous inflationary event causing suddenly higher commodity prices, perhaps from Trump sanctions or military threats against Iran. Bond gurus Bill Gross and Jeff Gundlach think that 2.6% and 3% on the 10-year are the demarcations for Doomsday. For now, rates have stalled and we consider rising rates a sign of a faster economy, higher earnings, and rising stock prices.

Become a subscriber and gain full access to our premium podcast interviews with leading guest experts by clicking here.